Amazon has a diversified business model. In 2023, Amazon generated nearly $575 billion in revenues while it posted a net profit of over $30 billion. Online stores contributed over 40% of Amazon revenues. Third-party Seller Services and Physical Stores generated the remaining. Amazon AWS, Subscription Services, and Advertising revenues play a significant role within Amazon as fast-growing segments.

Value Model: Selection, Price, and Convenience at scale.

Amazon’s mission statement is to “serve consumers through online and physical stores and focus on selection, price, and convenience.” Therefore, Amazon’s underlying values as a platform are selection, price, and convenience.

Amazon’s leading platform is an e-commerce marketplace, leveraging two-sided network effects. The more sellers join Amazon’s third-party seller services, the more the variety of products available at reasonable prices. That, in turn, brings back more and more users who shop on Amazon. As Amason fulfills its products at scale, the same users become repeat customers by offering a great customer experience, prompting others to join. That, in turn, makes the overall platform more appealing to other sellers.

Distribution Model: Brand, Growth Engine, Continuous Improvement.

Amazon’s growth is built on its strong brand, developed over the years. Amazon’s growth engine is made of a technical platform combined with a diverse variety of products at reasonable prices. Together with a solid underlying platform.

Financial Model: Cash Conversion Cycle.

The company generates cash flows thanks to positive cash conversion cycles. Inventory is turned into cash quickly, and suppliers/third-party stores are paid back within 30-60 days. That gives the company short-term liquidity that can be invested in its operations.

Amazon’s business model today

Before we dive into Amazon’s history and break down its whole business model. Let’s give a look at some of the key highlights for the company, in 2021.

Indeed, by 2021, Amazon had grown into a tech giant, which generated over $469 billion in sales.

Among its sales, over $241 billion were product sales (51.4%), and over $228 billion were service sales (48.6%).

The largest cost the company faced in 2021 was the cost of sales, which represented over $272 billion or 57.9% of the total revenues. Cost of sales comprises primarily sortation and delivery centers costs, together with the transportation service provider, and digital media content costs, including video and music. For instance, as Amazon highlighted, in 2021 the increase in the cost of sales was primarily due to increased product and shipping costs resulting from increased sales, costs from expanding Amazon’s fulfillment network, as well as increased carrier rates, increased wage rates, and incentives, and fulfillment network inefficiencies resulting from a constrained labor market and global supply chain constraints.

The fastest-growing Amazon segment in 2021, compared to 2020, was Advertising. Which grew from over $21.4 billion in 2020 to over $31.1 billion in 2021 (45% YoY). This was followed by Amazon AWS, which grew by 37% YoY, from over $45.3 billion in 2020 to over $62.2 billion in 2021. Third-party seller services and subscription services also grew very fast (see table below).

Amazon AWS is the largest contributor to Amazon’s operating margins. In fact, in 2021, of the total $33.3 billion in operating margins, over $18.5 billion came from AWS. This means that AWS contributed to over 55.5% of overall Amazon’s operating margins. What does it mean? Amazon’s e-commerce platform is running at very tight margins, even though it’s the largest segment. Instead, other segments, like Amazon third-party services, subscriptions, and advertising are running at much wider margins. However, it’s AWS, which, for now, is running at the widest operating margins. This is in part because of the underlying cloud infrastructure that makes Amazon AWS, which today powers up a good chunk of the Internet. In fact, Amazon AWS is among the largest players. Indeed, by 2021, Amazon AWS had revenues of over $62 billion, whereas Microsoft Intelligent Cloud, for over $60 billion, and Google Cloud, for over $19 billion.

The fact that Amazon’s e-commerce platform is the one with the tightest margins doesn’t make it the less important. Quite the opposite. The Amazon e-commerce platform is the main asset of the company. For a strategic choice made two decades ago by Jeff Bezos, Amazon keeps its e-commerce margins low, bypassing low prices to consumers, while on the other hand, building other business segments with very high margins (see AWS, Third-party seller services, Advertising, and Subscriptions).

While Amazon is still a product company, meaning its e-commerce platform is still the main component of its business model. It’s worth noticing how Amazon is leveraging its product side, to build its service business. In fact, Amazon has built a larger set of tools, for third-party stores to sell on top of Amazon. In addition to that, Amazon has also been building its Amazon Subscription business (Amazon Prime) and lastly, Amazon advertising services also are growing exponentially.

It’s also important to emphasize that today Amazon is a very complex business model, comprising various business units. Today Amazon is both a platform (Amazon e-commerce) and an infrastructure (Amazon AWS). This has been possible thanks to a lack of regulation on the Internet. Going forward it might be possible to see Amazon spinning off parts of its business, as a separate company (for instance AWS might be a completely separate enterprise business compared to Amazon e-commerce).

Fun stats:

Amazon Revenue Breakdown

2020

2021

Changes

Online stores

$197.34B

$222B

12.53%

Physical stores

$16.22B

$17B

5.23%

Third-party seller services

$80.46B

$103.36B

28.47%

Subscription services

$25.2B

$31.76B

26.03%

AWS

$45.37B

$62.2B

37.10%

Advertising

$21.45B

$31.16B

45.25%

Fastest Growing Segment

Understanding the tradition from e-commerce to platform

E-commerce focuses its efforts primarily on selling its products, or selling products through its stores, thus measuring its success based on how many products it sells via its stores. Instead, the marketplace focuses its efforts on how many products third-party stores sell on top of the marketplace. Therefore it measures its success based on the transactions on the platform from third-party stores.

Amazon AWS born as a side effect of making an order to the “jumbled mess” that had become Amazon infrastructure in the early 2000s is now the most profitable part of Amazon.

With $13.5 billion in revenues in Q1, it’s among the fastest-growing segments for the company.

And it generated over $4 billion in operating income, which represents almost half of the total operating income of Amazon! In short, if you were to spin off AWS, Amazon would be running at very tight margins.

To be sure it doesn’t mean the e-commerce part is not valuable. The opposite. Amazon explicitly runs it at a loss because it’s what gives the company scale.

And it also enables it to experiment and create new revenue streams. Indeed, Amazon Prime, Amazon seller services, and Amazon advertising (the most profitable segments) are all built on top of the Amazon e-commerce platform.

And Amazon AWS also was born as an attempt to make orders to the Amazon e-commerce infrastructure and enable more and more third-party stores to be hosted on top of it!

So when you look at Amazon, keep that in mind! It’s way way more than just an e-commerce company.

It’s a platform, a marketplace, an advertising giant, a streaming company, and one of the most powerful cloud enterprise businesses, powering up a good chunk of the web!

Was this a random transition? Nope, it was a conscious choice, which took two decades to build Amazon into the company that we know today.

Back in 2019, in Amazon’s shareholders’ letters, one of the last ones fromJeff Bezos, as CEO of Amazon, he highlighted:

The percentages represent the share of physical gross merchandise sales sold onAmazonby independent third-party sellers – mostly small- and medium-sized businesses – as opposed toAmazonretail’s own first-party sales.

Third-party sales have grown from 3% of the total to 58%.

To put it bluntly: Third-party sellers are kicking our first-party butt. Badly.

And it’s a high bar too because our first-partybusinesshas grown dramatically over that period, from $1.6 billion in 1999 to $117 billion this past year. The compound annualgrowthrate for our first-partybusinessin that time period is 25%.

But in that same time, third-party sales have grown from $0.1 billion to $160 billion – a compound annualgrowthrate of 52%. To provide an external benchmark, eBay’s gross merchandise sales in that period have grown at a compound rate of 20%, from $2.8 billion to $95 billion.

He also analyzed the context, to understand what made up Amazon’s success in attracting third-party stores, and he posed a few questions:

Why did independent sellers do so much better selling onAmazonthan they did on eBay? And why were independent sellers able to grow so much faster than Amazon’s own highly organized first-party salesorganization?

There isn’t one answer, but we do know one extremely important part of the answer:

We helped independent sellers compete against our first-partybusinessby investing in and offering them the very best selling tools we could imagine and build. There are many such tools, including tools that help sellers manageinventory, process payments, track shipments, create reports, and sell across borders – and we’re inventing more every year.

In short, a successfulplatformincentivizes third-party stores and e-commerce to compete against the first-party stores, and it offers them a set of key tools to manageinventory, payments, track shipments, and reporting.

But of great importance are Fulfillment byAmazonand the Prime membership program. In combination, these two programs meaningfully improved the customer experience of buying from independent sellers. With the success of these two programs now so well established, it’s difficult for most people to fully appreciate today just how radical those two offerings were at the time we launched them.

AsJeff Bezos, highlighted, those two programs (now widely successful) were not guaranteed to succeed:

We invested in both of these programs at significantfinancialrisk and after much internal debate. We had to continue investing significantly over time as we experimented with different ideas and iterations.

In fact, while those make sense now, and seem obvious, in hindsight, it took a lot of mistakes, failures, and iterations, to get there:

We could not foresee with certainty what those programs would eventually look like, let alone whether they would succeed, but they were pushed forward with intuition and heart, and nourished with optimism.

This passage above is critical to understanding the evolution of Amazon’s business model so that we can understand and appreciate its history.

The history of Amazon

We can break down Amazon’s history in four key waves:

1994-2005: in the early day Amazon, through the vision of Jeff Bezos was among the most prominent Internet players. Amazon had placed substantial bets on various companies and it had quickly scaled its operations. Starting from books, by the late 1990s, Amazon had already expanded into other categories, and Jeff Bezos had placed investments in various Internet startups. As the dot-com bubble burst, though, Amazon not only lost substantial amounts of money into failed bets (the epitome of that was the bankruptcy of Pets.com one of the key bets the company had placed) but it shrank in value, and many analysts predicted its demise. However, in those years, especially in the early 2000s Amazon changed its business playbook. It cut all the investments in things it could not directly control and it started to move from an e-commerce company to a platform business model.

2005-2015: By the mid-2000s Amazon had set the stage for a complete change in its business model. The company had also started to experiment with various programs and products. Some were a complete failure (like the Kindle Fire Phone) and others would turn out into incredible products, and business segments (Amazon Prime, Amazon Advertising, and Amazon AWS).

2015-2020: By the year 2015, Amazon had turned into a tech giant already, and it showed the world, finally, that not only it had survived but that it had the ability to scale at an international level. In these years, Amazon showed the world the incredible numbers behind Amazon AWS (most business players were astonished and other companies like Microsoft and Google started to double down on cloud computing as they saw the success of AWS). And the company managed to expand in Europe, Mexico, and India and tried hard also to break into China.

2020-Forward: as the pandemic hit, Amazon became one of the companies that defined this moment in the history of western humanity. In fact, by choice Amazon started to burn a substantial amount of cash to further scale its service, and make it one of the most compelling for consumers.

Amazon, through the vision of Jeff Bezos, had the merit of creating a customer-obsessed business, which I argue, has been continuously Blitzscaling, since its inception.

The fast pace of Amazon has made it also a very controversial company. In fact, obsessing over customers has made Amazon, a business loved by consumers.

On the other hand, it has also created tensions toward other stakeholders (employees, suppliers, and third-party stores in particular). Indeed, if your main focus is the customer, and you’re obsessed with it, then you might operate in a way that leverages your negotiating position to squeeze other stakeholders.

This has made Amazon a controversial company for sure.

The Launch

Amazon was launched on July 16, 1995, as a humble online bookstore operating out of the garage of founder Jeff Bezos. In little more than two decades, the company is now the largest eCommerce retailer in the world with annual revenue in 2020 of $386 billion. Bezos originally wanted Amazon to be called Cadabra – a shortened version of Abracadabra.

In 1994, Bezos and then-wife MacKenzie Tuttle began registering several domain names. These included Awake.com, Browse.com, and Bookmall.com. The pair ultimately settled on Amazon.com after searching through a dictionary for inspiration. As the biggest river in the world, it aligned with a goal Bezos had to make his online store similarly vast.

What’s in a name?

Bezos originally wanted Amazon to be called Cadabra – a shortened version of Abracadabra.

However, his lawyers advised him that the reference to the popular magic catchphrase might be too obscure. They also contended that Cadabra could be misconstrued as “cadaver” instead.

In 1994, Bezos and then-wife MacKenzie Tuttle began registering several domain names. These included Awake.com, Browse.com, and Bookmall.com. The pair ultimately settled on Amazon.com after searching through a dictionary for inspiration. As the biggest river in the world, it aligned with a goal Bezos had to make his online store similarly vast.

The early years

The original Amazon business model of selling books online was met with much derision from skeptics. Many argued Amazon would not be able to compete with established chains such as Borders and Barnes & Noble.

Where Amazon differed from these established players was convenience. Bezos wanted to deliver online orders directly to any customer anywhere in the world – a process we take for granted now that was revolutionary at the time.

Very early on, a bell would ring in the Amazon office every time a customer made a purchase. The company was so small that employees would crowd around to see if they personally knew the customer.

After a few short weeks, however, orders became so frequent that the bell had to be removed. During its first month of operations, Amazon had sold books to people in all 50 states and 45 different countries. Each order was personally transported to the post office and dispatched by Bezos and his employees.

It all started back in the early 1990s, when a young Jeff Bezos was working at Hedge Fund D. E. Shaw & Co, where he was pulling off a very successful career on Wall Street. Yet as Jeff Bezos recounts, while at the firm, while doing a market research on the potential of the Internet he stubled across a staggering statistics: the web usage was growing at a 2,300% a year.

So he made sure right on to find a business plan that would make sense in that hypergrowth context. And he picked books. Why? As Jeff Bezos pointed out “there are more items in the book category than any other category by far,” with over three million different books worldwide. Only Music was number two.

Keep in mind those words. Indeed, as we’ll see throughout this incredible story. As Amazon scaled up it extended to wider and wider niches, from CDs and music, and slowly, then all of a sudden to everything else.

However, books were an incredible commercial niche, as it was a showcase for Amazon to emphasize the unbounded potential of the Web.

I want to have lived my life in such a way that when I’m 80 years old I’ve minimized the number of regrets that I have

Day One

On October 4, 1995, at 12:00 AM Amazon announced: “World’s Largest Bookseller Opens on the Web.”

They explained in the press release:

At a time when pundits are questioning the advantages of shopping online, Amazon.com offers consumers a shopping experience that would be impossible without the Internet. A physical bookstore as big as Amazon.com is economically impossible because no single metropolitan area is large enough to support such a mammoth store. Were Amazon.com to print a catalog of all of its titles, it would be the size of 7 New York City phone books.

While intellectuals discussed the viability of the internet, Amazon experimented fast. 25 years later, Amazon made over $386 billion in sales, selling way more than books. Becoming the “everything store”, a media house, and among the largest digital advertisers on earth!

Amazon proved the viability of the Internet explaining “a physical bookstore as big as Amazon.com is economically impossible because no single metropolitan area is large enough to support such a mammoth store.”

In 1995 Jeff Bezos highlighted:

We are able to offer more items for sale than any retailer in history, thanks entirely to the Internet, If you’re a reader and shopping from your keyboard, and hundreds of thousands of discounted items appeal to you, then we might interest you.

This is how Amazon opened up its operations on the web.

The Launch Of Amazon.com Associates

By July of 1996, as Amazon grew into one of the most popular domains on the web, it also announced a program called Amazon.com Associates. As Amazon explained at the time:

Through this program, any Web site, whether it attracts only a few visitors or hundreds of thousands of hits, can enhance its content and earn revenue by recommending books. More than 300 Web sites are currently enrolled as Amazon.com Associates, with dozens signing up daily.

They further explained:

With the Amazon.com Associates program, Web sites select books of interest to their visitors and link directly to the Amazon.com 1.1 million title catalogue. Amazon.com handles online ordering, credit card charging, customer service and shipping the books directly to customers. Amazon.com, already recognized as one of the leading electronic retailers, offers Associate customers the same discounted prices and service that has earned its reputation among Web users. Associate Web sites earn a referral fee for their book recommendations.

In short, while the affiliate business model was not new, Amazon had learned how to take advantage of it. And Jeff Bezos explained at the time:

By providing a referral fee for these recommendations, Amazon.com has developed an electronic business model that takes advantage of what the Web has to offer.

The IPO, The First Distribution Deals, And The First Legal Battle With Barnes And Nobles

As Amazon’s growth picked up further momentum, the company got ready for its IPO.

The original S-1 form, as Amazon got ready for its IPO.

As Amazon got ready for its IPO, it also started to close its first deals. Among the most important, Amazon closed a deal with Excite, and as explained:

The three-year relationship combines Excite’s core competencies in distribution and programming with Amazon.com’s strengths in bookselling and editorial content to offer consumers the opportunity to buy topic-related books while browsing Excite’s channels. Throughout Excite’s channels pages, Excite will offer users links that will take them directly to the related Amazon.com search results page. The full range of links is expected to be in place in the fourth quarter of 1997. Amazon.com’s advertising will begin running immediately throughout Excite’s popular topic-based channels at http://www.excite.com.

Amazon also closed another key deal with AOL, a deal that would place it on the most popular website on earth, at the time. As they explained back then:

Under the agreement, Amazon.com will receive a permanent “above-the-fold” front-screen button (visible without scrolling down) on the AOL.com homepage, the most visited site on the Web. This button will link users directly to Amazon.com (www.amazon.com), the leading online bookseller, where they will be able to review and purchase books.

In addition, Amazon.com and AOL will introduce a new navigational tool that will allow NetFind users to link directly to relevant Amazon.com search results pages through a hyperlink on every AOL NetFind Results page. By offering users additional in-context access to books at the time of their search, Amazon.com and AOL will enhance NetFind’s informational value and broaden user access to Amazon.com’s 2.5 million titles.

Furthermore, Amazon.com will have broad exclusive promotional placement rights on AOL.com and NetFind, including a range of banner advertisements on selected NetFind Review Category pages and keyword categories.

Amazon was closing distribution deals pretty much with the most important web players at the time, such as AltaVista, and then Netscape, which as explained:

In a related announcement today, Netscape unveiled its commerce strategy for Netcenter with the launch of Netscape Marketplace. Amazon.com will be one of the first commerce offerings that Netscape will provide to its Netscape Netcenter membership of busy professionals. “This agreement marks another important advance in our strategy to be the primary destination for all Internet bookbuyers,” said George Aposporos, Amazon.com Vice President of Business Development. “We are particularly excited about our relationship with Netscape because it secures Amazon.com’s place as the premier bookseller on the top three most highly trafficked sites on the Web.”

This was also the year that marked a fierce battle with Barnes & Noble. As Barnes & Noble took Amazon in court, for its “misleading” advertising as the “World’s Largest Bookseller” eventually the lawsuit was dismissed, and both companies agreed to compete in the marketplace.

And later that year, as Amazon announced its third-quarter results, it was clear the company was on a rocket ship growth trajectory. As Amazon announced at the time several initiatives were launched:

In September, Amazon.com launched major improvements to the Amazon.com store, including powerful new features that increase the benefits of online shopping. The new features include a state-of-the-art Recommendation Center; 22 subject-browsing areas; and the use of a proprietary technology, 1- Click(SM) ordering, to streamline the ordering process. These enhancements represent the largest-ever step forward in the company’s strategy of offering customers the easiest, most enjoyable, and most effective way to find their next book.

Amazon was pretty much anywhere. As it was the “premier bookseller” on AOL.com, Yahoo!, Netscape, Excite.com, the AltaVista Search Network, and the Prodigy Shopping Network.

To scale up its operations, by November 1997, Amazon opened its second distribution center. As Jeff Bezos highlighted at the time:

Now with distribution centers on both coasts, we can dramatically reduce order-to-mailbox time for Amazon.com customers everywhere

The same press release highlighted:

The new Delaware distribution center positions Amazon.com closer to its East Coast customers and provides immediate reductions in shipping times for many Amazon.com book buyers. The distribution center also brings the company closer to East Coast publishers, who benefit from faster shipping and receiving service.

This was the beginning of the Amazon’s scale up!

Amazon Scaling

As Amazon had proved itself in books, it was time to move on in new niches.

In the midst of the dot-com bubble, as Amazon grew its revenues at a double digits rate, it also started to acquire other businesses and in the process move to the most adjacent niche that Jeff Bezos had identified a few years back: Music.

By June 1998, Amazon.com opened up to music, with the following statement:

The leading online bookseller opened its music store at 1 a.m. today along with a major update of its award-winning Web site. The music store offers more than 125,000 music titles–10 times the number the average music store offers–at everyday savings of up to 40%, including 30% savings on the 100 bestselling Amazon.com CDs.

Jeff Bezos highlighted at the time:

It’s a music discovery machine, using the power of technology and the Internet, we’re enriching the music experience for everyone, from casual to devoted listeners alike.

As Amazon moved to music it used the same playbook it had used for books. It enlisted a militia of affiliates, who provided huge distribution to Amazon music products. In fact, by August of the same year, Amazon had over a hundred thousand affiliates!

David Risher, Amazon’s Vice President, in 1998, emphasized:

Amazon.com’s Associates program is the only major syndicated selling network in existence that enables participants to sell books, CDs, DVDs, and sheet music–giving them the potential to earn more than they could with any other program, the real winners, though, are the visitors to Associate Web sites who no longer have to keep track of multiple passwords, user IDs, and orders. With our cross-product program, visitors to Associate sites can purchase several titles across multiple product lines from a single source.

By October 1998, Amazon entered the European book market, starting from UK and Germany.

Get big fast

While the company was not profitable until 2001, Bezos noted that books were easy to source, package, and distribute.

With great business acumen, he noted that books would allow him to capitalize on the massive growth potential in online eCommerce. In fact, he believed online retailers would only be successful if they adopted the mantra “Get Big Fast” – a slogan Bezos had printed on company t-shirts.

To fund this strategy, Amazon held its IPO in May 1997 and managed to raise $54 million. The following year, it expanded its product range by selling computer games and music.

After several online bookstore acquisitions in Europe, the product range was extended once more to include consumer electronics, home improvement items, software, toys, and video games, among other things.

The rest, as they say, is history.

Amazon founder Jeff Bezos originally wanted the company to be called Cadabra. However, the idea was canned after lawyers noted its obscure reference to magic and possible confusion with the word “cadaver”.

Amazon’s original business model of selling books was derided by critics who suggested it could not compete with established players. To provide a point of difference, Bezos maintained a focus on customer convenience.

Amazon grew rapidly because Bezos identified how easily the sale of books could be scaled to achieve growth. This idea became a company mantra that is responsible for a large part Amazon’s success.

Surviving the dot-com bubble

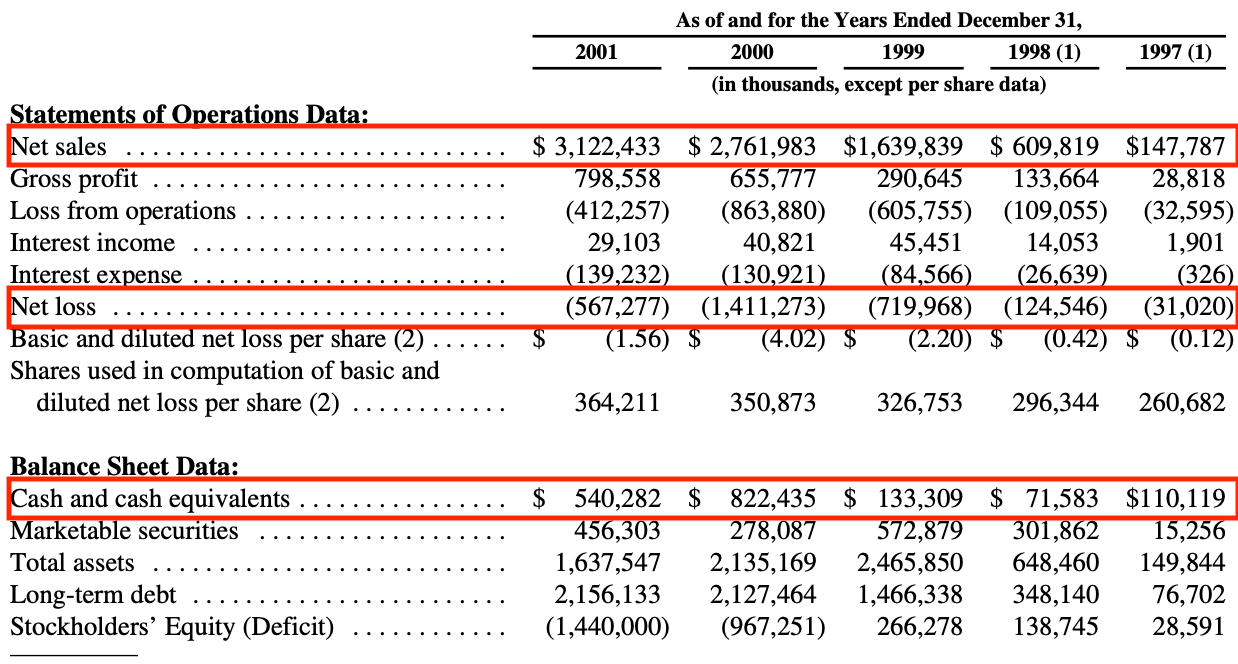

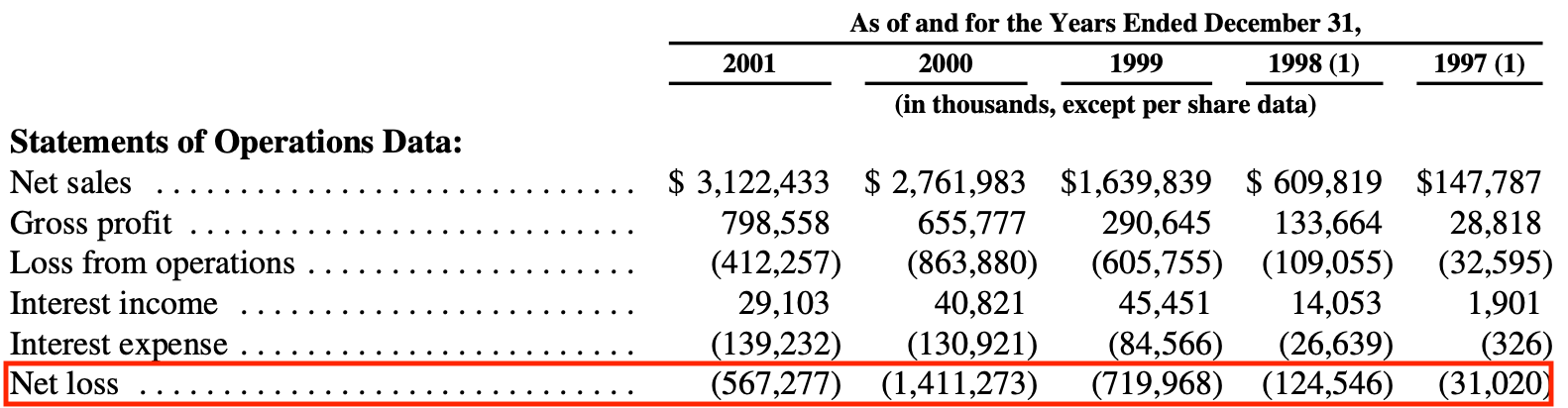

Since its inception in 1994, and its IPO in 1997, going to the 2000 dot.com bubble Amazon was not a profitable company. Indeed, as Amazon established itself as one of the strongest online brands, and the strongest bookstore online, already by 1996-1997, it quickly expanded to offer more and more, from DVD to any other item imaginable. That sort of expansion was driven to gain as quickly as possible market shares of, at the time, embryonic e-commerce market. Thus, Amazon lost money, year after year. Yet, the company still managed to generate positive cash flows, thanks to its positive cash conversion cycles and exponential revenue growth, until the dot-com bubble kicked in.

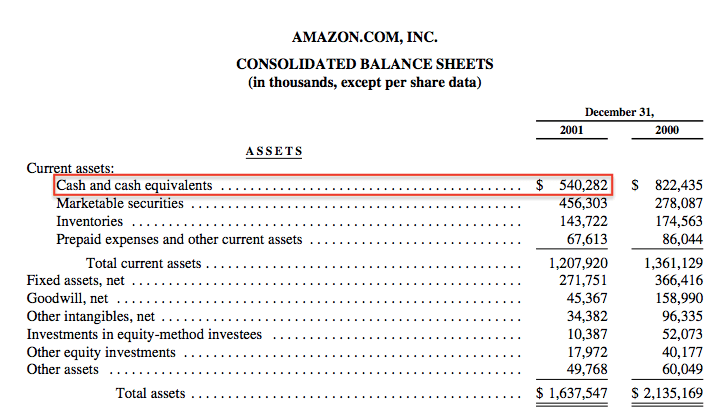

As Amazon revenue growth slightly slowed down, its cash generation also declined and from $822 million at the bank, in 2000, Amazon ended up with $540 million at the bank by 2001, thus burning over $280 million in cash.

Amazon pre-dot-com bubble

While at the time Amazon had already expanded in many categories and product types, it still didn’t think as a platform. Amazon was an incredibly successful e-commerce with a broad selection of items, low prices, discovery, the 1-Click technology, fulfillment, “look inside the book” feature, reviews, wish list and more.

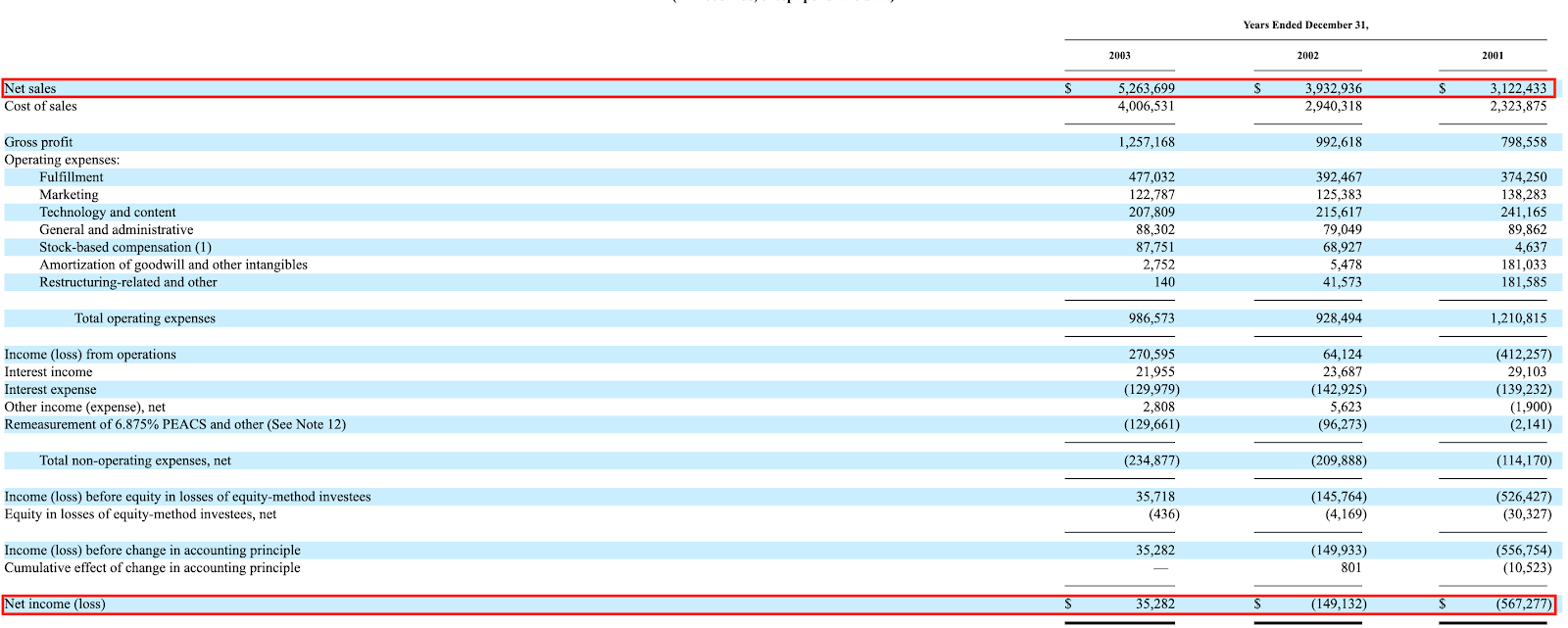

As we’ll see it would be only in 2001 that Amazon would start three core programs (Merchant@amazon.com Program, Merchant Program, Syndicated Stores Program), that would help Amazon gain substantial traction, with revenues moving from over $3.1 billion in 2001 to over $5.2 billion by 2003, and for the first time in its financial history (at least from its IPO) Amazon turned a profit and cash started to flow in again.

The near-death experience

During the 2000s with the explosion of the web, capital was flowing at a high rate. This was mostly a top-down approach where venture capitalists invested billions of dollars in companies hoping they would build something valuable. A simple idea coupled with a domain name was enough to spur excitement and inflated stock growth.

To have an idea of how gloomy was the scenario. As the Guardian highlighted in June 2000, in an article entitled “Amazon.bomb:“

Analyst Ravi Suria highlighted Amazon‘s “weak balance sheet, poor working capital management, and massive negative operating cashflow – the financial characteristics that have driven innumerable retailers to disaster through history.” It was a day during which Amazon‘s shares lost 20% of their value, and 51m of them changed hands. A company worth about $40bn (£25bn) just before Christmas had ended the day worth $12bn (£7.5bn), and things did not improve during trading yesterday.

At those comments, Jeff Bezos replied at the time:

Three years ago our stock was $1.50 a share, today it’s $30-something. There have been many, many days when our stock has gone up 20% in a day” – that laugh again – “and if stocks can go up 20% in a day, they can go down 20% in a day. All internet stocks are volatile, including Amazon.com… we are nowhere near running out of cash, and we are not at all worried about it.

And he was right. Even though the company had burned a few hundred million in cash in 2001.

It had managed to get a long-term loan of over six hundred million back in 2000, right before the explosion of the dot-com bubble. Thus, guaranteeing enough cash to go through that bad period.

Indeed, as of 2001, Amazon still had over five hundred millions of cash sitting in its bank account. To understand how bad Amazon reputation might have been at the time (of course not all agreed with that), an article dated April 26, 2001, by Doug Casey, author of “Crisis Investing,” highlighted:

I’ve said several times that Amazon is a cinch for bankruptcy, certainly Chapter 11 (a reorganization) and maybe even Chapter 7 (a liquidation), although I consider the latter a bit of a long shot.

Luck for sure played a key role. Amazon, like many other companies during the dot-com bubble, played with a very aggressive playbook skewed toward market domination and investing the whole resources brought back into the business for more aggressive growth and expansion. This became clear when, in 2000, Amazon found itself in a cash squeeze. The company was burning cash, and although one deal with AOL brought in an additional $100 million in cash as an investment into the company.

There was another event that saved Amazon from bankruptcy, and it happened a month before the dot-com crash. Amazon sold $672 million in convertible bonds to overseas investors and it did so at just the right time. Had Amazon waited just a bit longer it would have failed miserably.

Given the perfect timing of that capital raise, as the dot-com busted, investors also filed a class action against Amazon, that would be finally settled in 2005. It’s important to remark that many internet companies underwent lawsuits during that time, as the bubble burst, leaving off the table billions and billions of investors’ money.

That near-death experience taught Amazon to rehaul its whole playbook. It wasn’t any longer just about aggressive growth and expansion for its own sake, with an aggressive financial model where it was all about cash flows, but Amazon started to become more nimble and also to come up with programs such as Amazon websites (third-party) and many other programs that would lead to the success of the company.

Today Amazon praises itself as the most customer centric company on earth.

To understand also the shift on how Amazon spent money also in terms of product/technological development below a fragment from the Amazon financials back in 2001:

Technology and content expense was $241 million, $269 million and $160 million for 2001, 2000 and 1999, respectively, representing 8%, 10% and 10% of net sales for the corresponding periods, respectively. The decline in absolute dollars spent during 2001 in comparison to the prior year primarily reflect our migration to a technology platform that utilizes a less-costly technology infrastructure, as well as improved expense management and general price reductions in most expense categories, including data and telecommunication services, due to market overcapacity.

The paradigm shift

The turning point was 2001, after the dot-com bubble burst. Amazon realized it needed something to change its pace of growth. They stopped thinking in terms of a traditional business operating on the web and therefore using the web as a sales channel and they started to think of the web as a platform for business model change.

Thus they started to think in terms of ecosystem, so how do we enable other businesses on top of our platform? From there Amazon started to experiment some key programs that would not only enable the transition toward becoming a platform (most items sold on Amazon would be third-party) but also to develop later in the 2000s the cloud infrastructure that would evolve into AWS, today the most valuable part of the business, which is giving rise to another phenomenon, that of the AI company.

Back in the 2000s, Amazon opened up to brands like Toysrus.com, Inc., Target Corporation, Circuit City Stores, Inc., the Borders Group, Waterstones, Expedia, Inc., Hotwire, National Leisure Group, Inc., Virgin Wines, and others which further amplified Amazon’s brand.

If you could buy something from Target on Amazon, you would trust its brand more easily.

In 2001, we began marketing three services for third-party sellers that are designed to provide catalog retailers, physical store retailers and manufacturers with cost-effective e-commerce solutions and to expand the selection on our Websites for the benefit of our customers:

The third-party seller strategy started to work. And it showed how Amazon was leveraging on a platform business model to enhance its brand and business.

The third-party seller services strategy revolved around three core ones:

Merchant@amazon.com Program: here third party seller could offer their products on Amazon, either in its online stores or in a co-branded store on the Amazon site, or both. And they could also fulfill those thorough products Amazon by paying the company a fixed fee. Companies like Target and Toysrus were part of it.

Merchant Program: with which the third-party seller had its own URL and Amazon provide the option of providing fulfillment-related services on behalf of the third-party.

Syndicated Stores Program: which represented third-party seller’s e-commerce websites were offering products available on Amazon, which product were fulfilled by Amazon and the company paid commission to syndicated store.

The experiments that lead to becoming a tech giant

Some of the technologies that helped Amazon become a successful e-commerce company in the first place were the “1-click patent” and by 1999 Amazon had also launched its seller marketplace, that used to be called zShops, where sellers could sell their used merchandise.

While, the turning point came by 2003, when Amazon launched web hosting services, that would become AWS, in reality, the real turning point was in the 2000, when Amazon started to order their jumbled mess to offer third party to build their sites on top of Amazon, what was known at the time as Merchant.com.

What you may not know is that the roots for the idea of AWS go back to the 2000 timeframe when Amazon was a far different company than it is today — simply an e-commerce company struggling with scale problems. Those issues forced the company to build some solid internal systems to deal with the hyper growth it was experiencing — and that laid the foundation for what would become AWS.

It’s exciting to see Amazon Web Services, a $20 billion revenue run rate business, accelerate its already healthy growth. AWS has also accelerated its pace of innovation – especially in new areas such as machine learning and artificial intelligence, Internet of Things, and serverless computing. In 2017, AWS announced more than 1,400 significant services and features, including Amazon SageMaker, which radically changes the accessibility and ease of use for everyday developers to build sophisticated machine learning models. Tens of thousands of customers are also using a broad range of AWS machine learning services, with active users increasing more than 250 percent in the last year, spurred by the broad adoption of Amazon SageMaker. And in November, we held our sixth re:Invent conference with more than 40,000 attendees and over 60,000 streaming participants.

Amazon’s mindset

As Jeff Bezos recounted back in 2006, “many of the important decisions we make at Amazon.com can be made with data. There is a right answer or a wrong answer, a better answer or a worse answer, and math tells us which is which. These are our favorite kinds of decisions.”

Indeed, opinion and judgment, in that case, mattered way more. As Jeff Bezos recounted in 2006:

As our shareholders know, we have made a decision to continuously and significantly lower prices for customers year after year as our efficiency and scale make it possible. This is an example of a very important decision that cannot be made in a math-based way. In fact, when we lower prices, we go against the math that we can do, which always says that the smart move is to raise prices. We have significant data related to price elasticity. With fair accuracy, we can predict that a price reduction of a certain percentage will result in an increase in units sold of a certain percentage. With rare exceptions, the volume increase in the short term is never enough to pay for the price decrease. However, our quantitative understanding of elasticity is short-term. We can estimate what a price reduction will do this week and this quarter. But we cannot numerically estimate the effect that consistently lowering prices will have on our business over five years or ten years or more. Our judgment is that relentlessly returning efficiency improvements and scale economies to customers in the form of lower prices creates a virtuous cycle that leads over the long term to a much larger dollar amount of free cash flow, and thereby to a much more valuable Amazon.com. We’ve made similar judgments around Free Super Saver Shipping and Amazon Prime, both of which are expensive in the short term and—we believe—important and valuable in the long term.

More, in particular, the paper highlighted how, when an institution made decisions, primarily based on data and math, that made them take efficient operating decisions. Yet, as long-term, strategic and “unstructured” (based on processes that have not been encountered in quite the same form and for which no predetermined and explicit set of ordered responses in the organization) decisions, might not rely on quantitative understanding, will get underestimated.

That happens, because decisions that can be taken on a quantitative basis can be measured, thus institutions but also companies and managers in the field focus too much on measurable analyses. Yet those decisions might be good for the short-term. They might prevent an organization from focusing on long-term, hard and strategic decisions. Amazon, a company that relied over and over again on quantitative analysis of things that could be measured, optimized and maximized. Also relied a lot on judgment, opinion, and human decision-making when it came to long-term, strategic decisions that could not be based on previous experience or scenarios, but needed to be tackled. This point is very important. In a world of management that focuses more and more on the quantifiable, and measurable. Getting data-driven might mean losing the strategic focus.

Amazon laid out the foundation of its decision-making process, based on few key principles, defined in 1997, in the first Shareholders letter:

We will continue to focus relentlessly on our customers.

We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.

We will continue to measure our programs and the effectiveness of our investments analytically, to jettison those that do not provide acceptable returns and to step up our investment in those that work best. We will continue to learn from both our successes and our failures.

We will make bold rather than timid investment decisions where we see a sufficient probability of gaining market leadership advantages. Some of these investments will pay off, others will not, and we will have learned another valuable lesson in either case.

Amazon’s renewed business playbook

In the annual letter of 2001, Jeff Bezos highlighted:

When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.

And he continued:

Why focus on cash flows? Because a share of stock is a share of a company’s future cash flows, and, as a result, cash flows more than any other single variable seem to do the best job of explaining a company’s stock price over the long term.

Therefore, even though Amazon did survive the dot-com bubble, the business model which would enable the company to make it through the first phase of scale-up was drafted around the beginning of the year 2000, right at the bottom of the dot-com bubble.

In short, even though Amazon emphasized so much on cash flows, during the dot-com, the company was burning a substantial amount of cash. And Amazon itself still saw the web as a distribution platform, rather than a business model enabler.

Therefore, Amazon‘s survival through that period was nonetheless due to a bit of lack. However, Jeff Bezos led Amazon through that period with vision and extreme passion, and he kept pushing the company to a new business model.

A quick summary of the Amazon business model

Amazon was profitable in 2023. On nearly $575 billion in revenue for 2023, Amazon generated a net profit of over $30 billion. Since 2014, Amazon hasn’t recorded a net loss, but it did record a net loss of over $2.7 billion in 2022, while it recouped that in 2023. Indeed, in 2014, Amazon reported a net loss of $241 million, and it would be profitable until 2021. In 2022, Amazon turned unprofitable again and highly profitable again in 2023.

Started in 1994 as a bookstore, Amazon soon expanded and became the everything store. While the company’s core business model is based on its online store. Amazon launched its physical stores, which generated already over five billion dollars in revenues in 2017.

Amazon Prime (a subscription service) also plays a crucial role in Amazon’s overall business model, as it makes customers spend more and being more loyal to the platform. Besides, the company also has its cloud infrastructure called AWS, which is a world leader and a business with high margins.

Amazon also has an advertising business worth a few billion dollars. Thus, the Amazon business model mix looks like many companies in one. Amazon measures its success via a customer experience obsession, lowering prices, stable tech infrastructure, and free cash flow generation.

In 2023, Amazon generated nearly $575 billion in revenues, broken down as follows, where you can also appreciate the growth trajectory of each segment:

Amazon generated over half a trillion dollars in revenue in 2023, of which $231.87B from online stores, over $140.05B from third-party seller services, $90.76B from AWS, $46.9B from advertising, $40.21B from subscription services, $20.03B billion in physical stores, and $4.96B from other sources.

Amazon’s business model in a nutshell

Amazon is the largest marketplace on earth. Even though the United States represented the primary source of income for Amazon. It is expanding globally. Indeed, net sales have increased since 2014. In 2016 products represented almost 70% of total sales. Services sales have been growing at a fast pace.

In terms of operating income, the growth has been mainly driven by the high margins derived from service sales.

By looking more in-depth at the revenue sources, subscription and AWS services have been growing.

That denotes how Amazon is expanding globally by moving more and more toward services (like Prime subscription and AWS).

Amazon, according to Jeff Bezos’ vision

Amazon fundamental principles that drove and drive the company are:

Customer Obsession

Ownership

Invent and Simplify

Are Right, A Lot

Learn and Be Curious

Hire and Develop the Best

Insist on the Highest Standards

Think Big

Bias for Action

Frugality

Earn Trust

Dive Deep

Have Backbone; Disagree and Commit

Deliver Results

At times a great place to start to understand the business models of a startup it isn’t necessarily its financials but rather how the founder sees its baby. In fact, for any founder a la Jeff Bezos its company has been nurtured just like a baby.

Of course, the founders’ vision of their company can also be biased. In which case the perception of the company according to its founder and how the public perceives it might have a wide gap.

However, it is a useful exercise to look at the shareholder’s letters if you want to understand the past, present, and future of any company.

For Jeff Bezos, that means avoiding decline or extreme slow motion and pushing for more each day.

As he put it:

Day 2 is stasis. Followed by irrelevance. Followed by excruciating, painful decline. Followed by death. Andthatis why it isalwaysDay 1.

He has four main metrics to assess whether his company is on Day One, or is falling toward Day Two:

1. Customer obsession,

Customer obsession goes beyond quantitative and qualitative data about customers, and it moves around customers’ feedback to gather valuable insights. Those insights start by the entrepreneur’s wandering process, driven by hunch, gut, intuition, curiosity, and a builder mindset. The product discovery moves around a building, reworking, experimenting, and iterating loop.

You can be competitor focused, you can be product focused, you can be technology focused, you can be business model focused, and there are more. But in my view, obsessive customer focus is by far the most protective of Day 1 vitality.

2. A skeptical view of proxies,

As companies get larger and more complex, there’s a tendency to manage to proxies.

What does that mean?

A common example is process as proxy. Good process serves you so you can serve customers. But if you’re not watchful, the process can become the thing. This can happen very easily in large organizations…

…The process is not the thing. It’s always worth asking, do we own the process or does the process own us?

3 The eager adoption of external trends,

The outside world can push you into Day 2 if you won’t or can’t embrace powerful trends quickly. If you fight them, you’re probably fighting the future. Embrace them and you have a tailwind…

…We’re in the middle of an obvious one right now: machine learning and artificial intelligence.

4. High-velocity decision making.

Day 2 companies make high-quality decisions, but they make high-quality decisions slowly. To keep the energy and dynamism of Day 1, you have to somehow make high-quality, high-velocity decisions…

…First, never use a one-size-fits-all decision-making process…

…Second, most decisions should probably be made with somewhere around 70% of the information you wish you had…

Third, use the phrase “disagree and commit.” … “Look, I know we disagree on this but will you gamble with me on it? Disagree and commit?”

Putting it all together

Jeff Bezos offers a portrait of Amazon which is useful to understand its business model deeply. First, it all starts with Day One.

This, to me, is a way for Amazon to keep a “start-up mindset” also if it has become a large organization. It means focusing on customers, therefore, experimenting with new product lines, services, or anything that might become “delightful” to the public.

In fact, once Amazon does identify strong trends, rather than fight them it embraces them. One example is how nowadays Amazon is using AI and machine learning as the main propellers for its business growth.

In other words, practically speaking this makes Amazon fluid. Thus, the Amazon of tomorrow might have a different face – but the same soal – compared to the Amazon of today.

How does Amazon’s business work?

Amazon runs a platform business model as a core model with several business units within. Some units, like Prime and the Advertising business, are highly tied to the e-commerce platform. For instance, Prime helps Amazon reward repeat customers, thus enhancing its platform business. Other units, like AWS, helped improve Amazon’s tech infrastructure.

Amazon is a giant marketplace where each day billions of people find anything from the latest best selling book to things like Nicolas Cage pillowcase.

Amazon’s main metrics as per SimilarWeb

According to the Similar Web estimates each day, only in the US Amazon has over 2 billion visits. On average those people spend more than six minutes on the site and look at almost nine pages purchasing what they’re looking for.

That makes Amazon the fourth most popular site in the US. The Amazon business model revolves around four main players:

We serve consumers through our retail websites and focus on selection, price, and convenience. We design our websites to enable hundreds of millions of unique products to be sold by us and by third parties across dozens of product categories. Customers access our websites directly and through our mobile websites and apps. We also manufacture and sell electronic devices, including Kindle e-readers, Fire tablets, Fire TVs, and Echo, and we develop and produce media content. We strive to offer our customers the lowest prices possible through low everyday product pricing and shipping offers, and to improve our operating efficiencies so that we can continue to lower prices for our customers. We also provide easy-to-use functionality, fast and reliable fulfillment, and timely customer service. In addition, we offer Amazon Prime, an annual membership program that includes unlimited free shipping on tens of millions of items, access to unlimited instant streaming of thousands of movies and TV episodes, and other benefits.

Sellers

We offer programs that enable sellers to grow their businesses, sell their products on our websites and their own branded websites, and fulfill orders through us. We are not the seller of record in these transactions. We earn fixed fees, a percentage of sales, per-unit activity fees, interest, or some combination thereof, for our seller programs.

Developers and enterprises

We serve developers and enterprises of all sizes, including start-ups, government agencies, and academic institutions, through our AWS segment, which offers a broad set of global compute, storage, database, and other service offerings.

Content creators

We serve authors and independent publishers with Kindle Direct Publishing, an online service that lets independent authors and publishers choose a 70% royalty option and make their books available in the Kindle Store, along with Amazon’s own publishing arm, Amazon Publishing. We also offer programs that allow authors, musicians, filmmakers, app developers, and others to publish and sell content.

An effective business model to work properly has to involve and generate value for several stakeholders. That applies to the Amazon business model as well.

In fact, when I get into the Amazon marketplace as a consumer, I can find anything across dozens of product categories.

Among those, I can also buy Amazon products (like Kindle, and Echo), or subscribe to Prime (to get faster delivery and even access to an on-demand library of contents).

Also, thanks to the Amazon seller program the company earns fixed fees, a percentage of sales, per-unit activity fees, interest, or some combination of those based on the transactions generated by the marketplace; Although AWS is a platform of its own. Nonetheless, it has a strategic role in Amazon.

Last but not least, the KDP platform allows thousands of independent authors to publish their e-books and info-products. According to the plan in which the independent author enrolls into Amazon will earn anywhere from 30-70% of royalty fees from the sales.

Like all the other tech giants Amazon could create such a robust business model that it now works as the main engine for the dominance of the company in the next decade.

As technology becomes more and more competitive business models lose effectiveness. However, a business model well-designed can make a company capture value for a long time!

How does Amazon make money?

It’s time to dive into the numbers to understand how the company works. When trying to understand a business model, the revenues are a good starting point.

But it’s also important to look at other financial metrics to deeply understand what’s the real cash cow.

In fact, it’s easy to be fooled to believe a company falls into a specific business model. However, numbers don’t lie. Where does Amazon stand?

According to the infographic, you can see that Amazon makes most of its revenues from the sales of products. However, those product sales also have high costs. Thus, the margins Amazon makes on them is thin.

Instead, if we look at the operating income, you can see how this is fueled by the services, which comprise seller services, AWS, and subscription services.

In other words, by looking at the revenue, you might be fooled to think that Amazon is in the product business, just like Apple, yet there is a slight difference between the two companies!

Amazon vs. Apple

Like many things in business, so revenue generation seems to follow a power law. You try quite many things, but you end up with one reliable and sustainable source of income after all. Sometimes the differences in business models are subtle.

Take Apple and Amazon. As they generate most of their revenues from “products” one might think they have the same business model.

However, with a more in-depth look your realize their model is entirely different. In fact, while Apple sells its iPhone at a high margin, Amazon sells its products at a thin margin (in fact, the cost of sales for Amazon is almost as high as the revenue generated by its products).

In short, Amazon seems to use its products to ramp up its services revenues, which seems to be the real cash cow. However, if you look at revenues alone, you might be fooled to believe Amazon is in the “product” business.

Let’s give a look at the Amazon business model from several perspectives. The aim is to have an overview of Amazon that goes beyond the conventional wisdom that Amazon is a product company, it’s much more than that!

Amazon vs. Google

Google and Amazon are fighting for dominance between e-commerce and advertising. Where Google has a monopoly in the search market. Amazon might gain a monopoly in product searches. In 2020, Google opened its Google Shopping for free to contrast Amazon dominance on e-commerce and prevent Amazon from taking more space in the digital advertising industry, the core business fo Google.

A deep look at the business dynamics of the Amazon business model

Beyond the look, we have given so far at the Amazon Business Model, I want to give you an in-depth look so that you can really appreciate how the Amazon business model works and what powers up its business engine.

Amazon revenue model

Amazon’s business model follows both a B2C and B2-B distribution strategy. Indeed, on the one hand, its e-commerce platform is consumer-facing, providing millions of products to billions of users around the world. While its e-commerce platform is also used by other businesses, called third-party stores to sell their own products on top of Amazon.

If we look at the Amazon revenue model, a few things pop up right away. As we saw the online stores are still the core part of the business.

However, the core business is the foundation for other emerging businesses that run with different logic to its online stores. Where online stores run at tight margins and high volume by taking advantage of cash conversion cycles.

Other parts of the Amazon business model, like Amazon Advertising Services, Amazon Prime, and Amazon AWS run with much higher margins. Thus, Amazon’s online stores are the foundation for those other businesses that make the overall company more profitable in the long run.

Let’s give a look at the Amazon cash machine, which is the foundation of its ability to expand, and disrupt other industries, while expanding in other areas.

Amazon’s cash machine

One of the key elements of the Amazon business model is its cash machine business strategy. In short, Amazon has operated (and still does) for years at very tight profit margins on its online store.

The company has willingly done so throughout the years, as it made its prices low, convenient compared to traditional physical stores, and with a fast and efficient delivery system, what Amazon calls fulfillment centers.

This might give the impression that Amazon doesn’t generate enough cash flow to its business. However, that’s quite the opposite. As Amazon collects payments quickly from its customers, it then pays its vendors with relatively longer payment terms.

This gives Amazon short-term liquidity that can invest back to speed up growth. With this mechanism, Amazon has been able to disrupt several industries. Starting as a bookstore online, it quickly expanded to all the other industries.

One Amazon has built the most valuable two-sided marketplace on earth it has become way easier for the company to offer many other services.

Amazon advertising business

Amazon more than doubled its advertising revenues from the first nine months of 2017, compared to 2018. Indeed, the revenues went from $2.92 billion in 2018 to $6.72 billion in 2018. Compared to Facebook $38.37 billion and Google $83.68 billion for the same period, Amazon is still a small player. However, if we take into account that Amazon runs a diversified business model, with several revenue streams, it also gives the company more space to experiment with advertising!

A few people realize among other businesses, Amazon has become a digital advertising provider. And not a small one, but among the very few able to compete against the duopoly Google-Facebook.

Indeed, as of the first months of 2018, the Amazon advertising business netted over six billion in revenues!

With such an infrastructure and many e-commerce hosted on Amazon infrastructure, more and more entrepreneurs and marketers are willing to pay for Amazon advertising services.

This part of the business has higher margins compared to the tight margins of the online stores.

Yet, this growth hasn’t stopped here. Indeed, Amazon advertising revenues spiked to over $30 billion in 2021. In part, this is given by Amazon’s ability to capture commercially relevant traffic and on the other hand, also on the doubled down effort of Amazon to make sponsored content available on top of its platform.

Indeed, in 2022, Amazon is expanding the availability of sponsored content on its platform. Therefore, we can expect the digital advertising segment to keep growing at an incredible pace.

Amazon Prime

Many companies nowadays have shifted to the subscription business model. Amazon has converted part of its business to accommodate this change.

Amazon Prime is a critical element of Amazon’s growth strategy. The logic is simple, the more people join the Prime Memberships, the more products they purchase on the online stores.

Indeed, with Prime, members enjoy faster delivery services besides the access to Amazon’s original content offered via streaming. This subscription model also creates a more stable and predictable income over time.

Amazon AWS

Amazon AWS follows a platform business model that gains traction by tapping into network effects. Born as an infrastructure built on top of Amazon’s infrastructure, AWS has become a company offering cloud services to thousands of clients from the enterprise level, to startups. And its marketplace enables companies to connect to other service providers to build integrated solutions for their organizations.

Started as an experiment back in 2000, the Amazon AWS has grown to become an over seventeen billion dollars business in 2017. AWS also enjoys higher margins and network effects.

Amazon is doubling down on that as this business unit will be critical to its future success.

Coopetition describes a recently modern phenomenon where organizations both compete and cooperate, which is also known as cooperative competition. A recent example is how Netflix streaming platform has been among the major customers of Amazon AWS cloud infrastructure, while Amazon Prime has been among the competitors of Netflix Prime content platform.

It’s important to notice how AWS managed to keep high operating margins over the years. However, as the competition toward cloud computing gets harder, and as AI gets commoditized (AWS like all the other cloud players is working as the underlying infrustructure for the web and also as the underlying platform for the AI-powered web), it might be normal to assist to a decrease in margins.

Amazon virtuous cycle

Back in 2001, Jeff Bezos sketched on a piece of paper a flywheel that would become Amazon’s key marketing strategy for years to come. The Amazon Flywheel or Amazon Virtuous Cycle is a strategy that starts from customer experience to drive traffic to the platform, which traffic gets monetized via Amazon’s selection of products and by inviting third-party sellers to join the platform.

That improves the selection of goods, which Amazon would have taken years to build. In turn, the customer experience improves further. At the same time, Amazon uses the cash generated to further improve its cost structure. Rather than distribute the additional cash to shareholders the company passes it on to customers via lower prices.

This process contributes even further to the virtuous cycle which makes Amazon expand and take over other industries. This marketing strategy has been used in the first years by Amazon to expand its operations.

Understanding Amazon’s financial model

Amazon was profitable in 2023. On nearly $575 billion in revenue for 2023, Amazon generated a net profit of over $30 billion. Since 2014, Amazon hasn’t recorded a net loss, but it did record a net loss of over $2.7 billion in 2022, while it recouped that in 2023. Indeed, in 2014, Amazon reported a net loss of $241 million, and it would be profitable until 2021. In 2022, Amazon turned unprofitable again and highly profitable again in 2023.

For years, analysts have been puzzled by Amazon’s business model. They saw a lack of profitability, an exponential price-to-earnings ratio, and many assumed it was all a bubble.

However, from a better look, that is how Amazon has always been structured. The company, rather than focusing on pushing profit margins, pushed to generate cash flows (we saw it in the cash machine model) that could reinvest as much as possible in the growth of the business, by being in a sort of continuous blizscaling-mode.

While today Amazon’s marginality has improved substantially, that is primarily due to other segments (AWS, Prime, and other revenue streams), while online e-commerce still generates higher margins compared to the other revenue streams.

That is part of Amazon’s mission to keep a wide variety of things, by offering low prices.

Analyzing Amazon’s Digital Distribution

If we look into Amazon’s digital distribution, based on the data from SimilarWeb, it’s important to emphasize a few key points:

Amazon has a very strong digital brand, as shown from the fact that direct traffic still represents most of the composition of the traffic toward Amazon.

Amazon also enjoys great engagement metrics. A platform with over 2 billion visits per month, each visit usually lasts more than six minutes, and an average user navigates through 8-9 pages on Amazon!

Also, Amazon enjoys a strong demand from the US, which is still the main market for its digital distribution.

And the Amazon shopping platform is still among the most successful when it comes to shopping, also compared to major websites, like Google.com and YouTube.

Of course, as Amazon became more successful over the years, this also opened the way to competitors. Below are the top alternatives in terms of traffic affinity to Amazon.com:

Summary and Conclusions

Amazon is a tech giant. When it started back in the 1990s, it began as an online bookstore. Today Amazon is the store that sells anything imaginable. As its founder, Jeff Bezos has specified Amazon is a customer-centric company.

However, it is clear that what made and makes Amazon so compelling is the business model and which generates value for several players.

Consumers find products at a lower price and get them fast. Sellers can find new market opportunities or decide not to carry any inventory. In fact, Amazon has its own fulfillment center that manages the inventories for sellers.

Thus, that makes it easier for anyone willing to start an online store to have lower barriers to entry. Developers and enterprises can rely on AWS cloud services.

Content creators can effectively monetize their info products through programs like KDP. And customers can consume Amazon’s original content via Amazon Prime.

Even though Amazon makes almost 70% of its revenues through product sales. In reality that part of the business is the foundation to grow other more profitable segments.

From Prime, Advertising, and AWS, thanks to its cash machine Amazon has been able to create a diversified business model.

Thus, who are thinking of Amazon as just an online store has been fooled by its revenues, but have not bothered to look at how its business model really works!

Amazon shows us a valuable lesson. For how much we like to categorize things under fixed, immutable categories and definitions.

Often, a company to become a multi-billion enterprise has to create a hybrid business model that takes advantage of several revenues and business models at once.

Take Google, it started as a search engine with an advertising business model, yet it is now diversifying in other areas.

In fact, even though 86% of Google’s revenues still come from advertising in 2017, Google makes money in many other ways.

What organizational structure does Amazon run?

The Amazon organizational structure is predominantly hierarchical with elements of function-based structure and geographic divisions. While Amazon started as a lean, flat organization in its early years, it transitioned into a hierarchical organization with its jobs and functions clearly defined as it scaled.

Is Amazon a digital advertising player?

Amazon has been ramping up its advertising business, and in the last few years, it has become one of the key players in the digital advertising landscape. Indeed, it has become larger than YouTube, with over $31 billion in ad revenues generated in 2021, alone. Amazon has a huge advantage over other players, as it intercepts the commercial intents of billions of users across the world, thus easily converting that traffic into sales, on top of its e-commerce platforms, to sell both first and third-party products.

Amazon has a diversified business model, with several business units. From the Amazon e-commerce platform both selling Amazon-owned products, to third party products, hosted on the platform. Amazon also provides fulfillment services to these third-party sellers. Complementary to that there is Amazon Prime, a streaming subscription service, which also gives subscribers faster delivery of goods from the platform, and Amazon advertising, which enables third-party sellers to sponsor their products on the platform. On the other hand, Amazon AWS is an enterprise cloud business serving small, medium, and large-sized organizations.

How many business models does Amazon have?

Amazon has five main business models types running in parallel. In fact, Amazon is 1. An e-commerce company serving consumers by offering its own products and third-party sellers’ products. 2. Amazon also is an Enterprise Cloud Platform with AWS. 3. The company also runs Subscriptions with Prime. 4. And Advertising on the platform for third-party sellers. 5. The company also produces hardware Products such as voice assistant, Alexa, the ebook reader Kindle, and more.

How does Amazon work as a business?

Amazon is primarily a platform business model, which makes money by selling its own products, or by collecting a percentage of revenues from third-party products sold on the platform. The company also makes money through advertising. And its AWS Enterprise Cloud Platform makes money through subscription services, pay as you go, and more.

Amazon’s mission statement is to “serve consumers through online and physical stores and focus on selection, price, and convenience.” Amazon’s vision statement is “to be Earth’s most customer-centric company, where customers can find and discover anything they might want to buy online, and endeavors to offer its customers the lowest possible prices.”

In the Amazon Shareholders’ Letter for 2018, Jeff Bezos analyzed the Amazon business model, and it also focused on a few key lessons that Amazon as a company has learned over the years. These lessons are fundamental for any entrepreneur, of small or large organization to understand the pitfalls to avoid to run a successful company!

With 64,588,418 shares, Jeff Bezos is the primary individual investor. Owning 12.7% of the company. Other top individual investors include Amazon’s CEO Andy Jessy, who has 94,729 shares. Top institutional investors include mutual funds like The Vanguard Group (6.6% ownership) and BlackRock (5.7% ownership).

Amazon generated over half a trillion dollars in revenue in 2023, of which $231.87B from online stores, over $140.05B from third-party seller services, $90.76B from AWS, $46.9B from advertising, $40.21B from subscription services, $20.03B billion in physical stores, and $4.96B from other sources.

Amazon was profitable in 2023. On nearly $575 billion in revenue for 2023, Amazon generated a net profit of over $30 billion. Since 2014, Amazon hasn’t recorded a net loss, but it did record a net loss of over $2.7 billion in 2022, while it recouped that in 2023. Indeed, in 2014, Amazon reported a net loss of $241 million, and it would be profitable until 2021. In 2022, Amazon turned unprofitable again and highly profitable again in 2023.

Amazon AWS follows a platform business model that gains traction by tapping into network effects. Born as an infrastructure built on top of Amazon’s infrastructure, AWS has become a company offering cloud services to thousands of clients from the enterprise level, to startups. And its marketplace enables companies to connect to other service providers to build integrated solutions for their organizations.

Amazon subscription revenue in 2023 was over $40 billion, compared to over $35 billion in 2022 and nearly $32 billion in 2021. Amazon Prime grew from a $4.5 billion revenue segment in 2015 to an over $40 billion segment in 2023.

The Amazon Working Backwards Method is a product development methodology that advocates building a product based on customer needs. The Amazon Working Backwards Method gained traction after notable Amazon employee Ian McAllister shared the company’s product development approach on Quora. McAllister noted that the method seeks “to work backwards from the customer, rather than starting with an idea for a product and trying to bolt customers onto it.”

The Amazon Flywheel or Amazon Virtuous Cycle is a strategy that leverages on customer experience to drive traffic to the platform and third-party sellers. That improves the selections of goods, and Amazon further improves its cost structure so it can decrease prices which spins the flywheel.

In the letter to shareholders in 2016, Jeff Bezos addressed a topic he had been thinking quite profoundly in the last decades as he led Amazon: Day 1. As Jeff Bezos put it “Day 2 is stasis. Followed by irrelevance. Followed by excruciating, painful decline. Followed by death. And that is why it is always Day 1.”

A regret minimization framework is a business heuristic that enables you to make a decision, by projecting yourself in the future, at an old age, and visualize whether the regrets of missing an opportunity would hunt you down, vs. having taken the opportunity and failed. In short, if taking action and failing feels much better than regretting it, in the long run, that is when you’re ready to go!

A network effect is a phenomenon in which as more people or users join a platform, the more the value of the service offered by the platform improves for those joining afterward.

A platform business model generates value by enabling interactions between people, groups, and users by leveraging network effects. Platform business models usually comprise two sides: supply and demand. Kicking off the interactions between those two sides is one of the crucial elements for a platform business model’s success.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.