PayPal owns Venmo. Indeed, since 2002, PayPal has acquired several brands. In 2013, as PayPal indirectly bought Braintree, it also bought Venmo. Braintree acquired Venmo in 2012 for $26.2 million. Therefore, by 2013, Venmo entered the PayPal family of brands comprising payment solutions like Braintree, Venmo, Xoom, and iZettle products.

Detail

Description

Company

Venmo

Ownership Structure

Wholly owned subsidiary

Parent Company

PayPal Holdings, Inc.

Acquisition Date

December 2013 (through Braintree acquisition by PayPal)

Founding Date

2009

Founders

Andrew Kortina and Iqram Magdon-Ismail

Headquarters

New York City, New York, USA

Primary Business

Peer-to-peer payment service, mobile payment app

Strategic Goals

Expanding user base, enhancing payment features, integrating with PayPal’s ecosystem, and promoting secure and seamless transactions

Corporate Structure and Ownership: Venmo is a wholly owned subsidiary of PayPal Holdings, Inc. PayPal acquired Venmo as part of its acquisition of Braintree in December 2013. Braintree, a mobile payment system, had acquired Venmo earlier in 2012 for $26.2 million. When PayPal acquired Braintree for $800 million, it brought Venmo under its corporate umbrella. This acquisition allowed PayPal to integrate Venmo’s popular peer-to-peer payment service into its portfolio, expanding its reach in the mobile payments market.

History and Evolution: Venmo was founded in 2009 by Andrew Kortina and Iqram Magdon-Ismail. The idea for Venmo was born out of the founders’ frustration with traditional payment methods and their desire to simplify peer-to-peer payments. Venmo quickly gained popularity, particularly among younger users, for its ease of use, social features, and the ability to split bills and make payments with friends. The app allows users to link their bank accounts, debit cards, or credit cards to send and receive money. Venmo’s integration of social media-like features, such as transaction notes and public feeds, set it apart from other payment apps.

Business Model and Revenue Streams: Venmo operates as a free service for users to send and receive money, with revenue generated through various channels:

Transaction Fees: Venmo charges a fee for instant transfers to bank accounts and for payments made using credit cards.

Merchant Services: Venmo allows users to make purchases with participating merchants and charges businesses a transaction fee for processing these payments.

Venmo Debit Card: Venmo offers a branded debit card linked to users’ accounts, generating interchange fees from transactions.

Cash Back Rewards: The Venmo debit card includes a cash-back program, creating partnerships with merchants and offering users incentives.

Integration with PayPal’s Ecosystem: As part of PayPal, Venmo benefits from integration with PayPal’s extensive payment infrastructure and global reach. This integration allows Venmo to leverage PayPal’s technology, security features, and financial services to enhance its offerings. PayPal’s ecosystem includes online payments, digital wallets, and merchant services, providing Venmo with additional avenues for growth and innovation. Venmo’s ability to tap into PayPal’s resources has helped it expand its user base and develop new features to meet the evolving needs of its users.

Product Features and User Experience: Venmo’s core features include easy money transfers, social feeds for transactions, and the ability to split bills and request payments. The app emphasizes user convenience and security, with features such as:

Instant Transfers: Users can instantly transfer funds to their bank accounts for a small fee.

Venmo Debit Card: A Mastercard-branded debit card that allows users to spend their Venmo balance at any location that accepts Mastercard.

Crypto Support: Venmo allows users to buy, hold, and sell cryptocurrencies directly within the app.

Business Profiles: Venmo offers profiles for small businesses, enabling them to receive payments from customers.

Security and Compliance: Venmo prioritizes security and compliance, implementing measures to protect user data and transactions. The app uses encryption to safeguard sensitive information and offers features like multi-factor authentication for added security. Venmo complies with financial regulations and works closely with regulatory bodies to ensure its services meet legal requirements. The company continually updates its security protocols to address emerging threats and provide a safe environment for users to conduct transactions.

Market Position and Competition: Venmo is a leading player in the peer-to-peer payment market, particularly popular among younger demographics in the United States. The app competes with other payment services such as Zelle, Cash App, and Apple Pay Cash. Venmo’s strong brand recognition, user-friendly interface, and social features have helped it maintain a competitive edge. The app’s integration with PayPal and its focus on innovation and user experience position it well to continue growing in the competitive payments landscape.

Leadership and Governance: Venmo operates under the leadership of PayPal’s executive team, with key figures overseeing its strategic direction and operations. Dan Schulman, President and CEO of PayPal, plays a crucial role in guiding Venmo’s growth and integration within PayPal’s ecosystem. The company’s leadership emphasizes innovation, security, and user satisfaction, driving Venmo’s efforts to enhance its services and expand its market presence. Venmo’s governance structure ensures alignment with PayPal’s broader objectives while maintaining its unique brand identity and focus on peer-to-peer payments.

Aspect

Description

Analysis

Examples

Products and Services

Venmo primarily offers a mobile app that allows users to send and receive money easily among friends and contacts. It supports P2P transactions, splitting bills, and making payments for various purposes, including rent, utilities, and shared expenses. Venmo also provides a Venmo Card, a physical debit card linked to the user’s Venmo balance, enabling spending at physical stores and online retailers. Additionally, the app includes a social feed where users can share payment activities and engage with friends.

Venmo’s core product is its mobile app, facilitating P2P money transfers, bill splitting, and payments for various purposes. The Venmo Card extends the platform’s functionality to offline retail spending. The social feed feature adds a social element to financial transactions. Venmo’s user-friendly interface and social integration contribute to its popularity among users.

Mobile app for P2P money transfers, bill splitting, and payments, Venmo Card for offline retail spending, social feed for transaction sharing and social engagement, user-friendly interface, and social integration, contributing to popularity.

Revenue Streams

Venmo generates revenue primarily through transaction fees. While Venmo transactions between individuals are usually free, the company charges fees for certain types of transactions, such as business transactions (Pay With Venmo) and instant transfers of funds to linked bank accounts. Additionally, the Venmo Card earns revenue through interchange fees charged to merchants when users make purchases using the card.

The main source of revenue for Venmo is transaction fees, primarily applied to business transactions and instant transfers to linked bank accounts. The Venmo Card also contributes to revenue through interchange fees from merchants. While Venmo fosters a user-friendly P2P payment experience, it monetizes certain premium features and merchant transactions.

Revenue from transaction fees (business transactions, instant transfers to linked bank accounts), revenue generated through interchange fees from merchants using the Venmo Card, monetization of premium features and merchant transactions while offering a user-friendly P2P payment experience.

Customer Segments

Venmo serves a broad customer base that includes individuals looking for a convenient way to split bills, share expenses, and transfer money to friends and family. It also attracts businesses and merchants interested in offering Venmo as a payment option to their customers. Venmo’s user base is typically tech-savvy and comfortable with mobile payment apps.

Customer segments for Venmo encompass individuals seeking convenience in P2P money transfers, bill splitting, and shared expenses. Businesses and merchants interested in offering Venmo as a payment option to enhance customer payment choices also form a customer segment. Venmo’s user base typically consists of tech-savvy individuals comfortable with mobile payment apps.

Individuals seeking convenience in P2P money transfers, bill splitting, and shared expenses, businesses and merchants interested in offering Venmo as a payment option, tech-savvy user base comfortable with mobile payment apps.

Distribution Channels

Venmo primarily operates through its mobile app, which is available for download on iOS and Android devices. Users can also access Venmo through a web browser. The platform leverages its mobile app to facilitate P2P money transfers, payment sharing, and other financial transactions.

Distribution channels for Venmo revolve around its mobile app, accessible on iOS and Android devices. Users can also access Venmo through a web browser. The mobile app serves as the primary platform for P2P money transfers, bill splitting, payment sharing, and various financial transactions. Venmo prioritizes mobile accessibility to enhance user convenience.

Mobile app available on iOS and Android devices, web browser access, primary platform for P2P money transfers, bill splitting, payment sharing, and financial transactions, emphasis on mobile accessibility for user convenience.

Key Partnerships

Venmo collaborates with various partners to expand its reach and functionality. These partnerships may include financial institutions for linking bank accounts, businesses and merchants for payment acceptance, and integration with e-commerce platforms. Venmo also partners with charities and nonprofits to facilitate charitable donations through the platform. Additionally, the platform integrates with social media apps to enable users to share their payment activities.

Collaborations with financial institutions enable the linking of bank accounts. Partnerships with businesses and merchants expand payment acceptance options. Integration with e-commerce platforms enhances user convenience for online purchases. Charitable partnerships facilitate donations through Venmo. Integration with social media apps allows users to share payment activities, enhancing social engagement. Venmo’s partnerships contribute to its ecosystem’s growth and user experience.

Collaborations with financial institutions for bank account linking, partnerships with businesses and merchants for payment acceptance, integration with e-commerce platforms for online purchases, charitable partnerships for donations, integration with social media apps for payment activity sharing, ecosystem growth and enhanced user experience through partnerships.

Key Resources

Venmo’s key resources include its mobile app and technology infrastructure, a network of linked bank accounts, partnerships with businesses and merchants, user data and transaction history, a secure payment platform, and a user-friendly interface. These resources collectively enable Venmo to provide a convenient and secure P2P payment experience.

Key resources for Venmo encompass its mobile app and technology infrastructure, a network of linked bank accounts, partnerships with businesses and merchants for payment acceptance, user data and transaction history, a secure payment platform, and a user-friendly interface. These resources empower Venmo to offer a convenient and secure P2P payment experience to its users.

Mobile app and technology infrastructure, network of linked bank accounts, partnerships with businesses and merchants for payment acceptance, user data and transaction history, secure payment platform, user-friendly interface, resources for providing a convenient and secure P2P payment experience.

Cost Structure

Venmo incurs costs related to transaction processing, including payment processing fees and fraud prevention measures. Additional expenses include marketing and advertising campaigns to acquire and retain users, customer support and service operations, regulatory compliance efforts, employee salaries and benefits, and technology infrastructure maintenance. Costs can fluctuate based on user acquisition and expansion strategies.

Costs associated with Venmo’s operations include transaction processing expenses, such as payment processing fees and investments in fraud prevention measures. Other costs encompass marketing and advertising initiatives for user acquisition and retention, customer support and service operations, regulatory compliance efforts, employee compensation, and maintenance of technology infrastructure. The scale of user acquisition and expansion efforts can influence operational costs. Venmo manages its costs while pursuing user growth and engagement.

Costs related to transaction processing (payment processing fees, fraud prevention measures), marketing and advertising campaigns for user acquisition and retention, customer support and service operations, regulatory compliance efforts, employee salaries and benefits, technology infrastructure maintenance, cost management in alignment with user growth and engagement strategies.

Competitive Advantage

Venmo’s competitive advantage lies in its user-friendly mobile app and social integration, which make P2P payments and financial transactions convenient and engaging. Its widespread adoption among tech-savvy individuals and its partnership network with businesses and charities contribute to its popularity. Venmo’s ability to facilitate payment sharing and social engagement sets it apart in the P2P payment space.

Venmo’s competitive advantage is built on its user-friendly mobile app and social integration, enhancing the convenience and engagement of P2P payments and financial transactions. Its broad adoption among tech-savvy users and partnerships with businesses and charities bolster its popularity. The platform’s unique feature of payment sharing and social engagement differentiates it in the P2P payment market.

User-friendly mobile app and social integration for convenient and engaging P2P payments and financial transactions, widespread adoption among tech-savvy users, partnerships with businesses and charities, popularity boost, unique payment sharing and social engagement features distinguishing it in the P2P payment market.

Ownership and Acquisitions:

PayPal owns Venmo . Indeed, since 2002, PayPal has acquired several brands.

PayPal is the owner of Venmo, a popular peer-to-peer payment service.

In 2013, PayPal acquired Braintree, a payment processing company, and indirectly acquired Venmo as part of the deal.

Braintree had previously acquired Venmo in 2012 for $26.2 million.

PayPal’s Family of Brands:

Since its founding in 2002, PayPal has acquired several brands in the payment industry.

In 2013, after acquiring Braintree, PayPal’s portfolio included various payment solutions and brands.

Venmo became part of the PayPal family of brands, along with Braintree, Xoom, and iZettle products.

PayPal’s Strategy:

PayPal’s acquisitions, including Venmo and Braintree, have allowed it to expand its offerings and strengthen its presence in the digital payment space.

With Venmo as part of its portfolio, PayPal has been able to tap into the peer-to-peer payment market and attract a younger, tech-savvy user base.

Key Takeaways:

PayPal owns Venmo, a popular peer-to-peer payment service.

Venmo became part of the PayPal family of brands after PayPal acquired Braintree, which had previously acquired Venmo.

The acquisition of Venmo has helped PayPal expand its payment solutions and attract a broader range of

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.PayPal makes money primarily by processing customer transactions on the Payments Platform and from other value-added services. Thus, the revenue streams are divided into transaction revenues based on the volume of activity or total payments volume—and value-added services, such as interest and fees earned on loans and interest receivable. In 2022, PayPal generated over $27.5 billion in revenues and over $2.4 billion in net profits. eBay’s core business is a platform business model that makes money from transaction fees through its marketplaces. In short, eBay primarily makes money by charging fees on successfully closed transactions. For instance, in 2021, on an $87 billion worth of gross merchandise value sold on eBay, the company generated $9.77 billion in transaction revenues at an 11.19% take rate (fee).

OpenAI is an artificial intelligence research laboratory that transitioned into a for-profit organization in 2019, which comprised an entity called OpenAI LP and the non-profit parent foundation OpenAI. The lab, which was founded in 2015 by Elon Musk, Sam Altman, and various others, has a core focus on the development of friendly AI that benefits society as a whole. Yet now has primarily evolved as a capped-for-profit entity with an exclusive commercial license to Microsoft.

Its co-founders primarily own Airbnb: Brian Chesky, with 76,407,686 Class B shares, which gives him 29.1% of ownership; Nathan Blecharczyk, with 232,306 Class A and 64,646,713 Class B, which give him 25.3%; and Joe Gebbia, which has 5,113,865 Class A and 58,023,452 Class B, which give him 22.9% ownership.

Google is primarily owned by its founders, Larry Page and Sergey Brin, who have more than 51% voting power. Other individual shareholders comprise John Doerr (1.5%), a venture capitalist and early investor in Google, and CEO, Sundar Pichai. Former Google CEO Eric Schmidt has 4.2% voting power. The most prominent institutional shareholders are mutual funds BlackRock and The Vanguard Group, with 2.7% and 3.1%, respectively.

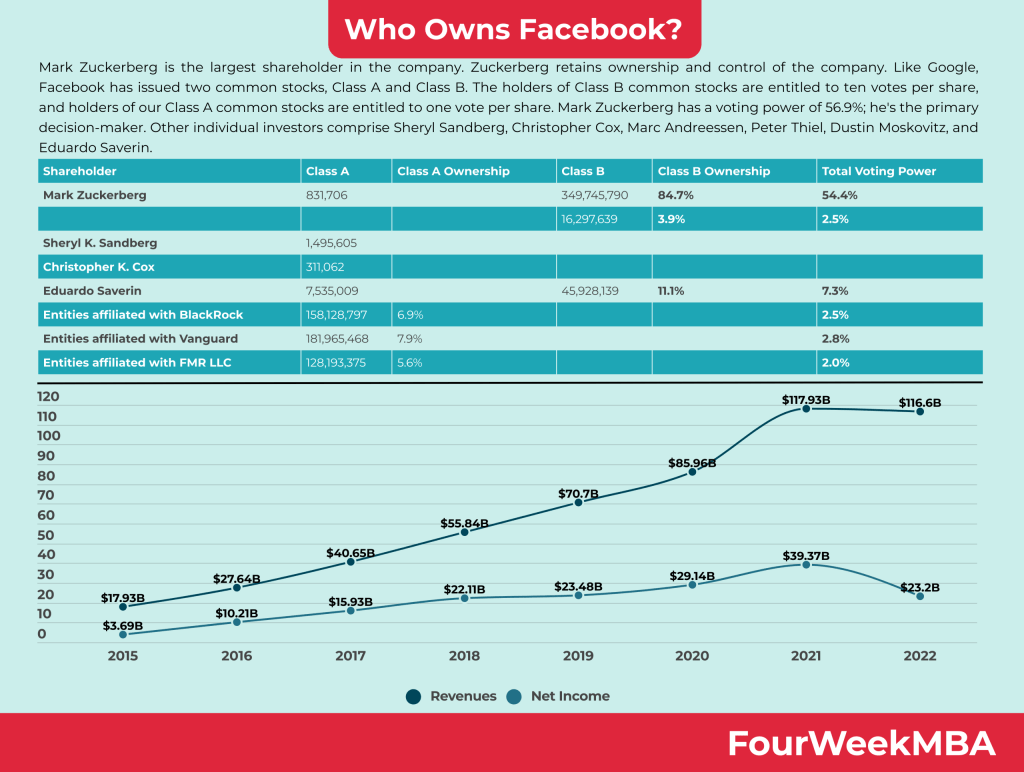

Mark Zuckerberg is the largest shareholder in the company. Zuckerberg retains ownership and control of the company. Like Google, Facebook has issued two common stocks, Class A and Class B. The holders of Class B common stocks are entitled to ten votes per share, and holders of our Class A common stocks are entitled to one vote per share. Mark Zuckerberg has a voting power of 56.9%; he’s the primary decision-maker. Other individual investors comprise Sheryl Sandberg, Christopher Cox, Marc Andreessen, Peter Thiel, Dustin Moskovitz, and Eduardo Saverin.

As of 2023, major Apple shareholders comprised Warren Buffet’s Berkshire Hathaway with 5.73% of the company’s stock (valued at over $130 billion). Followed by other individual shareholders like Tim Cook, CEO of Apple, with about 3.3 million shares, Artur Levinson, chairman of Apple, with over 4.5 million shares, and others.

With 64,588,418 shares, Jeff Bezos is the major individual investor. Owning 12.7% of the company. Other top individual investors comprise Amazon’s CEO Andy Jessy, with 94,729 shares. Top institutional investors include mutual funds like The Vanguard Group (6.6% ownership) and BlackRock (5.7% ownership).

Major shareholders comprise co-founder Bill Gates, who stepped down from the company’s board in 2020, which is why these shares are no longer publicly reported. In 2019, Gates still owned a stake of 103 million stocks, which accounted for 1.34% of the company’s ownership (worth over $23 billion in January 2023). Other individual shareholders comprise Satya Nadella, the company’s CEO, Brad Smith (former president), Jean-Philippe Courtois (EVP), and Amy Hood (former CFO).

By 2022, most of Tesla’s shares are still owned by Elon Musk, among the company’s co-founders and the CEO. Elon Musk is the top individual investor, with a 23.5% stake in the company, equivalent to over 244 million shares. Musk is followed by Lawrence Ellison (founder of Oracle), with a 1.5% company stake. Ellison also sits on Tesla’s board. And Antonio Gracias, among the company’s first investors, has over 1.6 million shares. Other institutional investors and mutual funds like The Vanguard Group (6%), Blackrock (5.1%), and Capital Ventures International also have a good chunk of the company’s stocks.

PayPal was first founded in 1998; it was called Confinity (among its founders was Peter Thiel); later, it merged with X.com, its major competitor, founded by Elon Musk (which would become known for other companies like Tesla and SpaceX). From this merger, PayPal was born. In 2002, PayPal was bought by eBay for $1.5 billion. eBay spun off PayPal in 2015, which would be listed as an independent entity. Today PayPal owns brands like Braintree, Venmo, Xoom, and iZettle.

Netflix’s largest individual shareholder is Reed Hastings, co-founder, and former CEO of the company, now Chairperson of Netflix, with a 1.7% stake, valued at over $2.4 billion in February 2023. Other significant individual shareholders comprise Jay C. Hoag, the company’s directors since 1999, and Ted Sarandos, former chief content officer and now Chief Executive Officer of Netflix. Major institutional shareholders comprise The Vanguard Group (7.55% ownership), BlackRock (6.58% ownership), and Capital Research Global Investments (5.84% ownership).

TikTok is owned by ByteDance, a Chinese internet technology company owning several content platforms worldwide (Douyin, Toutiao, Xigua Video, Helo, Lark, Babe). Bytedance passed the $300 billion private market valuation by 2022, making around $58 billion in revenue in 2022, over $4 billion from TikTok.

Acquired by Google, in 2006, for $1.65 billion, YouTube is now worth many times over. In 2022, YouTube generated over $29 billion in revenue from advertising alone. YouTube is part of Google (now named Alphabet), and as such, it is owned by main Google’s Alphabet shareholders and is one of the fastest-growing segments for the company.

As of April 25th, 2022, Elon Musk tried to take over Twitter. Musk tried to purchase the company at $54.20 per share, or about $44 billion. The deal finally closed by October 27th, 2022, and Elon Musk became the largest shareholder.

The multi-billion music streaming company Spotify is primarily owned by its founders, Daniel Ek and Martin Lorentzon. As of 2023, Daniel Ek has 16.5% ownership of ordinary shares and 31.7% of the voting power. Martin Lorentzon has 10.9% of ordinary shares and 42.6% of the voting power. Another key shareholder is Baillie Gifford & Co, a Scottish-based money management firm, followed by Morgan Stanley, T. Rowe Price, and Tencent.

The top individual shareholder of NVIDIA is Jen-Hsun Huang, founder, and CEO of the company, with 87,521,722 shares giving him 3.50% ownership. Followed by Mark A. Stevens, venture capitalist and a partner at S-Cubed Capital, who was part of the NVIDIA board in 2008 and previously served as a director from 1993 to 2006, with 6,258,803 shares. Institutional investors comprise The Vanguard Group, Inc, with 196,015,550, owning 7.83%. BlackRock, Inc., with 177,858,484, owns 7.10%. And FMR LLC (Fidelity Institutional Asset Management) with 158,039,922, owning 6.31%.

Evan Spiegel and Robert Cornelius Murphy are the co-founders and, respectively, CEO and CTO of Snapchat. Evan Spiegel owns 3% of Class A stocks, 25.7% of Class B stocks, and 53.4% of Class C stocks for a 53.2% voting power, whereas Robert Murphy owns 6% of Class A stocks, 25.7% of Class B stocks, and 46.6% of Class C stocks for a 46.6% voting power. Snapchat runs an advertising-based businessmodel.

Uber’s principal individual shareholders comprise Yasir Al-Rumayyan (3.73%), the Governor of the Public Investment Fund, the sovereign wealth fund of the Kingdom of Saudi Arabia, and Dara Khosrowshahi, the founder and CEO of Uber. There is Morgan Stanley, with 5.12% ownership among the top institutional investors.

The founder and CEO of Shopify, Tobias Lütke, owned or controlled 7,891,852 Class B multiple voting shares and 5,250 Class A subordinate voting shares, representing approximately 33.8% of the aggregate voting power attached to all of the Company’s outstanding voting shares. Another key stakeholder is John H. Phillips, an angel investor who placed an early bet on Shopify.

Roblox is owned by David Baszucki and Gregory Baszucki, with a 2.3% and 2.6% stake, respectively. Anthony lee, managing partner at Altos Ventures, with a 15.3% stake.

In 2014, Twitch was bought by Amazon for $970 million. Therefore Twitch is part of Amazon, comprising other subsidiaries bought over the years, like Audible, Whole Foods, and Zappos (in total, Amazon has 12 subsidiaries). Therefore, as of 2020, Twitch is a multi-billion dollar company, making money primarily via advertising through its video streaming platform (creators use Twitch today across many other verticals).

Zoom’s main private shareholders comprise Eric S. Yuan, a Chinese-American billionaire businessman that founded Zoom. Dan Scheinman, board member and angel investor in Zoom since the start, and Santiago Subotovsky, also an early investor in Zoom. Zoom follows a freeterprise business model where free accounts are channeled into enterprise customers.

PayPal owns Venmo . Indeed, since 2002, PayPal has acquired several brands. In 2013, as PayPal indirectly bought Braintree, it also bought Venmo. Braintree acquired Venmo in 2012 for $26.2 million. Therefore, by 2013, Venmo entered the PayPal family of brands comprising payment solutions like Braintree, Venmo , Xoom, and iZettle products . PayPal owns Venmo .

What are the ownership and acquisitions?

PayPal is the owner of Venmo, a popular peer-to-peer payment service.. In 2013, PayPal acquired Braintree, a payment processing company, and indirectly acquired Venmo as part of the deal.. Braintree had previously acquired Venmo in 2012 for $26.2 million.

What are the paypal's family of brands?

Since its founding in 2002, PayPal has acquired several brands in the payment industry.. In 2013, after acquiring Braintree, PayPal's portfolio included various payment solutions and brands.. Venmo became part of the PayPal family of brands, along with Braintree, Xoom, and iZettle products.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.

")

")