Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

How Coinbase evolved over the years in terms of products and services offered (Image Source: Coinbase S-1).

In 2012, as a simple crypto exchange platform, Coinbase evolved over the years as a trading platform.

And it is completing its evolution in the coming decade as a “digital bank” where crypto-assets can be deposited to earn interest, exchanged, or perhaps lent and borrowed.

Coinbase’s primary value model moves along the digitalization of the financial system.

The web’s first waves had brought leaps of digitalization in many fields; the financial system wasn’t much affected.

While new companies like PayPal tried to create a sort of digital currency.

The system never changed toward the decentralization of money, where banks could be disintermediated.

Coinbase and the whole Blockchain industry found its most compelling potential application, decentralizing money.

For that sake, Coinbase has become one of the most known brands that enable a broad base of retail users to exchange, transact and earn in crypto assets.

Vision

As Coinbase’s founder, Brian Armstrong, highlighted in the first shareholder letter “Coinbase is a company with an ambitious vision: to create more economic freedom for every person and business.”

As he further highlighted, “Everyone deserves access to financial services that can help empower them to create a better life for themselves and their families.”

Therefore, Coinbase claims to be “building the cryptoeconomy – a more fair, accessible, efficient, and transparent financial system for the internet age that leverages crypto assets: digital assets built using blockchain technology.“

The company started in 2012 after Coinbase’s co-founders had read the Bitcoin White Paper from Satoshi Nakamoto.

From there, the idea of enabling wider adoption of cryptocurrencies (headed by Bitcoin) has become the main driver for Coinbase’s growth. Indeed, Coinbase’s revenues are also tied to the price/adoption of cryptocurrencies. Therefore, its long-term success does depend on that.

Mission

Coinbase’s mission is “to create an open financial system for the world.”

As the company further highlighted in its financial prospectus, “the way that we invest, spend, save, and generally manage our money remains cumbersome, inaccessible, expensive, and regionally isolated. In contrast, the internet has transformed our society by connecting the world and enabling the seamless exchange of information. The legacy financial system is struggling to keep pace with the speed of technological advancements in a global and digitally interconnected society, resulting in the need for a new, natively digital financial system.”

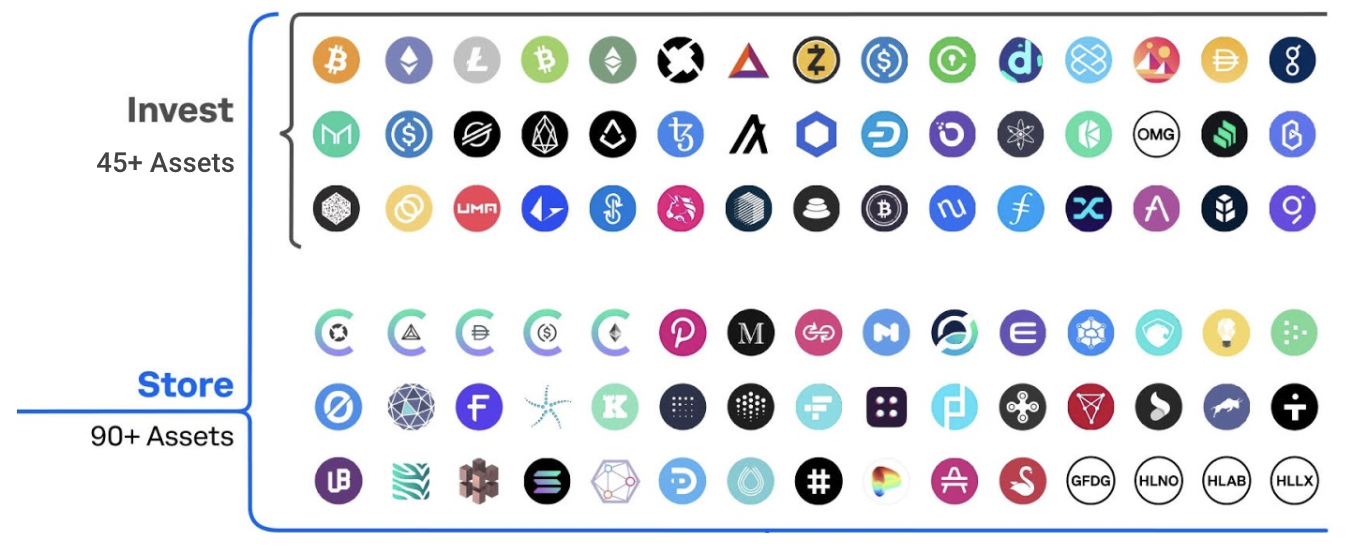

Coinbase enables anyone to transact cryptocurrencies. The trading/investing platform has been integrating the most popular Blockchain protocols and dozens of crypto assets over time, either for trading or custody. Therefore, Coinbase’s value proposition moves along two main services: investing (the ability to purchase dozens of crypto assets) and depositing (the ability to store over ninety crypto assets by the time of Coinbase’s IPO).

Problem:

Coinbase tapped into the financial system’s decentralization, which was the primary pay-off/use case that Bitcoin leveraged. From there, exchange platforms like Coinbase were instrumentals to the initial success of Bitcoin.

Indeed, while initially mining Bitcoin could be done by anyone, once more people joined the network unless you had a mining facility*. Therefore, exchange platforms became fundamental to the success of Bitcoin. And legendary platforms like Mt. Gox (the first exchange platform that went bankrupt in 2014) became instrumental to Bitcoin‘s major success.

*Quick note: the mining process is the process of generating more Bitcoins. However, when Satoshi Nakamoto designed the Blockchain protocol for Bitcoin, it placed some limitations to the number of Bitcoin that could circulate in the long-run (once it reached 21 million Bitcoin in circulation, no more could be mined). At the same time, the more Bitcoin circulated, the more mining them became difficult. Indeed, miners needed more computing power to solve the complex mathematical problems required to be rewarded new Bitcoins (this is known as proof of work, and it is the mechanism at the basis of Bitcoin‘s Blockchain). Therefore, while in the early

A Proof of Stake (PoS) is a form of consensus algorithm used to achieve agreement across a distributed network. As such it is, together with Proof of Work, among the key consensus algorithms for Blockchain protocols (like the Ethereum’s Casper protocol). Proof of Stake has the advantage of the security, reduced risk of centralization, and energy efficiency.

Mt. Gox Failure, Coinbase’s Success

It is worth exploring, in a nutshell, the story of Mt. Gox.

When Jed McCaleb, back in 2010, had read about Bitcoin on a PR release over Slashdot, he was convinced that an exchange would have helped Bitcoin grow, so he set it up on a website he had bought years before for an online magic game called “Magic: The Gathering Online” which would be reused as the domain for Mt. Gox.

Once set up, the exchange quickly picked up, and it became in a short time frame the most successful Bitcoin exchange platform.

However, it has shown since the beginning one of the major drawbacks of exchange platforms: security. Where the Blockchain protocol had been designed for security and privacy.

Once people started to exchange Bitcoins via Mt. Gox, two issues came up quickly: one, the identity of Bitcoin holders that through the Blockchain was kept private, would be easily revealed via Mt. Gox.

Second, as more people referred to Mt. Gox to store their Bitcoins security problems became a major issue. Indeed, by 2014 Mt. Gox had to file for bankruptcy as a massive number of Bitcoin had been stolen by hackers, thus exposing Mt. Gox to a huge financial liability.

That lesson, extremely expensive for Mt. Gox would become a valuable lesson for all the other crypto platforms that survived.

Solution

Coinbase’s services have been modeled around the main customers. Perhaps, retail users can trade multiple crypto assets.

While institutional clients have access to an advanced platform for both trading and securing crypto assets.

Image Source: Coinbase S-1

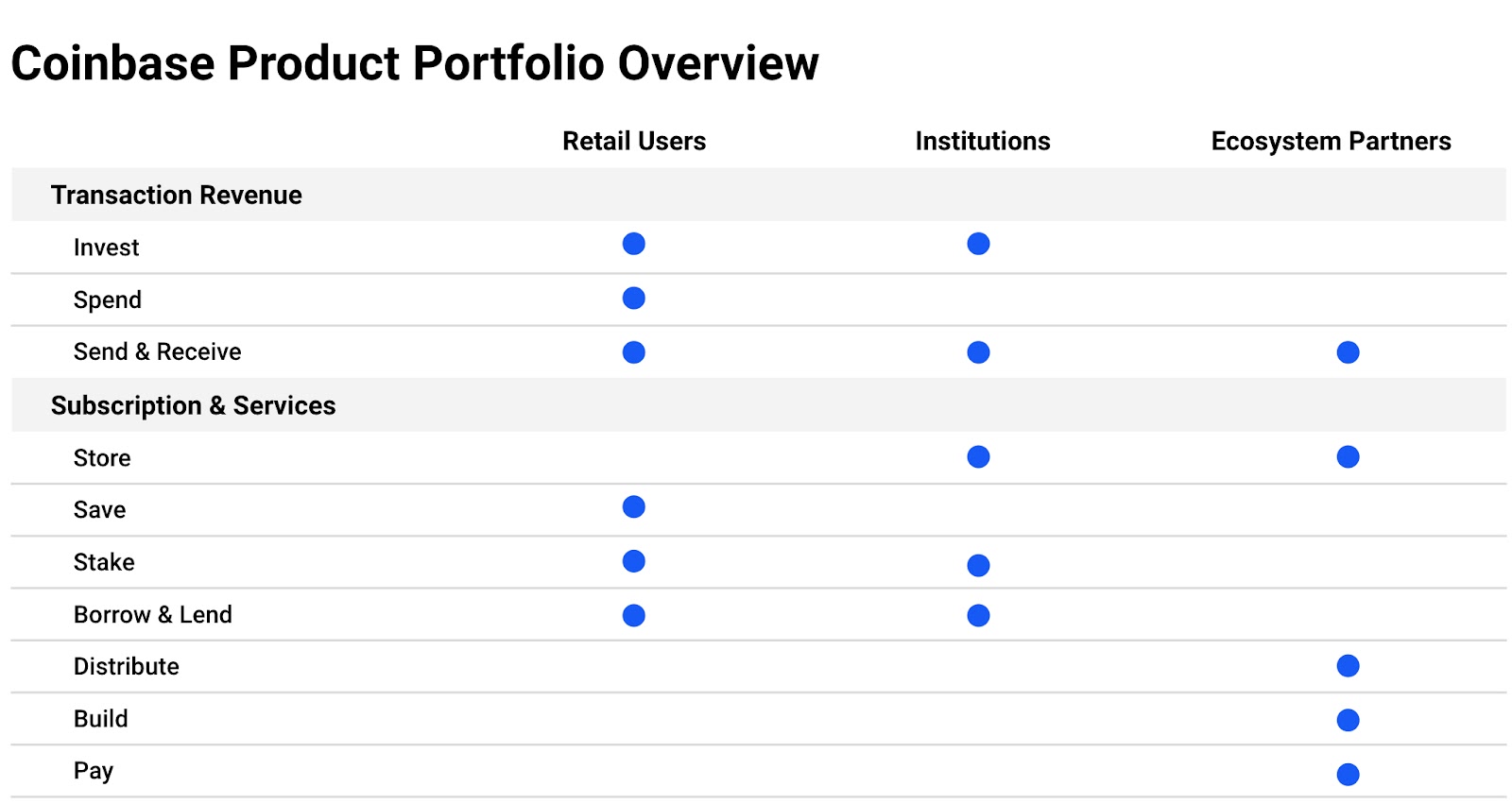

Customer Composition

Retail users: Coinbase offers a “safe, trusted, and easy-to-use platform to invest, store, spend, earn, and use crypto assets.”

Institutions: Coinbase offers a “one-stop shop for accessing crypto markets through advanced trading and custody technology, built on top of a robust security infrastructure.”

Ecosystem partners: developers, and merchants can build applications on top of the platform, and participate actively in the protocols part of the Coinbase offering.

Technological Model: Core Technology and R&D Management

Coinbase’s technological model is based on its end-to-end financial infrastructure — as explored in the economics of AI compute infrastructure — , where customers can buy dozens of crypto assets, secure them and find various options to store these assets.

Coinbase ecosystem combines retail customers, institutions, and other partners (like merchants and developers). The tech platform focuses on cybersecurity, compliance, and expansion of Blockchain protocols over time.

To understand how the Coinbase value proposition is enhanced by its platform, you need to understand the nature of the Crypto asset markets, which (as Coinbase emphasizes) “natively digital, real-time, and operate globally on a 24/7/365 basis.”

Coinbase stresses out that the “always-on” nature of the crypto economy (crypto assets are traded 24/7) requires a technical infrastructure able to support this ongoing demand for crypto assets. Thus, Coinbase focused its efforts over the years in making this platform as stable and safe as possible, which drives a tremendous amount of direct traffic (people accessing it directly via its web apps or mobile apps).

Indeed, let’s remember that one of the critical issues that former crypto exchange platforms had encountered were all related to security, scalability, and regulatory compliance, all things that Coinbase has been able to successfully address so far.

The major, continuous investment for Coinbase will be to keep improving its security, discoverability, and the crypto assets available on the platform to become the “one-stop” crypto shop for retail investors.

Retail Platform

One key challenge/element/value of the retail platform is to enable users to potentially trade a wide number of crypto assets. Therefore, security coupled with scalability (and compliance) is key element for the retail platform’s success (Image Source: Coinbase S-1).

The main features that make Coinbase’s platform successful (so far) are:

Invest.

Spend.

Send & Receive.

Save.

Stake.

Over time, becoming the “one-stop-shop” for crypto assets becomes critical.

Institutional Platform

One key challenge/element/value of the institutional platform is to provide a solid infrastructure for large transactions and storing to execute complex trades (Image Source: Coinbase S-1).

The main components of the institutional platform comprise:

Investing, which enables institutional investors to perform complex trades, as institutional customers can use over-the-counter, or OTC, trading desks, with a volume-based pricing.

Send & Receive Store, to provide a “highly secure cold storage solution.” Indeed, one of the key issues of transactions outside the Blockchain is that if hacked and the private keys stolen there is no way to trace them back. Thus, this service addresses one of the key weaknesses that trading crypto assets present.

Staking (a specific form of validation for some blockchain protocols).

Borrow & Lend.

Partners’ Platform

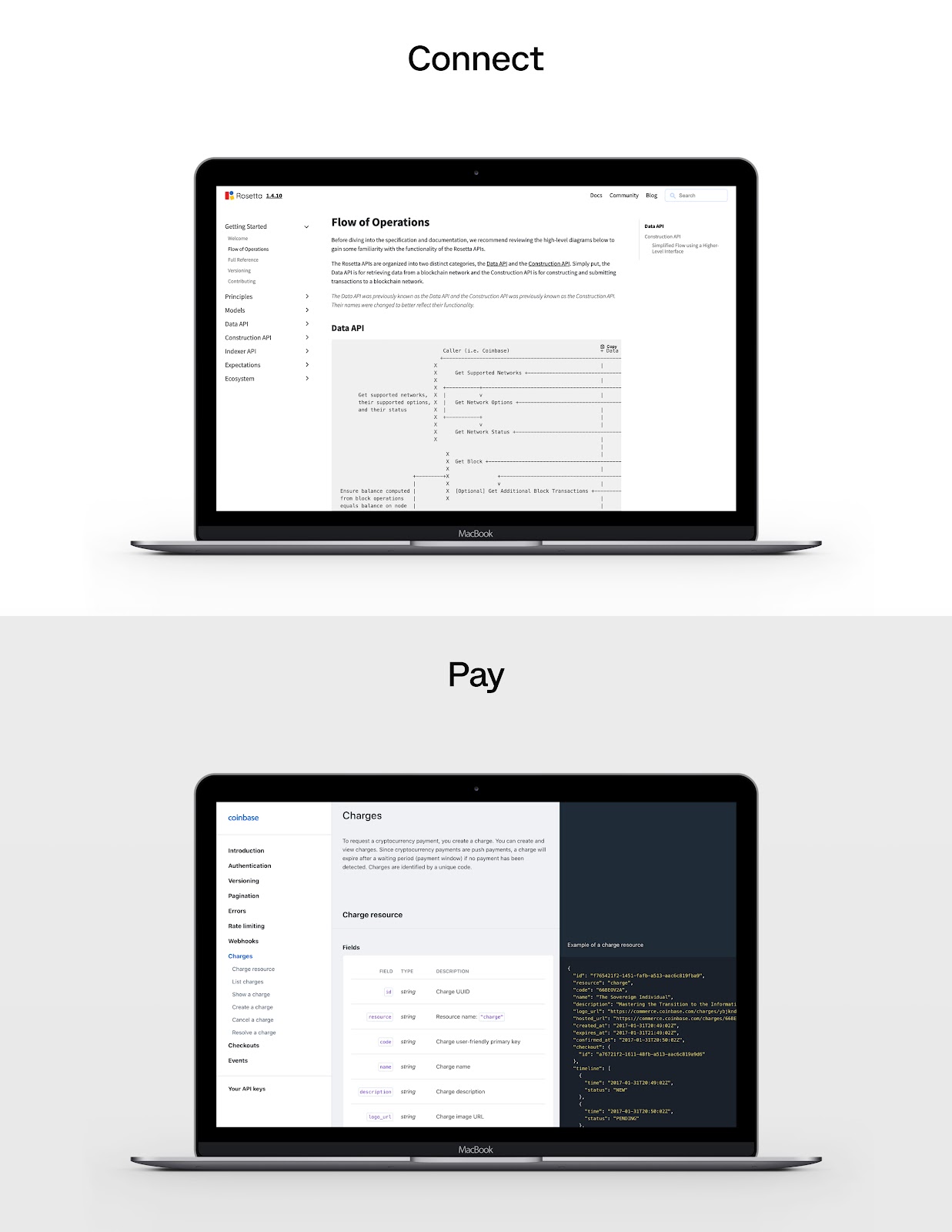

One key challenge/element/value of the partners’ platform is to provide tools that can be used to leverage the crypto-economy. Some key issues that developers in the crypto economy encounter comprise “lack distribution, trust, and usability, and the availability of easy-to-use and scalable infrastructure.” (Image Source: Coinbase S-1).

Some key elements of the partners’ platform comprise:

Distribution: Coinbase has a platform with over forty million verified users (as of March 2021). These can be leveraged to sponsor new crypto projects. For instance, Coinbase has been implementing a system of e-learning and gamification, to reward users of crypto assets if completing certain actions (like following short lectures or downloading the app).

Build. Coinbase also offers the infrastructure for developers to build tools like, Coinbase Analytics (analytical tool licensed to law enforcement and financial institutions to monitor blockchain transactions – customer personal data is kept private); Rosetta which enables developers to build applications for different blockchains by using a single standard; USDC: a crypto asset backed 1:1 by a U.S. dollar.

Pay enabling merchants to accept cryptocurrency payments in a fully decentralized way.

Leapfrog Innovation

Coinbase has been capable of building a solid platform in the first wave of the crypto economy. In the future, new protocols and crypto assets might become key players in the industry. Being able to anticipate or at least quickly adopt these crypto assets will be a key ingredient for the future success of Coinbase. As part of the platform’s success is given by the fact it trades the successful assets from the crypto-economy.

Distribution Model and Go-to-market strategy

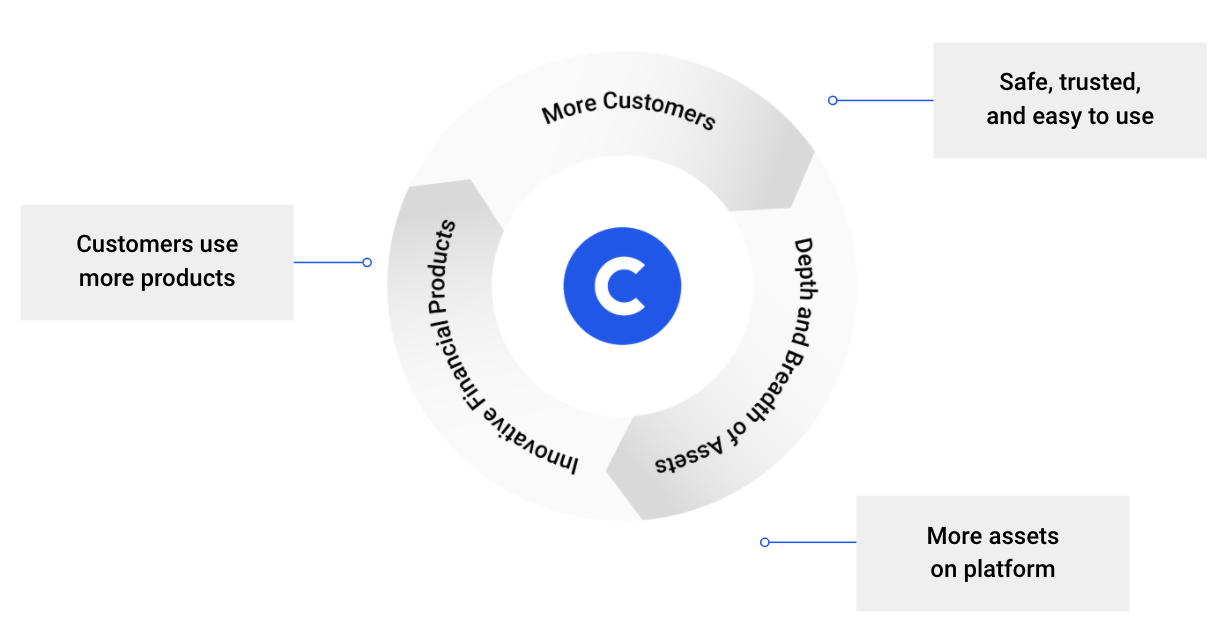

Coinbase follows the flywheel pattern as a platform business model where its customer base (made of retail users, institutions, and partners) improves the platform and amplifies it. In fact, as retail users go to Coinbase to discover the prices of crypto assets (Coinbase has built a solid and user-friendly discovery and search engine for crypto assets), they might also prefer it as the go-to platform for transactions. From there, institutions and partners attracted by a large number of retail customers join in.

The Coinbase flywheel in action: where more retail users get to the platform given its known brand and organic traffic (driven by its user-friendly search/discovery engine for crypto assets), the more those same users might transact on the platform. Thus, driving more partners to develop apps on top of Coinbase, while at the same time offering new products and protocols, therefore, further attracting retail users.

Adding more customers by increasing adoption of products/crypto-assets for its key customers, by leveraging growthmarketing, product development, and all the other key digital channels for continuous growth.

Expanding the available assets on the platform, thus making it more valuable for all customers and partners.

Launching new products.

Financial Model

Coinbase’s main metrics or KPIs are measured based on the number of verified users on the platforms, the monthly transaction each user is performing through the platform. The assets which are stored and traded on the platform, together with the trading volume. Based on these transactions, Coinbase will earn its income, thus generating more or less income. That is why Coinbase’s success is also tied to the public’s continuous interest in the crypto-economy (Data source: Coinbase S-1).

Revenue Model

Coinbase’s revenue model primarily moves around three main streams: transaction revenues, which by far represent the largest income source, subscription, and services revenue, and other revenues (Crypto asset sales revenue and Corporate interest income) – data source: Coinbase S-1.

Coinbase generated $1.52B in transaction revenue, $1.4B in subscriptions and services, and $182 million in other revenue for 2023.

In 2023, transaction revenue represented 49% of Coinbase’s total revenue, while subscriptions and services represented 45%.

Coinbase Revenue model moves around a few key streams:

Transaction revenues: made when each transaction is processed through the platform. Most of them come from retail investors.

Subscription and services revenues: comprising a set of subscription services offered on the platform and custodial fees. In addition to earning campaign revenues and interest income.

And other revenues comprising crypto-asset sales revenues and corporate interest income.

Transaction revenues

The major driver of revenues for Coinbase was in 2023.

Each time a transaction is processed via Coinbase the platform will earn revenue as a fee from the transaction. Coinbase applies a volume-based pricing approach where transaction fees will vary based on the trading volume. In general, the transaction fee is collected from the customer at the time the transaction is executed.

Retail transaction revenues

In 2020, the transaction fees from retail investors represented the majority of the fees generated by Coinbase.

Things changed by 2022 when institutional investors played a key role again.

Coinbase reported a trading volume of $468 billion in 2023. Of which $75 billion came from consumers vs. $393 billion from institutional clients.

While the main assets traded on the platform remained, the two major crypto assets were Bitcoin and Ethereum.

In 2023, of the $468 total trading volume on Coinbase, 34% came from Bitcoin; 20% from Ethereum, 35% from other coins, and 11% from USDT.

Retail transaction revenues

In 2020, the transaction fees from institutional investors represented a minority of the fees generated by Coinbase.

Yet, by 2022, institutional investors represented a good chunk of the company’s transaction revenues.

Subscriptions and services

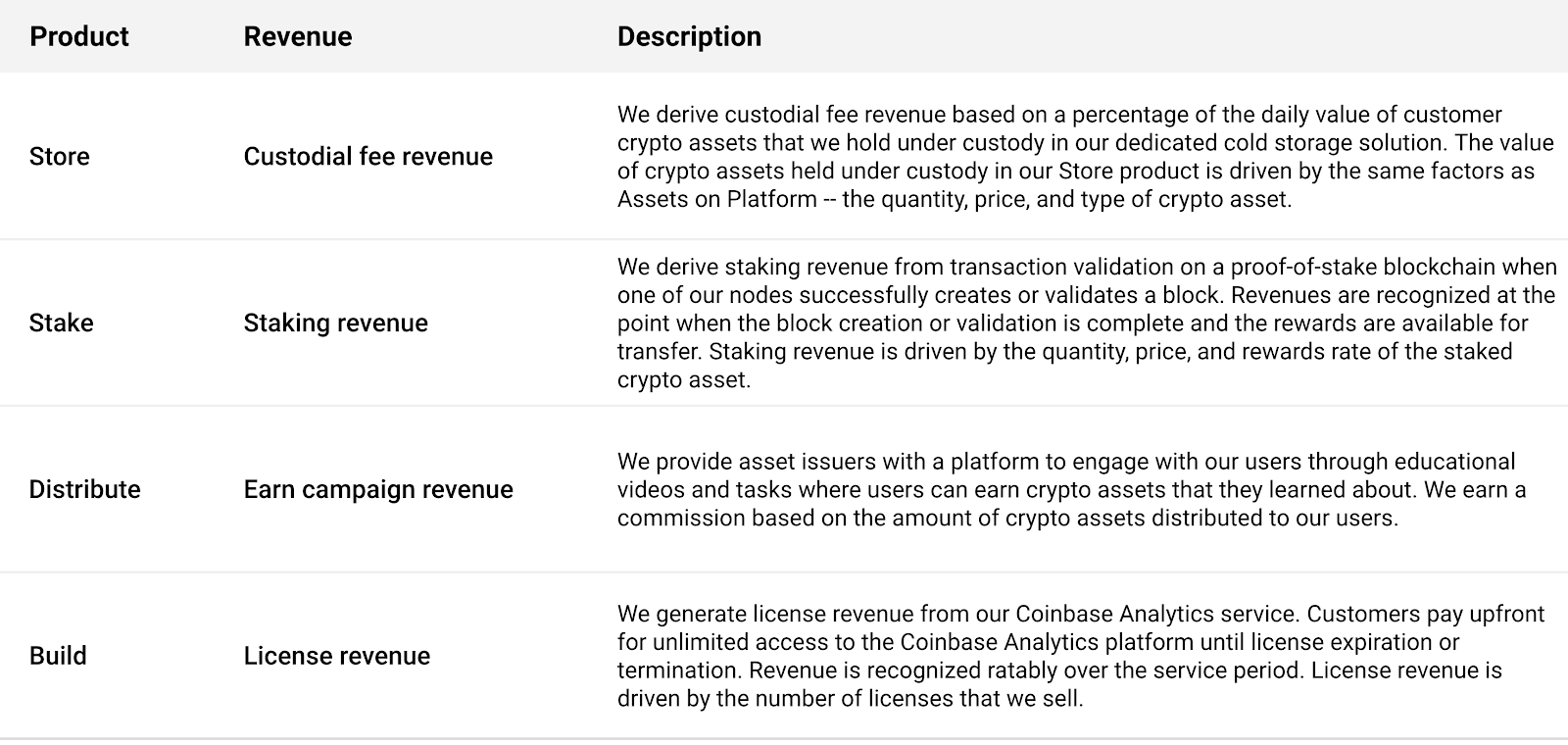

The other source of revenues is subscription and services comprising Store, Stake, and Borrow & Lend, especially to reduce dependence on transaction revenues (highly dependent on short-term trading volume).

Other custodial fee revenue (given the increase in the number of customers and the value of crypto assets held under custody within the Coinbase Store product).

Custodial fee revenue

Coming from a dedicated secure cold storage solution to customers, which generates fees for Coinbase, based on the value of the crypto assets held in the storage solution. The fee is collected on a monthly basis.

Staking revenue

For blockchain-based on proof-of-stake, Coinbase gets the reward by creating or validating blocks on the network. Thus, these get validated, thus making Coinbase earn a reward (paid in the crypto asset validated via the platform).

A Proof of Stake (PoS) is a form of consensus algorithm used to achieve agreement across a distributed network. As such it is, together with Proof of Work, among the key consensus algorithms for Blockchain protocols (like Ethereum’s Casper protocol). Proof of Stake has the advantage of the security, reduced risk of centralization, and energy efficiency.

Earn campaign revenue

This part of the platform offers crypto asset issuers the chance to amplify and market their products via Coinbase. Through specific actions (like completions of video tutorials, quizzes, and more) crypto-asset issuers can get their product known, while the users will receive in exchange the crypto asset for free, and Coinbase gets fees as a result of the transactions on the platform (the crypto assets distributed to users).

Interest income and corporate interest income

This is the interest earned on customers’ custodial funds, that the company keeps together with cash and cash equivalents.

Other subscription and services revenues

Primarily including revenue from early-stage services.

Other revenues

In some cases, Coinbase might fulfill customer transactions using its own crypto assets. This happens when the transaction volume might spike. In that case, Coinbase records the full transaction as revenues, and the transaction value not related to fees as an operating expense. Others also increased substantially driven by the sales of Coinbase crypto assets.

Cost Structure

Coinbase’s cost structure is primarily divided into transaction expenses, technology & platform development, and sales & marketing activities.

Transaction expense

These comprise all the costs to run the platform, such as the costs associated with the processing of trades and wallet services. All the costs incurred for account verifications fees, fees to process transactions on blockchain networks, and fees paid to other payment processors are part of the transaction expenses.

Technology and development

These comprise all the costs related to maintaining and developing the platform, including website hosting and other infrastructure costs, together with costs to develop new products and services.

Sales and marketing

These primarily consist of costs to acquire customers, advertise the platform and other marketing programs, together with the personal costs.

General and administrative

These include all the costs related to legal, finance, compliance, human resources, customer experience, and support operations, executive management, and other administrative services.

Profitability

The company’s profitability highly depends on keeping a high trading volume, in part driven by the interest in crypto assets. Part of this profitability has been smoothing (since 2018) by subscription services. Simultaneously, massive investments toward the platform and the high general and administrative costs drive profitability down.

Cash Generation

In 2020, most of the cash was provided by the custodial funds kept by Coinbase. In short, these are funds held for customers. Indeed, by December 2020, of the over three billion in cash from operating activities, $2.7 billion was related to custodial funds.

These funds are kept on dedicated accounts and are restricted for use.

Putting it all together

Coinbase is a digital platform for trading and storing cryptocurrencies. It makes money via transaction fees, subscriptions, commissions earned on custodial funds, and interests earned on these.

Coinbase tech platform is both a search and discovery engine for crypto assets. Its underlying platform also offers tools for developers, merchants, or other institutional partners.

The platform’s flywheel is developed around its variety in crypto assets, attracting retail users attracted by a known brand, safe and secure for trading.

Key Highlights

Mission and Vision: Coinbase’s mission is “to create an open financial system for the world,” empowering individuals and businesses with economic freedom. Their vision is to build a more fair, accessible, efficient, and transparent financial system using crypto assets and blockchain technology.

Platform Evolution: Starting as a crypto exchange in 2012, Coinbase has evolved into a comprehensive platform that facilitates trading, storing, spending, and earning in crypto assets. It aims to become a “digital bank” offering diverse financial services centered around cryptocurrencies.

Value Propositions: Coinbase’s value propositions include enabling retail users to invest, store, spend, earn, and use crypto assets. It provides a secure platform for retail customers, institutions, and ecosystem partners to engage with the crypto economy.

Revenue Streams: Coinbase generates revenue through transaction fees, subscription and service fees, custodial fees, staking rewards, and more. Its main income sources come from facilitating transactions and offering value-added services.

Customer Segments: The platform serves retail users, institutional investors, and partners like developers and merchants. It caters to a diverse range of clients interested in trading, storing, and utilizing crypto assets.

Technology and Security: Coinbase focuses on providing a stable and secure platform for trading and storing crypto assets. Its technological infrastructure addresses issues of security, scalability, and regulatory compliance.

Distribution Model: Coinbase’s platform follows a flywheel pattern, where the growing user base of retail customers attracts institutions and partners, creating a self-reinforcing cycle of growth.

Profitability and Cash Generation: Coinbase’s profitability is closely tied to trading volumes and interest in crypto assets. Subscription services and institutional participation help stabilize revenues. Custodial funds and interests contribute to cash generation.

Long-Term Success and Crypto Adoption: Coinbase’s success is linked to the broader adoption of cryptocurrencies and blockchain technology. Its growth and profitability are intertwined with the expansion and interest in the crypto economy.

Mission-Driven Approach: Coinbase’s overarching mission is to promote financial freedom and accessibility. It strives to revolutionize the financial system by leveraging the potential of crypto assets and blockchain technology.

Business Model Element

Analysis

Implications

Examples

Value Proposition

Coinbase’s value proposition centers on providing a secure and user-friendly platform for buying, selling, and managing cryptocurrencies. It offers a wide range of cryptocurrencies, secure storage solutions, and educational resources. Coinbase emphasizes accessibility, reliability, and regulatory compliance, making it a trusted choice for both beginners and experienced crypto users.

Provides a secure and user-friendly platform for cryptocurrency transactions. Offers a diverse selection of cryptocurrencies for trading and investment. Fosters trust through regulatory compliance and security measures. Attracts both beginners and experienced cryptocurrency users. Offers educational resources to enhance users’ understanding of cryptocurrencies. Promotes financial inclusion by simplifying crypto access.

– Users can buy, sell, and store various cryptocurrencies on Coinbase’s platform. – Coinbase offers secure storage solutions, including Coinbase Wallet and Vault, to protect users’ assets. – Emphasis on regulatory compliance and security instills trust in users. – Coinbase’s user-friendly interface makes it accessible to beginners while providing advanced features for experienced traders. – Educational resources like Coinbase Learn educate users about cryptocurrencies and blockchain technology. – Coinbase’s mission to make cryptocurrency accessible aligns with its value proposition of promoting financial inclusion.

Customer Segments

Coinbase serves a broad customer base, including individual investors, cryptocurrency enthusiasts, traders, institutions, and businesses. It caters to both retail and institutional users, offering various services tailored to different needs. Coinbase’s global reach attracts users from around the world seeking cryptocurrency solutions and investment opportunities.

Addresses the needs of individual investors, cryptocurrency enthusiasts, and traders. Attracts institutional investors and businesses seeking crypto services. Offers a global platform connecting users from diverse backgrounds. Provides a range of services, from simple buying and selling to advanced trading and custody solutions. Supports financial institutions through Coinbase Custody.

– Individual investors use Coinbase to buy, hold, and trade cryptocurrencies for investment purposes. – Cryptocurrency enthusiasts and traders leverage Coinbase Pro, a more advanced trading platform. – Businesses may use Coinbase Commerce to accept cryptocurrency payments from customers. – Institutions rely on Coinbase Custody to secure their digital assets. – Coinbase’s global platform serves users from various countries and backgrounds.

Distribution Strategy

Coinbase primarily operates as a digital platform accessible through its website and mobile apps. It offers services for cryptocurrency trading, storage, and payment acceptance. Coinbase provides a user-friendly experience, making it easy for users to buy, sell, and manage their digital assets. It also offers educational content to help users navigate the crypto space.

Ensures accessibility through digital platforms and mobile apps. Provides a user-friendly interface for seamless cryptocurrency transactions. Offers a range of services, including trading, storage, and payment solutions. Promotes financial literacy and education through Coinbase Earn. Attracts users seeking a convenient and secure way to access cryptocurrencies. Simplifies the onboarding process for beginners.

– Users can access Coinbase’s platform through its website and mobile apps, enabling trading and asset management from anywhere. – Coinbase’s user interface is designed for simplicity, making it suitable for both beginners and experienced users. – A variety of services, including Coinbase Pro for traders and Coinbase Commerce for businesses, caters to different user needs. – Coinbase Earn offers educational content and rewards to users who complete lessons on various cryptocurrencies, enhancing users’ understanding of the space. – Coinbase simplifies the onboarding process by providing clear instructions and easy account setup for newcomers.

Revenue Streams

Coinbase generates revenue primarily from trading fees, spread markups, and custody fees. It charges users for cryptocurrency transactions, including buying, selling, and converting digital assets. Coinbase Pro, designed for active traders, offers tiered fee structures. Coinbase also earns income from staking services, where users can earn rewards by holding certain cryptocurrencies.

Relies on trading fees and spread markups as primary revenue sources. Offers tiered fee structures on Coinbase Pro for different user levels. Generates income through custody fees for secure asset storage. Provides staking services for users to earn rewards. Diversifies income streams to maintain financial stability.

– Users are charged trading fees and spread markups when buying, selling, or converting cryptocurrencies on Coinbase’s platform. – Coinbase Pro offers tiered fee structures based on trading volume, providing cost savings for high-volume traders. – Coinbase Custody charges fees for secure storage services, especially for institutions and high-net-worth individuals. – Users can earn rewards through staking services, contributing to Coinbase’s income diversification strategy. – Diversified revenue streams help maintain financial stability, even during market fluctuations.

Marketing Strategy

Coinbase’s marketing strategy includes digital advertising, content marketing, partnerships, and referrals. It focuses on simplifying cryptocurrency for the masses, promoting security and regulatory compliance, and highlighting the platform’s ease of use. Coinbase encourages users to refer others, offering rewards for successful referrals. The platform also provides educational resources through Coinbase Earn.

Utilizes digital advertising and content marketing to reach potential users. Simplifies cryptocurrency through marketing messages. Promotes security, regulatory compliance, and ease of use as key selling points. Encourages word-of-mouth marketing through referral programs. Offers educational resources to enhance cryptocurrency knowledge. Attracts users seeking a trusted and accessible crypto platform.

– Coinbase runs digital ad campaigns that emphasize the simplicity and accessibility of cryptocurrency trading on its platform. – Content marketing efforts include blog posts, articles, and guides to educate users about cryptocurrencies and blockchain technology. – Marketing materials highlight Coinbase’s security measures, regulatory compliance, and user-friendly interface. – Coinbase’s referral program rewards users who refer others to the platform, promoting word-of-mouth marketing. – Educational resources provided through Coinbase Earn help users understand and navigate the crypto space.

Organization Structure

Coinbase operates with a centralized structure overseeing product development, marketing, and customer support. It collaborates with regulators and law enforcement to ensure compliance with financial regulations. Coinbase maintains a strong customer support team to assist users with inquiries, account management, and security-related matters. The platform actively engages with the crypto community and industry partners.

Employs a centralized structure for product development and support. Collaborates with regulators to ensure regulatory compliance. Maintains a dedicated customer support team to assist users. Actively engages with the cryptocurrency community and industry partners. Focuses on security and user education to build trust. Supports regulatory changes and industry developments to stay compliant.

– Coinbase’s product development teams work on enhancing the platform’s features and security measures. – Collaborations with regulators and law enforcement agencies ensure compliance with financial regulations. – Customer support assists users with inquiries, account management, and security-related issues. – Active engagement with the crypto community and industry partners fosters collaboration and knowledge sharing. – Coinbase places a strong emphasis on security and user education to build trust among users. – Staying informed about regulatory changes and industry developments allows Coinbase to adapt to evolving requirements and maintain compliance.

Competitive Advantage

Coinbase’s competitive advantage lies in its user-friendly platform, regulatory compliance, and strong focus on security. It offers a diverse range of cryptocurrencies and services, attracting both beginners and experienced users. Coinbase’s commitment to regulatory compliance and collaboration with authorities builds trust among users and regulators alike. Its educational resources and referral programs contribute to user growth.

Offers a user-friendly platform for cryptocurrency transactions. Emphasizes regulatory compliance and security measures. Provides a diverse selection of cryptocurrencies for trading and investment. Attracts a broad range of users, from beginners to experienced crypto enthusiasts. Builds trust among users and regulators through compliance and collaboration. Encourages user growth through educational resources and referral programs.

– Coinbase’s platform is known for its simplicity, making it accessible to individuals new to cryptocurrencies. – Regulatory compliance and security measures instill trust in both users and regulatory authorities. – A wide range of supported cryptocurrencies and services caters to various user needs. – Coinbase’s user base includes both beginners and experienced cryptocurrency enthusiasts. – Collaborative efforts with regulators and authorities demonstrate Coinbase’s commitment to a compliant and secure environment. – Educational resources and referral programs contribute to user acquisition and growth.

Main individual shareholders comprise co-founders Brian Armstrong (58.5% voting power), Frederick Ernest Ehrsam (25.4% voting power), and other individual investors such as Surojit Chatterjee (current CPO “poached” from Google), Paul Grewal (former magistrate who joined Coinbase as Chief Legal Officer), and venture capitalists who early on invested on Coinbase, like Marc Andreessen (founder of a16z) and Fred Wilson (founder of Union Square Ventures), together with venture capital firms like Andreessen Horowitz, Paradigm, Ribbit Capital and Union Square Ventures.

Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

Coinbase generated $3.108 billion in revenue in 2023, compared to $3.2 billion in revenue in 2022, compared to $7.84 billion in 2021 and $1.28 billion in 2020.

Coinbase generated $1.52B in transaction revenue, $1.4B in subscriptions and services, and $182 million in other revenue for 2023. In 2023, transaction revenue represented 49% of Coinbase’s total revenue, while subscriptions and services represented 45%.

Acorns is a fintech platform providing services related to Robo-investing and micro-investing. The company makes money primarily through three subscription tiers: Lite – ($1/month), which gives users access to Acorns Invest, Personal ($3/month) that includes Invest plus the Later (retirement) and Spend (personal checking account) suite of products, Family ($5/month) with features from both the Lite and Personal plans with the addition of Early.

Started as a pay-later solution integrated to merchants’ checkouts, Affirm makes money from merchants’ fees as consumers pick up the pay-later solution. Affirm also makes money through interests earned from the consumer loans, when those are repurchased from the originating bank. In 2020 Affirm made 50% of its revenues from merchants’ fees, about 37% from interests, and the remaining from virtual cards and servicing fees.

Alipay is a Chinese mobile and online payment platform created in 2004 by entrepreneur Jack Ma as the payment arm of Taobao, a major Chinese eCommerce site. Alipay, therefore, is the B2C component of Alibaba Group. Alipay makes money via escrows transaction fees, a range of value-added ancillary services, and through its Credit Pay Instalment fees.

Betterment is an American financial advisory company founded in 2008 by MBA graduate Jon Stein and lawyer Eli Broverman. Betterment makes money via investment plans, financial advice packages, betterment for advisors, betterment for business, cash reserve, and checking accounts.

Braintree

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

Compass is a licensed American real-estate broker incorporating online real estate technology as a marketing medium. The company makes money via sales commissions (collected whenever a sale is facilitated or tenants are found for a rental property) and bridge loans (a service allowing the seller to purchase a home before the revenue from the sale of their previous home is available).

Dosh is a Fintech platform that enables automatic cash backs for consumers. Its business model connects major card providers with online and offline local businesses to develop automatic cash back programs. The company makes money by earning an affiliate commission on each eligible sale from consumers.

E-Trade is a trading platform, allowing investors to trade common and preferred stocks, exchange-traded funds (ETFs), options, bonds, mutual funds, and futures contracts, acquired by Morgan Stanley in 2020 for $13 billion. E-Trade makes money through interest income, order flow, margin interests, options, future and bonds trading, and through other fees and service charges.

Klarna is a financial technology company allowing consumers to shop with a temporary Visa card. Thus it then performs a soft credit check and pays the merchant. Klarna makes money by charging merchants. Klarna also earns a percentage of interchange fees as a commission and for interests earned on customers’ accounts.

Lemonade is an insurance tech company using behavioral economics and artificial intelligence to process claims efficiently. The company leverages technology to streamline onboarding customers while also applying a financialmodel to reduce conflicts of interest with customers (perhaps by donating the variable premiums to charity). The company makes money by selling its core insurance products, and via its tech platform, it tries to enhance its sales.

Monzo is an English neobank offering a mobile app and a prepaid debit card for consumers and businesses. It was one of the first app-based banks to enter the UK market, founded by Gary Dolman, Jason Bates, Jonas Huckestein, Paul Rippon, and Tom Blomfield in 2015. All were employees of Starling Bank, a similar neobank challenging the dominance of established financial institutions in England. The company enjoys many revenue streams: business and consumer subscriptions, interchange and overdraft fees, personal loans, and more.

NerdWallet is an online platform providing tools and tips on all matters related to personal finance. The company gained traction as a simple web application comparing credit cards. NerdWallet makes money via affiliate commissions determined according to the affiliate agreements.

Quadpay was an American fintech company founded by Adam Ezra and Brad Lindenberg in 2017. Ezra and Lindenberg witnessed the rising popularity of buy-now-pay-later service Afterpay in Australia and similar service Klarna in Europe. Quadpay collects a range of fees from both the merchant and the consumer via merchandise fees, convenience fees, late payment, and interchange fees.

Revolut an English fintech company offering banking and investment services to consumers. Founded in 2015 by Nikolay Storonsky and Vlad Yatsenko, the company initially produced a low-rate travel card. Storonsky in particular was an avid traveler who became tired of spending hundreds of pounds on currency exchange and foreign transaction fees. The Revolut app and core banking account are free to use. Instead, money is made through a combination of subscription fees, transaction fees, perks, and ancillary services.

Robinhood is an app that helps to invest in stocks, ETFs, options, and cryptocurrencies, all commission-free. Robinhood earns money by offering: Robinhood Gold, a margin trading service, which starts at $6 a month, earn interests from customer cash and stocks, and rebates from market makers and trading venues.

SoFi is an online lending platform that provides affordable education loans to students, and it expanded into financial services, including loans, credit cards, investment services, and insurance. It makes money primarily via payment processing fees and loan securitization.

Squarespace is a North American hosting and website building company. Founded in 2004 by college student Anthony Casalena as a blog hosting service, it grew to become among the most successful website building companies. The company mostly makes money via its subscription plans. It also makes money via customizations on top of its subscription plans. And in part also as transaction fees for the website where it processes the sales.

Stash is a FinTech platform offering a suite of financial tools for young investors, coupled with personalized investment advice and life insurance. The company primarily makes money via subscriptions, cashback, payment for order flows, and interest for cash sitting on members’ accounts.

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Wealthfront is an automated Fintech investment platform providing investment, retirement, and cashmanagement products to retail investors, mostly making money on the annual 0.25% advisory fee the company charges for assets under management. It also makes money via a line of credits and interests on the cash accounts.

Zelle is a peer-to-peer payment network that indirectly benefits the banks’ consortium that backs it. Zelle also enables users to pay businesses for goods and services, free for users. Merchants pay a 1% fee to Visa or Mastercard, who share it with the bank that issued the card.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.