A Quick Glance At Inditex, The Spanish Fast Fashion Empire

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue.

Key Components

Inditex business model

Inditex is the holding that controls a set of brands, among them, Zara, one of the dominating brands in the fast fashion industry. In 2017, Inditex comprised eight brands:

Zara

Zara is by far the largest brand in the group, representing over 70% of the group’s net sales.

Pull&Bear

Pull&Bear, with over €1.8 billion in net sales in 2021, Pull&Bear represented almost 7% of the group’s net sales.

Massimo Dutti

Massimo Dutti made over €1.6 billion in net sales in 2021, representing about 6% of the group’s net sales.

Bershka

After Zara, Bershka is the largest of the sister brands in sales in 2021.

Stradivarius

Stradivarius made over €1.8 billion in 2021, representing about 6.7% of the group’s total sales.

Oysho

With a turnover of €600 million, Oysho represented over 2% of the group’s net sales.

Inditex values and key partners

Inditex group core values can be summarized in:

Real-World Examples

AppleMetaSheinTarget

Key Insight

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue.

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue. Spain contributed the most to the fast fashion Empire sales, with nearly 15% of its revenues.

Inditex is the holding that controls a set of brands, among them, Zara, one of the dominating brands in the fast fashion industry. In 2017, Inditex comprised eight brands:

Zara.

Pull&Bear.

Massimo Dutti.

Bershka.

Stradivarius.

Oysho.

Zara Home.

The holding, Inditex, continued to focus on commercial initiatives to grow the value of each brand, expand its stores worldwide, and build up its e-commerce platforms.

Let’s quickly overview each brand part of Inditex Holding.

Zara is part of the retail empire Inditex. It is the leading brand in what has been defined as “fast fashion.” Zara had over €26 billion in sales in 2023 (comprising Zara Home) and followed an integrated retail format with quick sales cycles. Customers can move from a physical to a digital experience.

Zara is by far the largest brand in the group, representing over 70% of the group’s net sales.

With its massive flagship stores worldwide (Madrid, Venice, Mumbai, and many others), Zara created a large, recognized brand in the fast fashion industry.

The company also extended its online presence in Southeast Asia and launched http://www.zara.com in Malaysia, Singapore, Thailand, Vietnam, and India.

Pull&Bear

Pull&Bear generated €2.36 billion in revenue in 2023, €2.15 billion in 2022, and €1.87 billion in revenue in 2021, compared to €1.42 billion in 2020 and €1.97 billion in 2019.

Pull&Bear, with over €1.8 billion in net sales in 2021, Pull&Bear represented almost 7% of the group’s net sales.

The company has also opened up new flagship stores worldwide (like Rue de Rivoli in Paris, Ermou in Athens, and One World in Bangkok).

Massimo Dutti

Massimo Dutti generated €1.65 billion in revenue in 2021, compared to €1.27 billion in 2020 and €1.9 billion in 2019.

Massimo Dutti made over €1.6 billion in net sales in 2021, representing about 6% of the group’s net sales.

The company expanded with its new stores in Valencia and Milan.

Just like Zara’s flagship stores, Massimo Dutti positions itself in exclusive locations but with a minimalist interior design to convey a different style than the sister brands.

Bershka

Massimo Dutti generated €1.84 billion in revenue in 2023, €1.59 billion in 2022, €1.65 billion in 2021, €1.27 billion in 2020, and €1.9 billion in 2019.Bershka generated €2.62 billion in revenue in 2023, €2.38 billion in 2022, and €2.18 billion in revenue in 2021, compared to €1.77 billion in 2020 and €2.38 in 2019.

After Zara, Bershka is the largest of the sister brands in sales in 2021.

Indeed, the company made over €2.7 billion, representing almost 8% of the total group sales.

Like its sister brands, Bershka collaborates with influencers to enhance its brand awareness.

Like the campaign with the Italian rapper, Fedez (Fedez for Bershka).

The company also expanded its operations by opening pop-up stores in New York and Rome.

Stradivarius

Stradivarius made over €1.8 billion in 2021, representing about 6.7% of the group’s total sales.

Like its sister brands, the company has inaugurated a new flagship store in Barcelona.

Oysho

With a turnover of €600 million, Oysho represented over 2% of the group’s net sales.

The Spanish clothing retailer of women’s homeware and undergarments expanded by bringing its store to Barcelona, Madrid, Milan, Doha, Moscow, Paris, Tunisia, Istanbul, Dubai, and Bali.

Inditex values and key partners

Inditex group core values can be summarized in:

1. Strong customer focus.

2. Modesty.

3. Self-reliance.

4. Non-conformism.

5. Teamwork.

6. Creativity.

7. Diversity.

8. Innovation.

The principal partners of the group are:

Employees are considered as any person who works for Inditex Group stores, offices, or logistics centers.

Customers, as anyone who purchases a product sold by Inditex Group’s eight sister brands.

Suppliers as companies that are part of the Inditex supply chain.

Community, as all people or entities that are part of the context of Inditex.

Shareholders as any individual or entity that owns Inditex Group shares.

Inditex follows an integrated model, where the customer journey is driven across several channels.

Still, with a continuous dialogue, from store to online channels, Inditex creates multiple touchpoints with its brands.

Key Highlights

Inditex: A Spanish Fast Fashion Empire with over €27 billion in sales in 2021.

Zara: The leading brand in “fast fashion” with almost €20 billion in sales in 2021. It is the largest brand in the Inditex group, contributing over 70% of the group’s revenue. Zara follows an integrated retail format, allowing customers to move freely between physical and digital experiences.

Pull&Bear: Generated €1.87 billion in revenue in 2021, representing almost 7% of the group’s net sales. It has opened new flagship stores worldwide.

Massimo Dutti: Generated €1.65 billion in revenue in 2021, representing about 6% of the group’s net sales. It expanded with new stores in Valencia and Milan, positioning itself in exclusive locations with a minimalist interior design.

Bershka: Generated €2.18 billion in revenue in 2021, representing almost 8% of the total group sales. Bershka collaborates with influencers to enhance brand awareness and expanded operations by opening pop-up stores in New York and Rome.

Stradivarius: Made over €1.8 billion in 2021, representing about 6.7% of the group’s total sales. It inaugurated a new flagship store in Barcelona.

Oysho: With a turnover of €600 million, Oysho represented over 2% of the group’s net sales. The Spanish clothing retailer expanded by bringing its stores to various locations worldwide.

Inditex Core Values: Strong customer focus, modesty, self-reliance, non-conformism, teamwork, creativity, diversity, and innovation are the core values of the Inditex group.

Principal Partners: The principal partners of the group are employees, customers, suppliers, the community, shareholders, and the environment.

Inditex Integrated Model: Inditex follows an integrated model with multiple touchpoints for customer engagement, both in-store and online, creating a continuous dialogue from store to online channels.

Slow fashion is a movement in contraposition with fast fashion. Where in fast fashion, it’s all about speed from design to manufacturing and distribution, in slow fashion, quality and sustainability of the supply chain are the key elements.

Patagonia is an American clothing retailer founded by climbing enthusiast Yvon Chouinard in 1973 who saw initial success by selling reusable climbing pitons and Scottish rugby shirts. Over time Patagonia also became a fashionable brand also for its focus on slow fashion. Indeed, the company sells high-priced clothing items built to last which it will repair for free.

Patagonia has a particular organizational structure, where its founder, Chouinard, disposed of the company’s ownership in the hands of two non-profits. The Patagonia Purpose Trust, holding 100% of the voting stocks, is in charge of defining the company’s strategic direction. And the Holdfast Collective, a non-profit, holds 100% of non-voting stocks, aiming to re-invest the brand’s dividends into environmental causes.

Fash fashion has been a phenomenon that became popular in the late 1990s and early 2000s, as players like Zara and H&M took over the fashion industry by leveraging on shorter and shorter design-manufacturing-distribution cycles. Reducing these cycles from months to a few weeks. With just-in-time logistics and flagship stores in iconic places in the largest cities in the world, these brands offered cheap, fashionable clothes and a wide variety of designs.

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue. Spain contributed the most to the fast fashion Empire sales, with nearly 15% of its revenues.

LVMH is a global luxury empire with over €86 billion ($93 billion) in revenues for 2023, spanning several industries: wines and spirits, fashion and leather goods, perfumes and cosmetics, watches and jewelry, and selective retailing. It comprises brands like Louis Vuitton, Christian Dior Couture, Fendi, Loro Piana, and many others.

Kering Group follows a multi-brand business model strategy. The central holding helps the brands and Houses part of its portfolio leverage economies of scale while creating synergies. At the same time, those brands are run independently. Based on this multi-brand strategy, Kering is a global luxury brand that made nearly €20 billion in revenue in 2023. Within Kering Group are brands like Gucci, Bottega Veneta, Saint Laurent, and many more—the primary operating segments based on luxury and lifestyle.

Kering is a luxury goods multinational founded in France by François Pinault in 1963. The company, which initially specialized in timber trading, grew via acquisitions and was listed on the Paris Stock Exchange in 1988. Two years later, Kering merged with a French conglomerate interested in furniture, department stores, and bookstores.

The Ultra Fashion business model is an evolution of fast fashion with a strong online twist. Indeed, where the fast-fashion retailer invests massively in logistics and warehousing, its costs are still skewed toward operating physical retail stores. While the ultra-fast fashion retailer mainly moves its operations online, thus focusing its cost centers on logistics, warehousing, and a mobile-based digital presence.

ASOS is a British online fashion retailer founded in 2000 by Nick Robertson, Andrew Regan, Quentin Griffiths, and Deborah Thorpe. As an online fashion retailer, ASOS makes money by purchasing clothes from wholesalers and then selling them for a profit. This includes the sale of private label or own-brand products. ASOS further expanded on the fast fashion business model to create an ultra-fast fashion model driven by short sales cycles and online mobile e-commerce as the main drivers.

Real-time retail involves the instantaneous collection, analysis, and distribution of data to give consumers an integrated and personalized shopping experience. This represents a strong new trend, as a further evolution of fast fashion first (who turned the design into manufacturing in a few weeks), ultra-fast fashion later (which further shortened the cycle of design-manufacturing). Real-time retail turns fashion trends into clothes collections in a few days or a maximum of one week.

SHEIN is an international B2C fast fashion eCommerce platform founded in 2008 by Chris Xu. The company improved the ultra-fast fashion model by leveraging real-time retail, quickly turning fashion trends in clothes collections through its strong digital presence and successful branding campaigns.

Zara is part of the retail empire Inditex. It is the leading brand in what has been defined as “fast fashion.” Zara had over €26 billion in sales in 2023 (comprising Zara Home) and followed an integrated retail format with quick sales cycles. Customers can move from a physical to a digital experience.

Wish is a mobile-first e-commerce platform in which users’ experience is based on discovery and customized product feed. Wish makes money from merchants’ fees and advertising on the platform, and logistic services. The mobile platform also leverages an asset-light business model based on a positive cash conversion cycle where users pay in advance as they order goods, and merchants are paid in weeks.

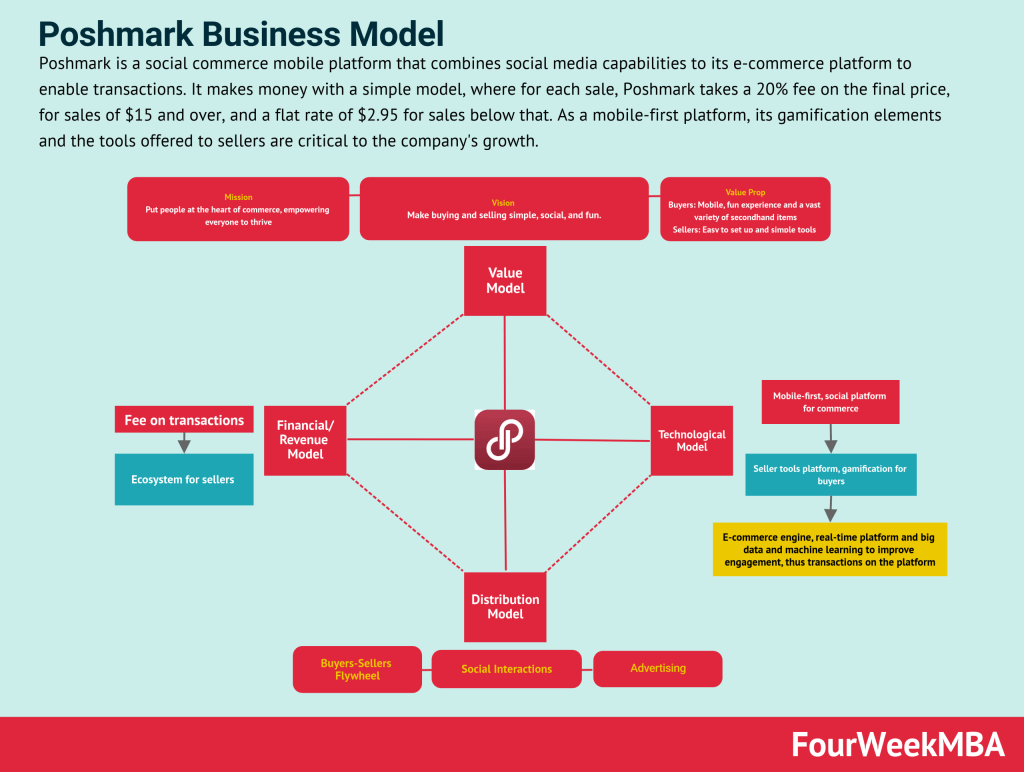

Poshmark is a social commerce mobile platform that combines social media capabilities with its e-commerce platform to enable transactions. It makes money with a simple model, where for each sale, Poshmark takes a 20% fee on the final price for sales of $15 and over and a flat rate of $2.95 for sales below that. Its gamification elements and the tools offered to sellers are critical to the company’s growth as a mobile-first platform.

Hermès revenue grew from €5.96 billion in 2018 to €13.43 billion in 2023. The company generated €6.88 billion in 2019, €6.39 billion in 2020, €8.98 billion in 2021, and €11.6 billion in 2022.

Prada generated €4.72 billion in revenue in 2023, compared to €4.2 billion in revenue in 2022, primarily from its leading brand, Prada, which generated €3.49 billion in 2023. This was followed by Miu Miu, which generated €649 million, and Church’s, which generated €28.5 million.

Massimo Dutti generated €1.84 billion in revenue in 2023, €1.59 billion in 2022, €1.65 billion in 2021, €1.27 billion in 2020, and €1.9 billion in 2019.

Bershka generated €2.62 billion in revenue in 2023, €2.38 billion in 2022, and €2.18 billion in revenue in 2021, compared to €1.77 billion in 2020 and €2.38 in 2019.Pull&Bear generated €2.36 billion in revenue in 2023, €2.15 billion in 2022, and €1.87 billion in revenue in 2021, compared to €1.42 billion in 2020 and €1.97 billion in 2019.

In 2020, the revenue was $555 million.

The revenue decreased in 2021 to $418 million.

However, in 2022, Jimmy Choo’s revenue increased significantly to $613 million.

Miu Miu is a crucial brand part of the Prada Group. Miu Miu generated €648 million for 2023, compared to €431 million in revenue in 2022, €346 million in 2021 and €329 in 2020.

Curch’s footwear is a brand part of the Prada Group. The company generated over €28 million for 2023, compared to €29 million in revenue in 2022 and 2021, and nearly €37 million in revenue in 2020.

What is A Quick Glance At Inditex, The Spanish Fast Fashion Empire?

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue. Spain contributed the most to the fast fashion Empire sales, with nearly 15% of its revenues.

What is Inditex business model?

Inditex is the holding that controls a set of brands, among them, Zara, one of the dominating brands in the fast fashion industry. In 2017, Inditex comprised eight brands:

What is Massimo Dutti?

Massimo Dutti made over €1.6 billion in net sales in 2021, representing about 6% of the group’s net sales.

What are the inditex values and key partners?

Employees are considered as any person who works for Inditex Group stores, offices, or logistics centers.. Customers, as anyone who purchases a product sold by Inditex Group’s eight sister brands.. Suppliers as companies that are part of the Inditex supply chain — as explored in how AI is restructuring the traditional value chain — .

Frequently Asked Questions

What is A Quick Glance At Inditex, The Spanish Fast Fashion Empire?

With nearly €36 billion in sales in 2023, the Spanish Fast Fashion Empire Inditex, which comprises eight sister brands, has grown thanks to a strategy of expanding its flagship stores in exclusive locations around the globe. Its largest brand, Zara, contributed over 70% of the group’s revenue. Spain contributed the most to the fast fashion Empire sales, with nearly 15% of its revenues.

What is Inditex business model?

Inditex is the holding that controls a set of brands, among them, Zara, one of the dominating brands in the fast fashion industry. In 2017, Inditex comprised eight brands:

What is Zara?

Zara is by far the largest brand in the group, representing over 70% of the group’s net sales.

What is Pull&Bear?

Pull&Bear, with over €1.8 billion in net sales in 2021, Pull&Bear represented almost 7% of the group’s net sales.

What is Massimo Dutti?

Massimo Dutti made over €1.6 billion in net sales in 2021, representing about 6% of the group’s net sales.

What is Bershka?

After Zara, Bershka is the largest of the sister brands in sales in 2021.

What is Stradivarius?

Stradivarius made over €1.8 billion in 2021, representing about 6.7% of the group’s total sales.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.