In this episode, Jimmy Soni (Author & speechwriter) and former managing editor of The Huffington Post tells us the story of one of the most interesting startups of the early Internet era. A company that wrote the rules of startup growth, and the business playbook that many startups would later on follow.

Jimmy Soni is also known for A Mind at Play, his award-winning biography of Claude Shannon known as “the father of information theory.”

In this episode, we’re covering the story behind PayPal, based on:

Thanks for joining this conversation, Jimmy, it’s a pleasure to me because you wrote an incredible book called The Founders where you actually tell the story of the PayPal founders, and also the people behind PayPal. Thanks a lot for joining this conversation.

Jimmy:

Well, thank you for having me and for the kind words, and also for taking the time to read the book. It’s funny, the book is longer than I thought it would be. And I think some of my readers have said it’s taken them a little while, so I appreciate you taking a look at an early copy and spending some time reading it.

Gennaro:

Yeah. Actually thank you. Because it was a pleasure, I’m really honored to have had the chance to look at the initial manuscript before the launch, it’s incredible research. You’ve done an incredible job. The story, it’s so incredible, and I want to start from here because of course I know because I already read the manuscript why you were drawn to tell the PayPal story, but let me ask you what drove you to actually cover a story of a company that yes, defined the internet business playbook but was a company that was launched more than 20 years ago.

Yeah. I came at this in a little bit of an accidental way. As my projects tend to go. I had finished up a book on a mathematician and electrical engineer named Claude Shannon and Claude Shannon had worked at Bell Laboratories in the 20th century. And Bell Labs was just the most extraordinary collection of talented people. And they had invented the transistor, they had won multiple Nobel Prizes. They invented the laser, they invented touch-tone dialing.

And I started to think about, and honestly just go down Wikipedia rabbit holes of, what are other places like this, not individual talents, but clusters, groups of talented people? And I looked at Fairchild Semiconductor, which is a famous example. I looked at Zeropark, another example, general magic stood out in history. And someone had done either great books or great documentaries on those three subjects. And so, I fast-forwarded in the history and the late 1990s in Silicon Valley, the place is on fire. There’s so much happening, there’s so much money, so much ambition.

And in that particular environment, you find this company created called PayPal and PayPal turns out to be the finishing school for this whole generation of entrepreneurs. Some are obviously household names, people like Elon Musk, Peter Thiel, Reid Hoffman. But there’s a whole cast of characters there that maybe don’t make the front pages of the headlines, but learned a lot from their time there. And I went into it just not really knowing what I was doing in the sense that I just figured, “Okay. There’s probably a book on this.”

And then when I discovered that there should have needed to be more work done, I just started contacting people. And before long, I discovered that there really was something that happened at PayPal in the late 1990s and early 2000s and that the story deserved to be told, but that’s how I came to it.

Gennaro:

Wow. Interesting parallel with the Bell Laboratories and let’s say a company where interesting people came out and as you said yes, Elon Musk, I think, it’s a name that everyone recognizes today. Of course, names like Thiel and also Reid Hoffman, they’re known in the business world. I’m not sure really if they’re known outside that. I wouldn’t say that my mom knows who like Thiel or Elon or Hoffman are, but those are people that define really the internet as we know it. Let’s get to a little bit of background of the stories, of course, of some of the people that created PayPal.

And in the book, it’s such an interesting account because it’s not just about the stories of, as you said, the main founders, like Thiel, Levchin, and Musk on the other side, but it is also the story of many other people as we see.

How did the PayPal initial founders got together?

Jimmy:

Yeah. What I found to be some of the most interesting parts of the story, and I think part of the reason is it’s very easy to look at these people today and assume that they were destined for success. Just the very quick version of it, or the medium size version of it is on one side of the story, you have a young engineer who is fresh out of the University of Illinois, Champagn, Urbana. His name is Max Levchin and he arrives in Silicon Valley and through a series of events, he meets this young investor named Peter Thiel.

And Peter has been looking to invest in internet businesses. Max has an idea for what would be his next business, and they get together and develop a friendship and Peter makes a decision to invest in Max. And eventually, Peter becomes the CEO of that very tiny company with a few other co-founders who play pivotal roles as well. Ken Howery, Luke Nosek, Yu Pan, and Russ Simmons. That’s a group of six that’s on one side of this. And their initial idea is that they’re going to make it possible for people to be money between PalmPilots.

And so for those listeners of a certain age, they’ll know that PalmPilots are maybe the distant ancestors of your iPhones, and they were handheld devices that were very popular in the mid-1990s and they had introduced an infrared port as one update in the latest series of PalmPilots and Max Levchin’s idea was we can do cryptographically secure transactions between this. So if I’m sitting at lunch with you and I want to send you $10, how cool would it be if I could do that through the infrared port on my PalmPilot?

That was one part of the origin story. The other side of the origin story, which is really never really gotten truly, I think explored is Elon Musk had successfully built and then sold a company called Zip2. And he was thinking about what would come next for him. And from his days as an intern at a bank in Canada, he had thought a lot about how the financial system was running on old technology and that there were unnecessary fees, unnecessary bloat, middlemen, bureaucracy within that financial system.

And he thought, well, look, the internet is fundamentally reducing a lot of that in other industries, it should do so in finance, so he built and found three co-founders for a site that was X.com and X.com was going to be a revolution in finance; banking, insurance mortgages. It was going to do everything. At one point I had employees tell me he would say, “We’re going to be the federal reserve. We’re going to be the world’s financial system.” It was a vast ambition, certainly different from beaming money, but those were the two predecessor companies of the company that becomes PayPal.

Gennaro:

Interesting. And as we see those two companies for a bit of context, those two companies saw one side Confinity, which was as we said, founded by Peter Thiel who had met this brilliant guy, Max Levchin who was the technical guy. They founded Confinity on the one side and then Musk on the other side who had founded X.com. As a side note in the podcast series, I also interviewed Jerry Campbell, who was in charge of product management back in days in the ’90s Compaq and Compaq was the company that actually bought Zip2 for 21 million.

There was the first cash infusion that gave Musk the ability to start his next company, which would turn into PayPal and interesting enough Zip2 would play also an important role in Compaq’s strategy as Compaq also bought as changing at the time called AltaVista because at Zip2 built out local directories. So it was a key tool to have in this expansion strategy of the internet at the time. You see how many interesting things are how they cross each other.

Jimmy:

Yeah. It’s interesting that you mentioned that, and I’m glad you’re mentioning this part of the history because one of the reasons I wrote this book is I had thought, “Okay, it’s fantastic to get all this press attention for the different things that these people do today, like electric cars and rockets, but what if we went back and really asked them about the most boring or perhaps most formative and interesting period in their lives, which is their first series of startups?” And Zip2 was hugely important in Elon’s life.

And I think what’s underestimated and under-covered is the fact that Zip2 broke a lot of technological boundaries. When they were doing the things they were doing with Maps, these are all predecessors of things like Google Maps and Yelp. And there was a lot of technology built-in Zip2 that was really innovative for its time. It was some of the first applications of Java, which had just launched. And so I think, I don’t know that Elon ever actually gets enough credit for the vision and the engineering, especially in the early days of Zip2, which he started with his brother and a co-founder named Greg Kouri.

They were really doing remarkable stuff. I’m glad you mentioned it because I think it’s the easiest thing to overlook. People don’t tend to… They tend to focus on what’s going on in 2022, but back in the mid-1990s, when Elon was basically fresh out of college, he built Zip2 into something really remarkable, what one person labeled at the time, like a mini Microsoft. And so I’m glad that you’re mentioning it because it is a part of the past so we tend to overlook it.

How did Confinity on the one side and X.com on the other side evolve and eventually merge?

Jimmy:

Yeah. It’s one of the central and most interesting parts of this story is let’s say the period in 1999 and very early 2000 when both of these companies get going and the abbreviated version is Confinity launches its product, which is called PayPal with the idea that you and I are going to become… We’re going to move all our money and all our transactions over to PalmPilots, and we’re just going to be beaming each other money left and right. They build an email backup product, and it turns out that the email backup product takes off.

X.com has this other vision, which is we are going to be the place where you put all your and do everything financial, but for it too, the product that is most successful is this emailing money from person to person product. And so, it’s interesting because in both cases, no one expects that the breakthrough product is this emailing money thing, because on both sides, I think there’s a certain amount of… Well, that’s so simple, it’s so much more interesting to do a financial services superstore.

It’s so much technologically interesting to do PalmPilot money beaming, but both of them end up actually having this email money product take off. And part of the reason is that it takes of in a place where that service is needed and that’s eBay. And so, eBay at the time had grown into a public company. It was the world’s largest digital auction house. And for all of that success, it actually hadn’t rationalized how auction buyers and sellers would pay for goods and services. So if I bought something from you, I still had my choice of how I was going to pay you.

And people were still paying through checks and money orders, and these very high friction systems, enter PayPal and X.com’s email money offering, and all of a sudden I’ve got a way to pay you that’s very, very quick. They find that their user growth explodes on this platform where they hadn’t really anticipated their growth. And that begins a race to see who’s going to win there with this seed group of buyers and sellers on eBay who have decided to embrace these two services.

And it’s a foot race the early part of 2000 is this insane battle between these two companies that leads out to obviously some moments of real humor and intensity. But it also, it also paves the way for them to become one company.

Gennaro:

And this is such an interesting point to emphasize because as you said, those companies stumbled upon a use case, which turned out to be a killer commercial use case, and also the two completely different philosophies. On the one side, you had a more technical, practical approach of Confinity with Thiel and of course, Levchin was way more technical, who looked at the PalmPilot as the main application for Confinity. And on the other side, you had the visionary approach of Musk that nonetheless, he wanted to change the whole financial system.

In reality, he figured also for X.com the email feature on top of eBay was getting used a lot. The interesting part is that both those companies eventually converged into the commercial viability which was the possibility to pay through email, but those companies had to acknowledge that actually this was the main killer commercial use case.

And it’s interesting because as you also point out in the book, years after that, for instance, Levchin was still looking at the PalmPilot which was a successful device in the late ’90s, but definitely didn’t get the traction that it was supposed to, and Levchin was still looking at the PalmPilot as the core application. This purist view of the technological world, where you had to be on this technological platform rather than an auction website, like eBay that for how much traction it was getting, it was not as interesting as the founders thought.

And then on the other side also, Musk acknowledging that again, this was the most important application they were supposed to actually go for it. A little bit of evolution there. How did the companies then ended up from becoming successful at least, successful is probably a big word because they were struggling all along.

How did they go (Confinity and X.com) from being companies that were simply enabled to then merging together?

Jimmy:

Yeah. You made such great points and I do want to emphasize a couple of things that you said just in your meditation on their early success. There’s two things. One is just the humor of at one point, Max Levchin actually tries to block eBay IP addresses and the use of the PayPal product on eBay, because he is so horrified by the idea that his technological marvel is going to be used on this auction website that he doesn’t really think very much of at the time. And on the other side of it, Elon has a very big vision for what finance could be. And in some ways, he’s 20 years ahead of his time.

We see a lot of the things and ideas that he was talking about coming into being today. And so, you do have this funny thing of these people are both… They’re so technologically ahead of the curve, but they can’t miss the clear evidence of fast user growth in this very obscure place or what they think of as an obscure place on the internet, which is auction buying and selling. And so, that’s the funny part of it. I think the more interesting part or the lesson that I think people could take is, you shouldn’t mess with success and you shouldn’t ignore success.

Meaning like, it could have gone very differently had Levchin pursued this, like, “We’re not doing this eBay thing, we’re sticking with mobile encryption and security.” Or if Elon had said, “Yeah, that eBay person to person payment thing is nice, but we really got to focus on these other tools and options.” And it is interesting that I think one of the descriptions that I had from David Sacks was, it was the product that ate the company. It was this email money afterthought product that actually became the product that we all know and use today.

David Sacks, “it was the product that ate the company.“

And it changed everything from what the company was focused on to the company’s name. Because if you remember the names of these companies are actually Confinity and X.com and PayPal is a product that Confinity created. And 20 years later, it’s the product that’s left standing. You asked a question about how they came together.

There’s a whole series of complicated wheeling and dealing, but the basic facts are at some point, there’s a recognition on both sides that the only true competitor in town is the person that’s just up the road on University Avenue. X.com’s CEO at the time recognizes like, “Look, we are spending ourselves dry, trying to beat these Confinity guys on eBay, and it’s not good. This isn’t going to end well for anybody.”

And then the folks at Confinity say, “This X.com group has a seasoned entrepreneur, much bigger brand name, they’re moving just as fast as we are, and we’re going to lose because they have more money.”

Both companies are also trying to raise financing rounds in early 2000 at a time when the early signals of the market decline, you’re starting to see them. There’s little wisps of concern that the tech bubble may be a bubble. And both of these companies’ leaders, these are massive people, big personalities, lots of IQ points, but by hook and crook, they actually merge the two companies and close a joint hundred million round of financing just before the markets start to collapse. And there’s not a lot of like… It happens so fast.

What I just described happens in the space of eight to 10 weeks, roughly that these two former competitors now have to become one happy family. And it’s a very, very tense, very hard period, where everyone is working around the clock to continue to service the user growth, but they become one company. And as of, I think the official announcement was in late March, March 30th. As of March 30th, they are united as one fast growing payments company.

Gennaro:

Yeah. And there is one I think event that also made the company merge eventually. And it’s interesting also to probably account a little bit on how the deal eventually closed between the two companies. But mainly as you said, it was critical to close it at the time because without that runaway of money most probably we wouldn’t have any PayPal today because they would have finished up the liquidity to run the business. It was extremely, extremely important.

What happened next? How did Confinity and X.com merge go between the companies and was there a cultural clash?

Jimmy:

Yeah. It’s a really dramatic six months in these people’s lives. And whenever I would interview anyone, the year 2000 was this year, that for a lot of these people was the lo… They had to measure it in dog years. It was the longest year that they could remember. And they worked round the clock under a lot of pressure. As you can imagine, you have these two competitors, they’ve built two separate companies, and now they’re expected to be one company, but we’re not talking about a group of seasoned leaders who are really thoughtfully applying a year’s worth of M&A analysis to figure out what the synergies are.

This is legitimately a merger that is done in the space of two to three months. And it’s not that people weren’t thoughtful about the upside. It’s just that it’s really hard to manage that, particularly when the company is growing by tens of thousands of users every day. The companies merge and there’s a few different things that happen. There’s confusion around who’s going to be in charge and that leads to some things. There’s confusion around what are we trying to do? What is the vision for the company? And there’s some debates around that.

There’s confusions around what the company is going to be called and there’s some debates around that, but the long and short of it is that three month or four-month period from let’s say late March through the beginning of the fall, it’s a really intense time for the company because the PayPal we know today really comes into being during that period. There are tools and products created that PayPal users use to this day that are born in the summer of 2000, Musk become CEO in the summer of 2000. And the company also grows to a significant scale in the summer of 2000.

Now, those are some of the positives of the big developments. There’s also, the company starts to experience huge amounts of fraud and credit card chargebacks, so it loses money. There are some complicated leadership transitions and some battles at the top around things like the name, but more precisely to your question, there’s a debate about technological architecture, and there’s a little bit of background on this, which is, there was a long simmering internet dispute about whether Windows systems were superior or Linux based systems are superior.

And when X.com was first created, it was created on a Windows based system. And when Confinity first created PayPal, it was built to top the Linux system. And these systems have a tough time fusing together and there’s a decision made to rearchitect the paypal.com Linux based site onto a Windows based system. And this causes a schism in the ranks, let’s say, and it causes a lot of difficulty in conservation. You have senior people who flirt with the idea of quitting the company who think that their days are numbered. On the other side, you have people who say, “Hey, this is the only thing that makes sense because we need a stable system and paypal.com is going down once a week for hours, and we’re having to stay up all night to fix it.”

I want to paint the picture of, there’s not one thing that the company is dealing with in the summer of 2000. It’s seven very consequential things. You’ve built your success on a third party platform called eBay, so you have eBay attacking the company. You have credit card companies who are saying, “Wait, you’re using credit cards on paypal.com and you’re underwriting other people’s transactions. Aren’t you a master merchant? Aren’t you doing what we’re supposed to do?”

You have fraudsters who say, “Hey, these guys are giving out 10 and $20 bonuses. This is a gold mine. We’ve got to go and use this and take advantage of this.” And you have these two teams who are rapidly growing with relatively limited experience in this space, particularly at the top. You don’t have decades and decades of, call it company history, let’s say. These are companies that didn’t even exist a year prior to that moment. And so you have all this happening all at the same time, and it leads to some tension at the top and some changes in the company vision.

Gennaro:

Extremely interesting, and in the book, of course, people are going to find a lot of other stories that I don’t want to spoil, that are between the drama and the fan, because some of those stories are just incredible about the deal. Also, let’s say when Musk and Thiel were going to the meeting where they were about to seal the deal between the companies.

There’s one thing interesting that happens, but people can look at it in the book and also the way the negotiation eventually went through, pretty interesting because there were a few turns of events that actually were about to kill the merger between Confinity and the X.com. It was not a smooth one at all. But there was an interesting turn of event. And then also there, as you said, there are many near death experiences that happened which were about to kill the new formed company. It was not like this new formed company finally managed to give safety to the team.

Instead, they kept going through many near death experiences. And even though they had this funding ground, which saved them from the burst of dot-com bubble, yet they had to go through a lot of problems. And the main one of course, was that the main growth channel was the eBay platform. So they were working as if they were a third party application on top of the platform. And they were enabled to do that until eBay could actually decide to shut them down, which as we see it didn’t happen.

But a couple of key points,

One it’s about as you said, even though when they merged up, the two philosophies, even though they merged up eventually in good terms, the two philosophies came about because it was not just a technical problem. The underlying platform was the foundation of the old service. The difference between Musk, which went for the Microsoft enterprise tool was a much more entrepreneurial let’s say, approach where he recognized the stability of the platform and importance to use simple tools so that the code base could be reduced. And then on the other side, you have the more let’s say philosophical approach of Levchin which says Linux is an open source solution it’s superior not just because it’s open source of course there was much more to it, but the problem is by developing on top of the open source, the code base was also much more disorganized, much more complex to handle, I guess, at scale. And those two philosophies came at clash and was one of the reasons why there was eventually, as we see the host of Musk as a CEO.

But before we get to that there is one key interesting aspect, both companies built out the business playbook of internet companies, because they managed to grow virally.

Can you elaborate on the strategies that Confinity and X.com used to actually exponentially grow the user base?

Jimmy:

Yeah, it’s what I think is one of the most interesting parts of the PayPal story is the idea that we take for granted today of viral growth. Viral growth is this commonly used term. And in many ways, as you described the rudiments or the template for this was built in 1999 and 2000 with these two startups on University Avenue. There’s a few ways that they managed to take advantage of the fact that they have traction on eBay and I’ll talk through some of them. One is very simple, which is they use bonus payments.

And so, for Confinity’s PayPal, if I can send you $10 and if you sign up for PayPal I will get another $10. Meaning I have incented all sides of this behavior. It’s not just that I can send you $10, you accept it and we call it a day. It’s that I actually benefit from when you decide that you are going to finish your signing up. And again, some of this is… Yeah, it’s a two sided incentive.

And there’s a way in which it seems so basic to us, but this did take a certain amount of call it ingenuity and also bravado, because they are giving money out on the internet at a time of dialup modems, and limited experience with digital finance, for most customers. One person jokingly called it the largest transfer of venture capital money to college students and human history.

Because you had all these college students signing up and taking advantage of the fact that they could get all their friends to sign up and if 10 friends signed up, they were suddenly a hundred dollars richer. On eBay, the way this works is you have businesses using referral links to sign up users and every single transaction, suddenly the margins change. So if I’m buying a five-dollar touch key on eBay, and you’re giving me $10, I just made five dollars for buying something, right? Exclusive of shipping costs and everything else.

They use bonuses in a really interesting way and an inventive way. And in a way that actually goes beyond just the standard bank model of giving someone a toaster. Because it’s not as though, once I accept the toaster, the bank is getting another toaster. They went a step further and they were always assessing and analyzing. Sometimes they would change the bonus incentives. The Confinity guys were really nervous that X.com’s bonus was twice the size of theirs. So Elon is giving away $20 instead of 10. There’s this incentive piece.

The second thing they do is they get obsessed with taking advantage of the early sparks on eBay and they build tools that specifically cater to eBay power sellers, which are the core eBay community of people listing auctions. They just start building relentlessly, just building tools to scrape eBay webpages, to understand where PayPal’s being used to help eBay buyers insert PayPal logos.

They developed at one point a technology called Auto link, where if a seller is interacting with a buyer and the buyer has used PayPal, even once the PayPal button will show up on that seller’s page. They do all kinds of things to simply goose the growth that they’re already seeing, and to make it essentially seamless for eBay sellers to use PayPal. And I will tell you, I interviewed a few people who were sellers on eBay and looked at a lot of documents and message board posts and other things from this era.

And one of the things that comes back is sellers were always impressed by how quickly the company would create a tool or solve a problem once there was a complaint and I spoke to some people who worked at PayPal’s Omaha customer service headquarters, and it was actually one of the things that even impressed them. They said, “We would send something to Palo Alto and it would be changed or fixed by the next day.” And you can imagine this caused obviously enormous stress long hours, but what it did was it endeared them to this power seller community.

It wasn’t just that they stumbled on eBay, got lucky, called it a day. It was actually that once they noticed this first set of sparks on eBay, they started to do everything they could to increase that fire. The last thing I would say is there’s a quality within the company of pushing every limit you could right up to legal limits, if that makes sense, meaning sure the credit card companies are going to be unhappy, let’s push right up until we can’t anymore and we’ll continue to do what we can to service our user base and focus on the users and the product while treating other rules as fungible.

There’s just a series of innovations that PayPal has to do to deal with fraud, for example, that might have sunk any other company, but there is a particular focus on this group of just pushing those limits as far as we can and then we will fix what we need to fix later. And so, I don’t know what word might capture that quality. It’s part of why the virality is not an accident. It’s not an equation that someone plugged into a spreadsheet. It was the product of a lot of hard work that occurred in late 1999 and in 2000 to manage this and grow these initial sparks on eBay.

Gennaro:

Yeah. Extremely important point to emphasize, they managed to build a business playbook, which is still today, the playbook of startups on the internet when many of those disciplines didn’t even exist yet. They managed to build viral marketing, built into the product what today we would call agile software development, the lean startup methodology, growth tagging, blitzscaling. Many business frameworks that today we give for granted that more or less everyone in the online business world, the digital business world knows were developed at the time of PayPal.

Again, just to emphasize a little bit more viral marketing, where you build virality into the product, the product was a freemium when freemium would become a cool term between the late 2000s, like between 2005, 2006 the agile methodology, where, as you said, when you start building up on eBay and you see that some strategies are working out is not just random success, you are doubling down on that. So it means that you’re looking at the data over and over again.

You are iterating this iterative approach, which it’s a typical agile development and then link startup where really there is a loop in place that is based on what’s working and you keep building on that and growth tagging where you, let’s say, break down the walls between product development and distribution, meaning that the product is what gives you distribution. And that was like a fixation. There was really something that the PayPal team thought about a lot, and Peter Thiel also wrote a book about that, which is Zero to One.

Zero to One is a book by Peter Thiel. But it also represents a business mindset, more typical of tech, where building something wholly new is the default mode, rather than building something incrementally better. The core premise of Zero to One then is that it’s much more valuable to create a whole new market/product rather than starting from existing markets.

And then of course, blitzscaling, which is the term that was coined by Reid Hoffman founder of LinkedIn which, whether you like, or not the concept, I think there is a lot of misunderstanding around it. What he means is that in times of words and especially when you’re developing a new market, you need to really prioritize on speed over everything else, because most probably in a few months, if you don’t do that, you’re going to be dead. So if you’re put in the corner, either you go to war and you Blitz scale, or actually you are going to be dead.

Blitzscaling is a business concept and a book written by Reid Hoffman (LinkedIn Co-founder) and Chris Yeh. At its core, the concept of Blitzscaling is about growing at a rate that is so much faster than your competitors, that make you feel uncomfortable. In short, Blitzscaling is prioritizing speed over efficiency in the face of uncertainty.

Those are very critical points; I think to emphasize. And thanks for making me think about those.

Jimmy:

No, and I couldn’t have summarized it better than you just did and I think what’s interesting is part of the value in coming at this story as somebody who is not in tech and doesn’t have the same familiarity with that language is I was looking at these things as events, and then I would go, and I would research the origin of a phrase like freemium, right?

And I discovered, well, this is exactly the work and thinking around the freemium model was having at PayPal, but they didn’t have the word freemium to call it. I would go and look at the way they organized their tech team into small units that could make changes on their own with just two or three people, and it turned out that agile software development, the first book version of that thinking came out a year or two later.

The freemium – unless the whole organization is aligned around it – is a growth strategy rather than a business model. A free service is provided to a majority of users, while a small percentage of those users convert into paying customers through the sales funnel. Free users will help spread the brand through word of mouth.

It’s interesting that we came at this from both sides. PayPal does pioneer a lot of these features, but it’s not like they’re sitting around thinking, “What are we going to call this methodology that we just created?” What they’re doing is, “Oh my God, we’re losing $12.5 million every month. We’ve got to figure out how to fix this. We’ve got to move very quickly. It’s going to take X, Y, and Z.”

And then these things become principles that apply, obviously in other context, but you’re absolutely right. That a lot of this style of work came into being during this period. And I would say part of the reason it came into being is because the money dried up in Silicon Valley.

One of the things that I think is so easy to forget is that in the year, 2000, once they closed that nine figure round, there’s not going to be another nine figure round for a while, because you have the collapse of many dot-coms that were very high profile, and you have this, what someone who I interviewed called the killing fields, where just all of these companies dried up.

And so, there’s a part of this that is need is the mother of invention. They had to figure out solutions because they felt like if they didn’t, they were the next Pets.com and they were going to go bankrupt.

And so, it’s just interesting. I find that it’s useful to hear someone who’s more well versed in this, describe some of the broader principles because I had to reverse into them, meaning, understanding the events and then looking up and realizing like, wow, there was no book on freemium pricing model that David Sacks could have turned to to think about this.

Gennaro:

Yeah. And again, interesting also what you mentioned. There was definitely the whole playbook that still we have today was determined by the dot-com bubble. No doubt about it because many companies actually had to face near death experiences. And this was not just for PayPal for instance also huge companies, successful companies at the time, for instance Amazon were very, very close to bankruptcy.

Not many people know that, but I think in 2001, I told the story on the blog and on a few articles, which I wrote, but also Amazon was very close to bankruptcy during the birth of the dot-com bubble. And he managed to get the financing deal which gave it really the liquidity to survive those months. But once they passed through this period, they had to change the playbook altogether. For instance, in the case of Amazon, Amazon has had to transition from e-commerce to a platform business model, which is something completely different.

From a company who sold products on the internet to a company who hosted the third party sellers on the internet, and this changed the whole business, because they had to think in terms of platform, they had to think in term of how do we actually create the underlying infrastructure — as explored in the economics of AI compute infrastructure — , which would later become AWS in 2004, 2005 to host those stores? And this is extremely important. And as you said, the lessons of many… There were a couple of huge.

There were many, many bankruptcies, but there were two huge failures that were key lessons, I think for many of the startups during that period, but also later on. One was of course Webvan which had ambition to bring grocery online, which is something that has become viable throughout the 2010 and still now throughout the pandemic where a company worth billions would be built on top of lost my delivery, like Instacart, for instance.

But one was Webvan, which had these ambitious business plan and these ambitious vision, they thrown money without validating the market, without doing a lot of iteration as instead PayPal was doing and they ended up in a very bad situation where they burned one billion of dollars very quickly, and they had to shut down. Another example, which you mentioned, which I think’s very interesting, it Pets.com, which was really another key failure that made those companies change the business playbook and go toward agile and all the other methodologies that we know today.

Just as a reminder I was looking in last days just in 2001, Pets.com, spent a huge sum of money as also mentioned in a Super Bowl event, which definitely in a few months, made the company shut down. Those were key moments for PayPal. And then how was then the later transition from PayPal and Conf… Sorry, Confinity and X.com coming together, Musk getting hosted as a CEO? And also a little bit, how was the experience of Musk as a CEO?

Because I think this is an important point because in many accounts at least over the years, and thanks for putting together the book, because you also changed my mind. I had the impression that Musk as a CEO had not been a great experience for the employees or for the team around him, but from the book, that’s not my understanding.

How did the various CEOs transition from Musk to Thiel and what happened after that?

Jimmy:

Yeah. It’s interesting. I appreciate your point about, in many of these iterations of the PayPal story or versions of the retelling Musk was written out. And I think that if I can offer one important thought on this, that I really think is worth emphasizing, because it’s the easiest thing to miss. There may have been disagreements at the top and there certainly were, and they were disagreements about founder vision, product strategy, technological architecture, naming.

These were serious substantive disagreements about everything from, is he company burning through too much money to make these kinds of changes? But I think the thing that people forget about Elon’s tenure that I hope comes through in the book is that he was an incredible magnet for talented people who stayed with the company even after he was no longer CEO. So, if you just think of a few of the people that Elon was personally responsible for hiring, or certainly were hired under his leadership, Jeremy Stoppelman, who goes on to found Yelp.

Amy Rowe Klement, who goes on to becoming, I think one of the youngest executives at eBay when the company is acquired later. Elon hires Roelof both fresh out business school. In fact, Elon tries a few times to hire Roelof, and today obviously Roelof steers and stewards the Sequoia Capital and becomes PayPal CFO during this period. On and on. You can name person after person where they joined the company in some measure, or perhaps in great measure, because Elon really pushed and persuaded, like, “I have this vision, we’re going to do this thing.”

And I think that’s all often gotten ignored. That you had all these talented people and sure there were some disagreements at the top, but there’s no way to ignore his ability to attract talent. And I think that that’s… I would say by the way, that’s true of Max and Peter as well, but I think they’ve gotten credit for that over the years just the way these stories have been told, and I think that there’s a gentleman named Sanjay Bhargava who joins X.com and interviews with Elon and Elon’s the one who persuades him to join.

And Sanjay comes up with this concept for random deposits that is the way that the company authenticates bank accounts and it is critical to the company’s success. And it’s a story that again, rarely gets told, but part of what rarely gets mentioned is Elon is the one who meets with him, recruits him aggressively, brings him on board, actually hires Anita Bhargava, his wife as well, who plays a big role in this company and really fights for talent when he spots it and finds it.

And so I think that’s actually really important as an important part of this because I think there’s going to be a lot of attention paid to the Max versus Elon thing, but I would actually also emphasize that even in his departure, Elon was very gracious, but more importantly, a lot of the people that he hired go on to become some of the most consequential figures in this story. And then in contemporary Silicon Valley.

And I think, look, there’s plenty of things that are going to be said and written, but I feel like it’s one of the parts of the story that many do people missed, but all I had to do was look at the roster of X.com employees who were there early and say to myself, “Well, yeah. These people came because of Elon. They were inspired by him.” And I had many engineers tell me that despite the disagreements around Windows and Linux, they had joined the company initially because of Elon.

I did want to emphasize that because I don’t want people to think like, “This is just yet another version of this story that is the one side, but not the other.” To your question about what happens, Elon is removed from the CEO position. He remains a member of the board and the company’s largest shareholder, the company announces that it’s going to do a CEO search and they go through this six-month period where they’re interviewing CEOs.

And it’s a very funny process when it’s described to me by others, because basically a number of the key people in the company had decided in their minds that they wanted Peter to be CEO, but they were going to do these fictitious job interviews with other CEO candidates. Eventually, the board decides that it’s going to drop, what is the interim title from Peter Thiel’s title, because he was interim CEO after Elon. They dropped the interim title and he becomes the CEO of PayPal.

And he is the person who is running the company from late 2000 through to its IPO in 2002 and then through its sale to eBay in 2002. And I don’t want to make it seem like once that CEO transition happened, everything was fine. It really wasn’t. The company was still burning up money. They still had to fight fraud. They still had to figure out how they were going to get through everything. And I think one of the things people also overlook is right in the middle of all of that convulsion, September 11th happens. This team actually experienced the September 11th together.

And one of the things that every person I interviewed, 200 plus people, I would ask them about their memories of September 11th and as for any of us, it was a jarring searing day. And so you have all of that and you have, the markets are whip signed during this whole period. The world is down on technology. And so, in all of that, that’s actually what it provides useful context for how hard these years were. One of the things that I joke about in the introduction is it’s really only two years that passed from the merger of X.com and Confinity to the IPO on the Nasdaq.

And in those two years, these people feel like they’ve lived 10 lives. But that is how the story develops in late 2000.

Gennaro:

Yeah, I guess that the experience burned out many of them. I would like to emphasize a couple of points, which I think are extremely important. One is Musk was… Nonetheless the details which people can see in the book. He had eventually a gracious, let’s say he was fine about that at the end and how much of that was shaped by the admiration that Must had for Jobs? I wonder and also, how much of it also shaped the Musk of the later years?

Because I would like to remember also for people that would be listening that also, when Musk created Tesla when it started to develop its distributionstrategy, for instance to the building up the retail shops for Tesla or to sell the cars online. This was a strategy which would cut out the middleman. But when Musk was building out those two, actually he was drawing the lessons from Apple. Indeed, not only that, he also hired the main guy who played a key role in opening up the Apple Stores. And so I think over the years and still today, Tesla falls…

Its strategy is a lot similar to what Apple has done with the main difference though that a lot of processes were internalized way before by Tesla over the years. I’m talking about especially manufacturing where instead Apple managed to keep that as externalized, even though very close controlled by the company.

Was there a big influence of Jobs on Musk thinking?

Jimmy:

I have to be careful in providing an important disclaimer, which is I spent time with Elon talking about X.com and about PayPal and about the years from his collegiate years through 2002, but we didn’t really speak much about what happened in his life after 2002, because I wasn’t there to talk about those things. The one place that he did mention Steve Jobs was, he had a view that’s elegantly expressed in the book about the value of founder CEOs, the value of the founder continuing to steer the company. And he says it’s a great line, “The founder may be bizarre, they may be erratic, but this person’s a creative force.”

And one of the things that he talks about is that when Steve Jobs departed Apple, you lost some of that creative force and when he returned that creative force returned as well. And look, there’s been whole volumes written on that whole section of Apple’s life. And I am not the expert, but it’s the one place where in trying to explain the value of a founder CEO, Elon had mentioned to me the thinking around, Apple’s Renaissance begins when Steve Jobs returns, and there is some value in thinking about the role of a founder CEO as something critical as something set apart.

It’s part of what influenced me to call the book, The Founders, because I think the founding of a company is a different period from any other. It deserves its own special attention. Things get hardened into wet cement at founding that are difficult to dislodge later. But broadly speaking, I’m not the person to comment about how, or whether Apple influenced his thinking about Tesla. What I can say is in his meditation, somewhat in the middle of the book about the value and virtue of founder CEOs, both he and David Sacks speak very eloquently about what a founder brings that others might not.

And I don’t think they’re saying that, best as I can tell, they’re not saying this is true in every case or anything of the sort. They’re simply trying to acknowledge that a founder may have a different level of creative insight of emotional investment and some indefinable quality that they bring to a company. And so, that was the context in which we talked about Apple and about Jobs. Again, I would be speaking out of turn if I took it any further than that.

Gennaro:

Just to leave up just 30 seconds of speculation, do you think, speaking with Musk many, many years after the fact.

Do you think he also left company with the belief that one day he could have come back to for instance PayPal and revolutionize the company, bring it to become this financial behemoth that he had in mind?

Jimmy:

I would say a hundred percent. Yes.

Gennaro:

Cool.

Jimmy:

Look, I think part of the reason is, and let’s drill into it because it’s actually interesting. His underlying vision for what X.com would’ve been is in part upgrading mainframes that banks and governments use that are slow, that cost customers money and that he felt and still feels to this day should be upgraded. It was actually a real pleasure to listen to how impassioned he got about COBOL code and about how he’s talking about how these ancient mainframes run on this ancient code, it still is unnecessary. We should still fix it.

And so, I do think that he had this vision that someone… I think he still believes someone should do this. Someone ought to do this, but the fact is his earliest collegiate passions were electrical energy and space and all the things he’s doing there. And so, he returned to those. The way I described the ending of his PayPal tenure is it gave him creative breathing room to do these other things.

And you can’t ever run these experiments twice, so it’s not a perfect counterfactual, but in some ways I think the world has benefited from the fact that he was not the CEO of PayPal from late 2000 on because he’s applied his work ethic and his vision into other domains. That’s where I netted out on it and what I gathered from all of my discussions with different people at the heart of the story, but also being able to observe it from a critical distance.

Someone had said, an engineer, Scott Alexander had said Jobs made Pixar great because he was fired from Apple and Elon was able to create SpaceX and make Tesla great because he departed X.com. That’s not even my assessment. It’s the assessment of somebody who thinks very highly of them and who was an X.com… He was a very early engineer at X.com and his perspective was maybe it was a good thing for the world that things played out the way they did.

Gennaro:

Interesting point. And I know our time is almost due, I’m not sure how long you can stay…

Jimmy:

Let’s keep going. This is fun and you’re… It’s fun to engage with somebody. Again, I just really appreciate the time you took to dive into this, but then the context that you have, I found a lot of things about not just this company, but late 1990s and mid-1990s internet companies that was engaging to learn about. I spent a lot of time studying the Amazon history in order to understand some of this, but it’s good to… Let’s just keep rolling because this is fun.

Gennaro:

Nice. Okay. How did we eventually go? Because for a little bit of recap here, we had two companies starting on the let’s say on the payment side on the internet, which was not even the main killer application yet, if we can probably say here, they were still too early because other markets would prove to be killer applications on the internet. And one of those was auction, even though those companies was out to acknowledge ethos for what would later become PayPal.

But the interesting part is that eventually they managed to really survive but how did they eventually go from a separated company working on two different use cases on the internet payment industry, they merged together after many neared that experiences, they kept growing the company while hosting various CEOs. And how did they eventually manage to actually merge with eBay? What happened? What were some of the key events that brought to this deal?

Jimmy:

Yeah. If there wasn’t one crisis, there were five and for eBay, PayPal is not a welcome contribution to their platform. They are a nuisance. Imagine that you run a store and another company runs your cash registers, and does so quite well and earns the loyalty of your users. The way this begins is, obviously Confinity is PayPal, and X.com have success on eBay that success continues. eBay power sellers are excited about PayPal. They use it, it grows there, the companies obviously juice that growth through different techniques.

Over time, they develop an interdependent relationship. Meaning eBay was put in the position of, we can’t just shut PayPal down because they help us close transactions and PayPal, anywhere from, at any given time, 50 to 90% of their payment volume was coming from eBay, so they have this challenge of they’re both dependent on one another in some meaningful way. eBay, by the way makes several attempts to acquire PayPal. These acquisitions are always complicated. They don’t quite work out as planned, the prices change, there’s egos involved, there’s tension, drama.

In 2002, PayPal goes public. Actually the 20th anniversary of that IPO is in about three weeks. It’s February 15th. They go public and after they go public, there’s a clear price set for the company. It’s always hard to evaluate what the value of a private company is. But with public companies, you have a share price and you have a total number of shares. It allows for the renewal of negotiations with a clear mark. And what happens is that you have these two individuals who really, both behind the scenes and in front of the scenes help to push the negotiation forward and that is David Sacks and eBay’s Jeff Jordan.

And they meet at a particularly evocative moment, which is this eBay live conference that happens in 2002, PayPal invades this conference, they give out a bunch of PayPal t-shirts, PayPal t-shirts are everywhere. It annoys and wrinkles some of the eBay folks, but they are impressed by the hustle. And Jeff and David say, “Hey, we’re now competing on t-shirts, not just on payment systems. Let’s figure out a way to make this work.” There’s negotiation that still needs to happen.

There’s still tension, but in July of 2002 it’s announced that eBay is going to acquire PayPal and that PayPal will become a wholly owned subsidiary of eBay. And there are a number of reasons why the board votes in favor of this deal after again, years of negotiations and different kinds of back and forth, but the principle one is risk mitigation. There’s just a lot of risk with PayPal depending so heavily on eBay for its payment volume, and they don’t know what’s going to happen.

And so there’s a way in which the competitive pressures are significant. They always feel like they’re on shifting terrain. And as several employees said to me, they were like, “Look, we were tired. We had been fighting this fight for so long and it felt like we were just continuing to fight as opposed to creating value.” And that level of exhaustion as one board member put it, you can’t continue to expect people to work with that for years and years. And so, the announcement is made in July, the deal is formally closed in October and PayPal becomes a wholly owned subsidiary of eBay Incorporated.

Gennaro:

Interesting. The various highlights of the events that brought us here, of course, we went from two companies merging, which were Confinity and X.com becoming PayPal, then PayPal merging with the eBay. eBay who on each side actually tried to, as you said, to actually kill PayPal in various ways by out competing it. But also it owned like a payment system called Billpoint, but it didn’t manage to be successful as they wanted. Also, eBay never really shut down PayPal, even though they could have done it.

Was there any reasons why they didn’t do it? Was there any particular pressure on eBay not to do that?

Jimmy:

Yeah. There were a few different kinds of pressure that I talked through to a few of them. The first is eBay users liked PayPal. You have this situation where if you run a platform and you have this vocal group of users, and they were very vocal who were defending PayPal and saying, “Look, they’re a great service. They do this, they do that. And they’re better than the eBay homegrown service Billpoint. We don’t want to lose PayPal, we’re your users and we’re telling you, we want to stick with PayPal.”

The other thing is from a practical perspective as explained to me that look, even if they shut down PayPal, what eBay would’ve done is also shut down thousands, if not hundreds of thousands of transaction fees that were being paid to them. And so, it was actually not, the way I describe them in the book is it’s not homicide, it’s suicide. You actually have decided to cut off your own… You’re going to have to figure out how to do payments and your users are not going to be happy, but you’re going to lose a certain amount of revenue if you just turned PayPal off straight away.

I think in the early days, by the way, I think in late ’99, or maybe even early 2000, eBay may have been able to flip the switch in that way, but its users had already gone rogue in some sense. And they were paying by checks and money orders and cash, and this and that. And the other thing, and PayPal fulfilled this master merchant credit card function in the middle that nobody had figured out. And so, that’s a part of it.

And then I would say the final thing, it’s a minor threat, but it’s certainly a threat that the PayPal people tried to play up, which is there was a shadow in the air of technology, was the antitrust suit against Microsoft. And so, this idea that anything that smacked of anti-competitive behavior was not going to play well in the press and eBay by this point is a public company. That’s another thing people forget is when PayPal is getting started, they’re a startup. When nest within eBay’s platform, eBay is a publicly traded company subject to rules and regs, and gets a lot of press attention.

The press attention that was directed toward Microsoft during this period was not a good experience for them and it was around antitrust and anti-competitive behavior. What PayPal would do is it would send signals anytime eBay flirted with the idea of shutting the service down or made aggressive motions, they would send these little notes of like, “Well, make sure this doesn’t… This could be construed as anti-competitive behavior and we don’t want that.” And so they were a little bit of that.

Now, I would say that, in looking back at the history, that’s really the thing that led eBay not to shut the service down. It was simply more practical, which is its users use the service and transactions were completed because of the service. And so, the antitrust stuff by five, 10% concern, maybe. It wasn’t that significant at least as has been communicated to me by people who worked at eBay at the time.

Gennaro:

Yeah. Key point. I think as you said, if you have a product that the users love, it’s very hard to shut down and then it’s very important to understand the context for people that are listening. There was the time of the late ’90s when there was the browser wars, where Microsoft had wakened up during 1996, as Netscape had taken over the browsers market.

And it was about to become the next internet platform, but Marc Andreessen which was one of the co-founders of Netscape also awakened Microsoft on an interesting cover, I think in 1996 on time, he said that probably something along the lines of we are going to kill Microsoft. And this definitely awakened Bill Gates who on the strategic side, he decided that the main war to win was that against browsers. And then is when actually Microsoft started to bundle in its office package, the internet Explorer and steal market shares from Netscape.

On the other side, Microsoft also closed deals with AOL just to kill quickly Netscape. There were many interesting terms of event, and it’s very important to understand also the context that public companies, tech companies at the time were very scared to be into an anti-monopolistic situation. And as you said, sometimes also smart executives from PayPal used these strategy as a threatening strategy against eBay to avoid to fall into this practice. And of course, I think the strongest foundation was the fact that PayPal was so much successful on eBay as a platform.

And after that, how was that integration? Because the main story is PayPal went in… There was the merger with eBay, of course as you said, a key point to understand is that PayPal leveraged the negotiation position when it IPOed and with the IPO actually put a price on its valuation, which was unquestionable because was a price given by the market, which at the time was about 1.3, 1.4 billion. And therefore the transaction eventually closed at about 1.5 billion.

But the main story as it goes is that there was many business people say in this way, that there was really older PayPal people left eBay in a few months, but in the book you explain a different story. There were two kind of people that were yes, executives from PayPal but there were employees also, very important senior employees, which managed to stay at eBay.

How was the transition after the acquisition of eBay of PayPal?

Jimmy:

Yeah. It’s one of the things that I was glad for the chance to somewhat correct the record. There are several high profile people at the top who leave the company shortly after the acquisition by eBay in late 2000. People like Max Levchin and David Sacks and Peter Thiel, definitely depart, there are a variety of reasons, personal and otherwise for that, they wanted to go do other things. They had other passions. Max starts to explore the academic track for a brief period.

But one of the things that gave rise too, is the false narrative that eBay lost everybody, lost all the most talented people, which is just not true. There are so many people who worked at PayPal who stayed with eBay for anywhere from one year to, there are still employees, PayPal, or eBay today who were there from these early days, and there are any number of reasons they stayed.

And part of what happened is that these employees all had the experience of what it was like to really go through the acquisition, to continue to work on a larger team, to learn about new products, tools, and services, to have access to things like management training. And so, I wanted to tell the story because it had never really been covered, but some of Silicon Valley’s most important people today, CEOs of major household name companies stayed after the acquisition, in some cases thrived at eBay and there were cultural hiccups to be sure, and I document those as well.

But I think the idea that it was just this mass exodus and everybody talented left. That’s just not true, and there are countless examples you can point to. And I think it’s important to emphasize those because part of what you look back in hindsight, in all this is eventually eBay took PayPal and spun it back out and had another IPO. And it did quite well for the amount of money that they invested at the outset. And I think there’s always this revisionist history around whether eBay handled the integration well, or didn’t handle it well.

And I think I heard a decent number of stories that lead me to believe that it wasn’t the best integration, but what I wanted to make sure people understood is that it wasn’t as though 220 pre IPO PayPal employees suddenly left and turned out the lights, just handed the platform over to eBay. You had a whole generation of super talented people who joined eBay from, let’s say one year or five years, and then went off and did their own things or didn’t.

And I’m glad for the chance to actually explore some of that, because again, you get the exodus of the highest, highest profile people without this real acknowledgement that now, but you could have stayed, good careers, it was a great place for many of them to work depending on the team they were on. And then many of them went on to go do other things and create other ventures.

Gennaro:

Yeah. And that’s a very important point to stress out. As you said, some of the executives they left because they had managed to actually achieve in part their mission and they actually left also because they wanted to start something on their own. The other point is also very interesting on the fact that I think it’s also about time windows, windows of opportunity, meaning that there was a time in which auction and e-commerce were the most important applications on the internet.

And they still are today, but there was then a time window, especially in the 2010 going forward were internet payments become extremely important, and therefore PayPal eventually ended up being larger than eBay. eBay initially didn’t want to span off the company, drag off until 2014 when eventually eBay span off the company. And for a bit of context as of today, when we look at the market capitalization, of course, there was a huge sell off since October of 2021, but the capitalization in January 2022, sorry, for PayPal, it’s 185 billions and for eBay, it’s 36 billions.

It’s interesting to look that PayPal became many times over eBay and that’s also because again, payment on the internet finally became viable. Not only with mobile became way, way bigger as a market. The market opportunity became way, much bigger than auctioning. And so, I think this is also very important. Let’s finish this up then with some of the key people that really were the main factor in the PayPal success.

Who were some of the key people behind the PayPal story?

Jimmy:

Yeah. It’s hard to isolate the list in a way, because as I think, hopefully it comes across in the book, there’s a tendency to take the wins from PayPal and put them at the feet or ascribe them to just a few people. But, there’s a broad range of people who make this company successful. And it’s everyone from people who wrote code to people who thought fraud, to everything. I think what happens with this group and at the heart of your question is, what happens with this group?

And one of the descriptions that was given to me by Peter Thiel was, these people, and I think he said some version of this in other places, “We all learned that doing an internet business was hard, but doable. Meaning if it had been an easy success, we might have learned the wrong lessons. And if it had been hard and we failed, we might have learned that something like this is not possible, but we learned…” As he put it, “…the right lessons, which is, this is going to be very hard, but you can be successful.”

And so, obviously the alumni from this group have gone on to do any number of things. And to this day, they are continuing to create, to innovate, build companies and fund companies. And I think obviously like a lot of your listeners probably pay attention to their day exploits more than they maybe pay attention to those PayPal years.

But I found a lot of what they’ve brought to those other industries, the energy, the ambition, the focus on product, the focus on product distribution, the ethos of a small team that can go into an industry that you don’t know anything about, and change it from the ground up. A lot of that, you discover it during the PayPal years. And for particularly, I would say for the younger folks for whom this was either their first job out of college or the job just after their first job out of college, I had someone tell me something like, “I just didn’t know that things were supposed to be any different.”

This was the sum total of my professional experience was this crazy company where we were taking on the banks and taking on and so. And so, I think that’s, focusing on individual names, the readers will know the individual names and what they’ve gone on to do, but I think my thesis is that this created a custom mind in the same way that any intense four to five-year experience will create a way you do things for the rest of your life, whether that’s college or the military. This was that for this generation of people. And it came at a time when dot-coms… It started when dot-coms were…

They were the hottest thing and saw them through a period where people said the internet was just a fad. And they emerged on the other side of that as true believers in technology who had seen a product succeed and had managed to build that into a public company and then have it acquired by a bigger public company. And so, there’s a way in which the lesson that they took was, well, you can do this. You don’t have to know everything about chargebacks or about person to person payments.

You can figure it out as you go along. And I think that ethic has actually been brought forward to other companies and domains as well.

Gennaro:

Yeah. And of course, in a group of people that made the PayPal successful, this was made of incredible men and women who actually made these company possible in the first place. And actually were also people that followed the main co-founders to create many other interesting projects as people will see in the book. Jimmy, thanks a lot for this conversation. I hope that in the future or in the coming weeks, we can have probably another conversation about the Bell Labs, which to me it’s also another interesting topic.

Look at the innovation, how it worked way before the internet happened. That would be an interesting conversation as well.

Jimmy:

Yeah. And for that one, I might send you to my friend, Jon Gertner who wrote a book called The Idea Factory, which everyone should read-

Gennaro:

Nice.

Jimmy:

…which is a really great book about Bell Labs and it’s an amazing place in the same way that PayPal is and just the people they attracted and what they learned there.

Gennaro:

Yeah, absolutely. That would be amazing. Thanks a lot for joining me, Jimmy. Was a pleasure. Thanks. Thanks a lot.

Jimmy:

Yeah. Thank you for taking so much time to do this.

Gennaro:

Absolutely. It was my pleasure.

Key highlights

The story of PayPal is so interesting, for a few reasons that we can sum up below.

So different and yet so close

The story of PayPal has so many turns of events, that seem so unprobable. From two startups (Confinity and X.com) which were two startups operating in the internet payment industry. Yet, while they where neighbors, they also recognised how different was each other’s vision.

Confinity had started to build a valuable company by looking at a narrow application (enabling payments through the PalmPilot). X.com wanted to be a financial institution. Those two companies not only had a fundamental different vision, they also had a different philosophy in terms of the underlying technological infrastructure they had developed (X.com leveraged the Microsoft stack, where Confinity leveraged on Linux, open source software).

Eventually, those two companies ended up to merge, to become one, PayPal.

The Merger: From grandiose vision to commercial killer application

While both companies had some grandiose visions, the market also turned out in a direction that none of them had forseen. Enabling email payments which was supposed to be “side feature” became the killer commercial applications for both companies.

They also figured that their tools had become extremely relevant on eBay. This triggered an irreversible journey. Where both startups understood the path to growth, leveraged on virality to get there, and eventually decided to merge to tackle the market.

The new Internet business playbook

During this process a new business playbook has been developed. Which today we give for granted but at the time it didn’t exist. This playbook comprised concepts like:

The founding members of PayPal would go on to build many other valuable companies, and found the next wave of the Internet, what we now call Web 2.0 or Web2.

PayPal was first founded in 1998; it was called Confinity (among its founders was Peter Thiel); later, it merged with X.com, its major competitor, founded by Elon Musk (which would become known for other companies like Tesla and SpaceX). From this merger, PayPal was born. In 2002, PayPal was bought by eBay for $1.5 billion. eBay spun off PayPal in 2015, which would be listed as an independent entity. Today, PayPal owns brands like Braintree, Venmo, Xoom, and iZettle. Today, PayPal is mostly owned by institutional investors like The Vanguard Group (8.4%) and Blackrock (6.7%)

PayPal makes money primarily by processing customer transactions on the Payments Platform and other value-added services. Thus, the revenue streams are divided into transaction revenues based on the volume of activity or total payments volume—and value-added services, such as interest and fees earned on loans and interest receivable. In 2023, PayPal generated nearly $30 billion in revenues and $4.24 billion in net profits.

PayPal is a two-sided marketplace which collects a transaction fee for each payment that happens via the platform. PayPal’s flywheel is based on creating a stronger and stronger network, where the company provides a suite of services to merchants, and consumers are given affordable digital payment solutions. In 2022, PayPal processed over $1.35 trillion in global payments.

PayPal processed $1.53 trillion in payment volume in 2023, $1.36 trillion in payment volume in 2022, and $1.25 trillion in 2021—a growth of 12.5% year over year. In 2020, PayPal passed a trillion-dollar in payment volume, with $936 billion processed via the platform.

In 2023, PayPal generated nearly $30 billion in revenue compared to over $4.24 billion in profits. Compared to over $27.52 billion in revenue and over $2.42 billion in revenue in 2022.

In 2023, of nearly $30 billion in revenue, nearly $27 billion came from transaction revenues. Thus, transaction revenue represented over 90% of total revenue, while revenues from other value-added services (primarily comprising revenue earned through partnerships, interest and fees from merchants and consumer credit products, interest earned on certain assets underlying customer balances, referral fees, subscription fees, and gateway services) were over $2.91 billion, representing about 9% of PayPal’s total revenue.

PayPal had 426 million active accounts in 2023, a 2% slowdown compared to 435 million active accounts (users) in 2022, back to the 2021 level, when PayPal had 426 million active accounts.

The PayPal transaction per active account/user is a critical metric to measure the level of usage of PayPal. In 2023, the transaction per active account grew to 58.7, compared to 51.4 in 2022 and 45.4 in 2021. Thus, each active account has performed (on average) nearly 59 transactions via PayPal in 2023.

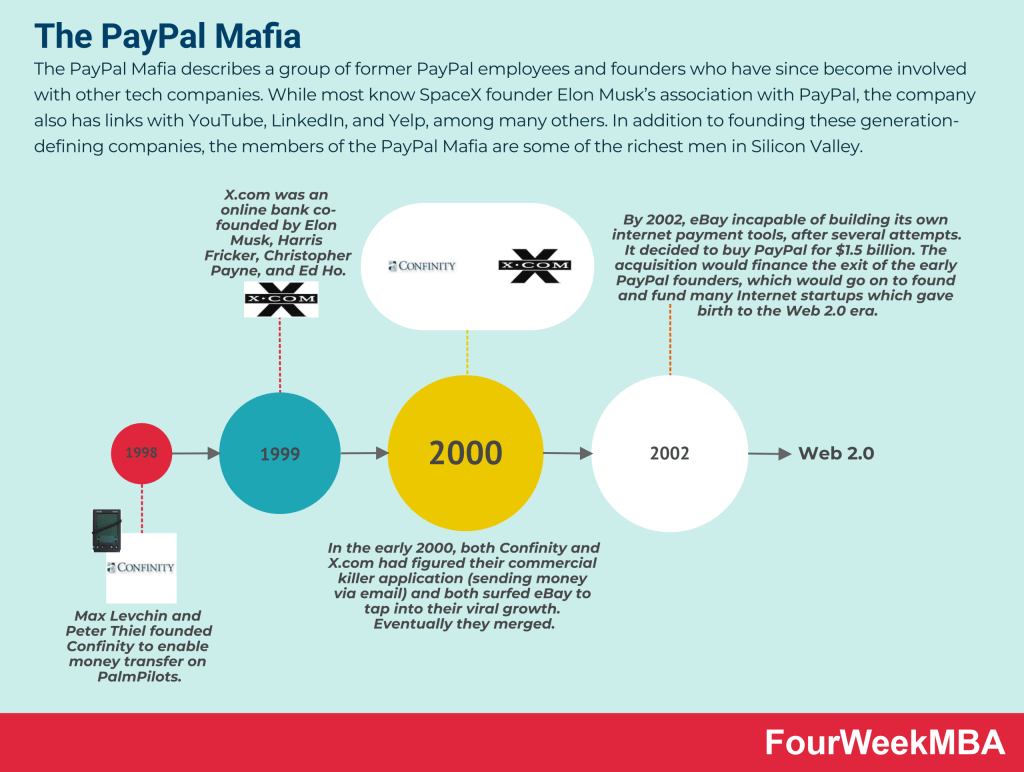

The PayPal Mafia describes a group of former PayPal employees and founders who have since become involved with other tech companies. While most know SpaceX founder Elon Musk’s association with PayPal, the company also has links with YouTube, LinkedIn, and Yelp, among many others. In addition to founding these generation-defining companies, the members of the PayPal Mafia are some of the richest men in Silicon Valley.

Acorns is a fintech platform providing services related to Robo-investing and micro-investing. The company makes money primarily through three subscription tiers: Lite – ($1/month), which gives users access to Acorns Invest, Personal ($3/month) that includes Invest plus the Later (retirement) and Spend (personal checking account) suite of products, Family ($5/month) with features from both the Lite and Personal plans with the addition of Early.

Started as a pay-later solution integrated to merchants’ checkouts, Affirm makes money from merchants’ fees as consumers pick up the pay-later solution. Affirm also makes money through interests earned from the consumer loans, when those are repurchased from the originating bank. In 2020 Affirm made 50% of its revenues from merchants’ fees, about 37% from interests, and the remaining from virtual cards and servicing fees.

Alipay is a Chinese mobile and online payment platform created in 2004 by entrepreneur Jack Ma as the payment arm of Taobao, a major Chinese eCommerce site. Alipay, therefore, is the B2C component of Alibaba Group. Alipay makes money via escrows transaction fees, a range of value-added ancillary services, and through its Credit Pay Instalment fees.

Betterment is an American financial advisory company founded in 2008 by MBA graduate Jon Stein and lawyer Eli Broverman. Betterment makes money via investment plans, financial advice packages, betterment for advisors, betterment for business, cash reserve, and checking accounts.

Braintree

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

Compass is a licensed American real-estate broker incorporating online real estate technology as a marketing medium. The company makes money via sales commissions (collected whenever a sale is facilitated or tenants are found for a rental property) and bridge loans (a service allowing the seller to purchase a home before the revenue from the sale of their previous home is available).