A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks. The earliest neobanks emerged from the ashes of the 2008 Global Financial Crisis as consumer confidence in the banking sector plummeted to historically low levels. Neobanks capitalized on the resentment felt toward traditional banks by offering a seamless online experience under a no or low-fee service model.

Visual Overview

Key Components

Introduction

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

Common characteristics of a neobank

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

Popular neobanks

Lastly, let’s take a look at some of the most popular neobanks on the market today:

List of FinTech Business Models

Read Next: Fintech Business Models , IaaS, PaaS, SaaS , Enterprise AI Business Model , Cloud Business Models .

Strengths

✓Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online…

✓Low Fees: Many Neobanks operate with lower overhead costs compared to traditional banks, allowing them to offer competitive fee structures.

✓Innovative Features: Neobanks often leverage technology to introduce innovative features and services that enhance the banking experience.

✓Financial Inclusion: Neobanks may cater to underserved or unbanked populations by providing access to basic banking services without the…

✓Agility and Flexibility: Neobanks are typically more agile and responsive to customer needs compared to traditional banks, thanks to their…

✓Limited Product Offerings: Neobanks may have a limited range of financial products and services compared to traditional banks.

Limitations

—

Real-World Examples

AirbnbAlibabaPaypalStripeUber

Quick Answers

What is Introduction?

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

What is Common characteristics of a neobank?

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

What are the advantages?

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch..

Key Insight

Today, neobanks are transforming the sector in a way not dissimilar to Airbnb in accommodation and Uber in personal transportation. Recent data shows that 6% of all American adults have a digital bank account , which equates to around 15.56 million people. This number is expected to increase to just over 39 million by 2025 .

Exec Package + Claude OS Master Skill | Business Engineer Founding Plan

FourWeekMBA x Business Engineer | Updated 2026

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

A neobank does not use technology to attract customers per se. Nevertheless, the technology appeals to savvier consumers who prefer to do their banking in a mobile app. Most neobanks partner with traditional banks to insure customer funds and do not tend to offer credit as a general rule.

Popular neobanks in the United States include Chime, Varo Bank, and MoneyLion. All three sell various products designed to help consumers improve their financial literacy and reduce fees.

Aspect

Explanation

Definition

A Neobank, also known as a digital bank or online-only bank, is a financial institution that operates exclusively online and offers banking services to customers without physical branch locations. Neobanks leverage technology and digital platforms to provide a range of financial services, including savings accounts, checking accounts, payment processing, lending, and often feature user-friendly mobile apps and websites for easy access and management of accounts. Neobanks often focus on providing a seamless and convenient banking experience with competitive fees and rates.

Key Concepts

– Digital-Only: Neobanks do not have brick-and-mortar branches and rely on digital channels for customer interactions. – Technology-Centric: They leverage technology, automation, and data analytics to streamline banking operations. – User Experience: Neobanks prioritize user-friendly interfaces and mobile apps for customer convenience. – Competitive Offerings: They often offer competitive fees, rates, and innovative financial products. – Accessibility: Neobanks aim to make banking services accessible to a broader range of customers through digital means.

Characteristics

– No Physical Branches: Neobanks operate without traditional physical branch locations. – Digital Services: They offer a wide range of banking services through web and mobile applications. – Fintech Integration: Neobanks often integrate with financial technology (fintech) services for enhanced offerings. – Low Overheads: Operating costs are lower due to the absence of physical branches. – Customer-Centric: They prioritize customer-centric design and user experience.

Implications

– Convenience: Neobanks offer convenient, 24/7 access to banking services via digital devices. – Cost Savings: They often have lower fees and competitive interest rates due to reduced overhead. – Financial Inclusion: Neobanks may improve financial inclusion by providing services to underserved populations. – Disruption: Traditional banks face competition and may need to innovate to remain competitive. – Security: Cybersecurity is a crucial concern in the digital banking landscape.

Advantages

– Accessibility: Neobanks offer accessible banking services to individuals who prefer digital banking. – Lower Fees: They often have lower or no fees for common transactions. – Innovation: Neobanks introduce innovative financial products and features. – User-Friendly: Customer-centric design results in user-friendly interfaces. – Convenience: Banking can be conducted from anywhere with an internet connection.

Drawbacks

– Limited Services: Neobanks may not offer the full range of services provided by traditional banks. – Security Concerns: Online banking involves cybersecurity risks, and customers need to be vigilant. – Trust and Regulation: Some customers may have trust concerns, and regulatory compliance is essential. – Dependence on Technology: Outages or technical issues can disrupt service. – Lack of Physical Presence: For some, the absence of physical branches can be a drawback.

Applications

Neobanks primarily serve as digital banking institutions accessible through web browsers and mobile apps. They cater to individuals seeking convenient and cost-effective banking solutions and may also be integrated with other fintech services.

Use Cases

– Personal Banking: Individuals opt for Neobanks for personal banking needs, including savings and checking accounts. – Business Banking: Neobanks offer business accounts and financial tools for entrepreneurs and small businesses. – International Travel: Travelers may use Neobank services for convenient international transactions. – Financial Inclusion: Neobanks may provide banking services to unbanked or underbanked populations. – Fintech Integration: They integrate with fintech apps and services for enhanced financial management.

Introduction

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

The earliest neobanks emerged from the ashes of the 2008 Global Financial Crisis as consumer confidence in the banking sector plummeted to historically low levels. Neobanks capitalized on the resentment felt toward traditional banks by offering a seamless online experience under a no or low-fee service model.

Today, neobanks are transforming the sector in a way not dissimilar to Airbnb in accommodation and Uber in personal transportation. Recent data shows that 6% of all American adults have a digital bank account, which equates to around 15.56 million people. This number is expected to increase to just over 39 million by 2025.

Common characteristics of a neobank

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

It should also be noted that neobanks do not use technology to attract customers per se. Instead, the technology is used to streamline processes, reduce fees, and then pass those savings on to customers.

The vast majority of neobanks also differ from traditional banks in the following ways:

They are not chartered as banks. In other words, their operations are not governed by bank-specific state or federal regulations. Having said that, neobanks do partner with traditional banks to insure customer deposits.

Neobanks do not extend traditional forms of credit to consumers such as an account overdraft. Their products may be more limited as a result and be restricted to checking and savings accounts, money transfer and payment services, and educative tools that increase financial literacy such as budget or investment trackers.

They use everything from big data to artificial intelligence to help consumers manage their money. This may include alerting the customer to unused subscriptions or unusually high bills. Some neobanks even help their users switch to cheaper electricity providers.

Advantages:

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch.

Low Fees: Many Neobanks operate with lower overhead costs compared to traditional banks, allowing them to offer competitive fee structures. Neobanks may waive account maintenance fees, minimum balance requirements, and overdraft fees, making them an attractive option for cost-conscious consumers.

Innovative Features: Neobanks often leverage technology to introduce innovative features and services that enhance the banking experience. These may include budgeting tools, real-time spending alerts, automated savings programs, and seamless integration with third-party financial apps.

Financial Inclusion: Neobanks may cater to underserved or unbanked populations by providing access to basic banking services without the barriers associated with traditional banks, such as credit checks or physical branch requirements. This promotes financial inclusion and expands access to banking services for a broader demographic.

Agility and Flexibility: Neobanks are typically more agile and responsive to customer needs compared to traditional banks, thanks to their leaner organizational structure and digital-first approach. They can quickly adapt to market trends, introduce new products, and improve service offerings based on customer feedback.

Disadvantages:

Limited Product Offerings: Neobanks may have a limited range of financial products and services compared to traditional banks. They may not offer services such as mortgage loans, business banking, or investment products, limiting their appeal to customers with diverse financial needs.

Security Concerns: The digital nature of Neobanks introduces cybersecurity risks, such as data breaches, identity theft, and fraud. Customers may be concerned about the security measures in place to protect their personal and financial information, especially given the increasing frequency of cyberattacks.

Dependence on Technology: Neobanks rely heavily on technology platforms and third-party providers to deliver their services. Any disruptions or outages in these systems, whether due to technical issues, cyberattacks, or system failures, can impact the availability and reliability of banking services for customers.

Regulatory Challenges: Neobanks must navigate complex regulatory frameworks and compliance requirements in the jurisdictions where they operate. Compliance with regulations related to banking licenses, anti-money laundering (AML), know-your-customer (KYC) requirements, and consumer protection laws can be challenging and resource-intensive.

Lack of Physical Presence: Unlike traditional banks with physical branches, Neobanks operate solely through digital channels. While this offers convenience for tech-savvy customers, it may pose challenges for individuals who prefer in-person interactions or require assistance with complex financial matters.

Popular neobanks

Lastly, let’s take a look at some of the most popular neobanks on the market today:

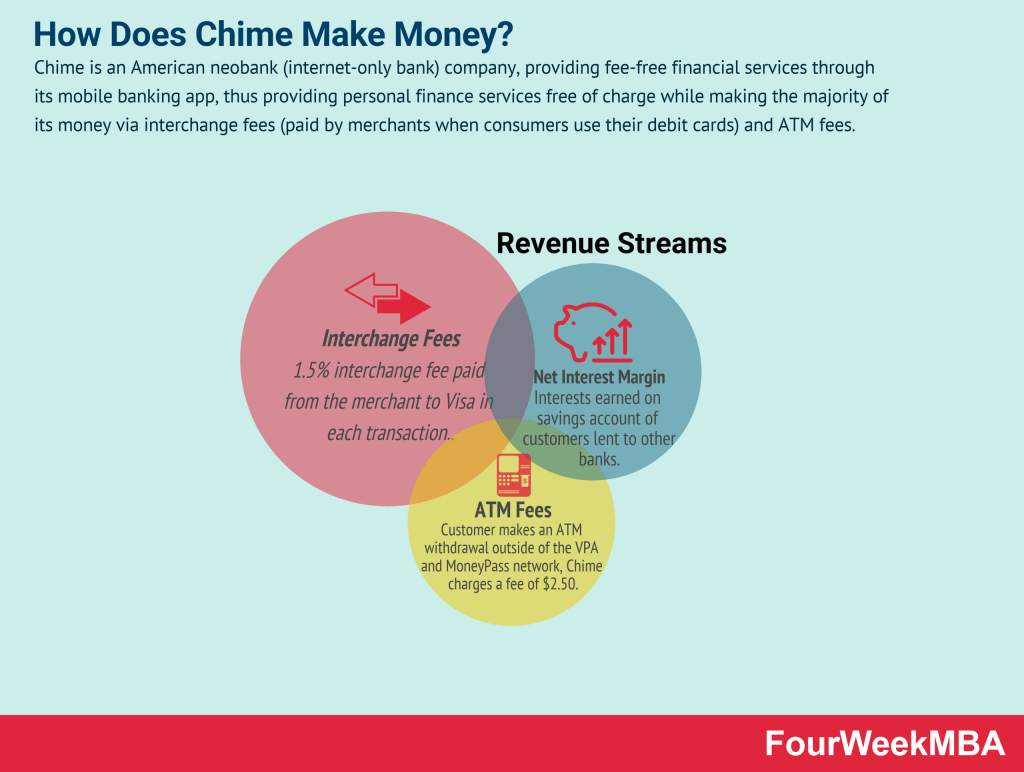

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

The most popular in the United States with over 13 million customers and a valuation of $25 billion. True to type, Chime eliminates many of the fees associated with traditional banks and also provides consumers with an opportunity to build their credit.

Varo was founded as a neobank but also received a full-service national charter in July 2020 to allow it to operate as a traditional bank. Varo boasts no minimum balance, no monthly fees, no credit checks for new customers, no overdraft fees, and a network of over 55,000 fee-free ATMs.

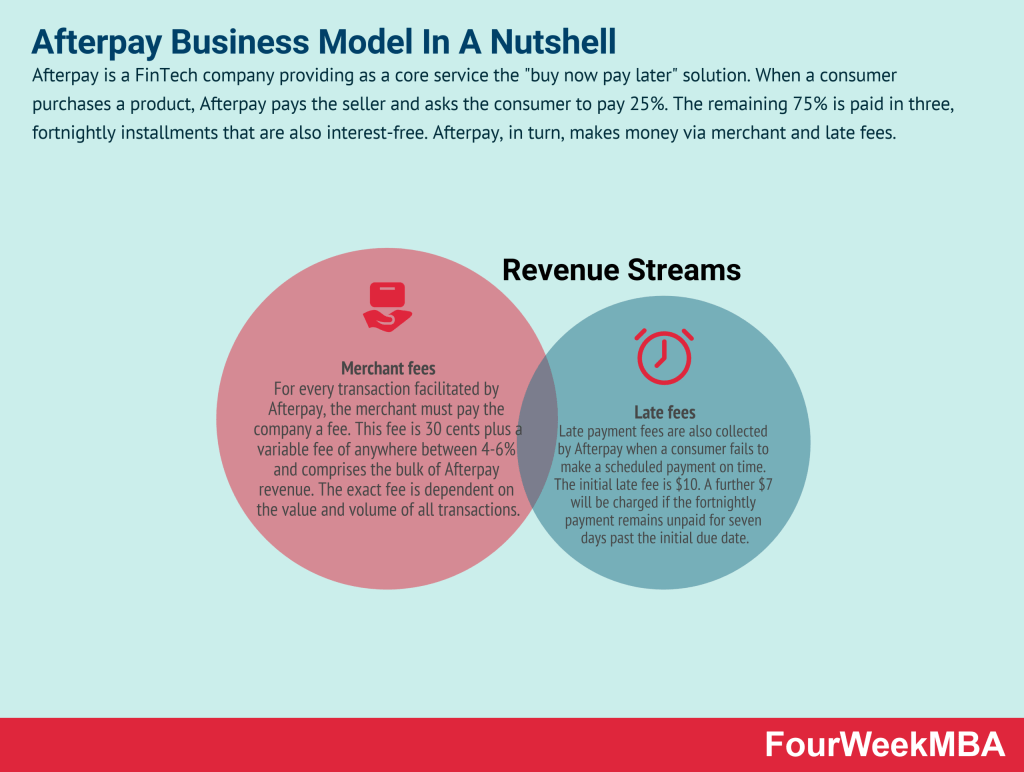

Afterpay is a FinTech company providing as a core service the “buy now pay later” solution. When a consumer purchases a product, Afterpay pays the seller and asks the consumer to pay 25%. The remaining 75% is paid in three, fortnightly installments that are also interest-free. Afterpay, in turn, makes money via merchant and late fees.

Quadpay was an American fintech company founded by Adam Ezra and Brad Lindenberg in 2017. Ezra and Lindenberg witnessed the rising popularity of buy-now-pay-later service Afterpay in Australia and similar service Klarna in Europe. Quadpay collects a range of fees from both the merchant and the consumer via merchandise fees, convenience fees, late payment, and interchange fees.

Klarna is a financial technology company allowing consumers to shop with a temporary Visa card. Thus it then performs a soft credit check and pays the merchant. Klarna makes money by charging merchants. Klarna also earns a percentage of interchange fees as a commission and for interests earned on customers’ accounts.

SoFi is an online lending platform that provides affordable education loans to students, and it expanded into financial services, including loans, credit cards, investment services, and insurance. It makes money primarily via payment processing fees and loan securitization.

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Fintech business models leverage tech and digital to enhance the financial service industry. Fintech business models, therefore, apply tech to various financial service use cases. Fintech business model examples comprise Affirm, Chime, Coinbase, Klarna, Paypal, Stripe, Robinhood, and many others whose mission is to digitize the financial services industry.

Acorns is a fintech platform providing services related to Robo-investing and micro-investing. The company makes money primarily through three subscription tiers: Lite – ($1/month), which gives users access to Acorns Invest, Personal ($3/month) that includes Invest plus the Later (retirement) and Spend (personal checking account) suite of products, Family ($5/month) with features from both the Lite and Personal plans with the addition of Early.

Started as a pay-later solution integrated to merchants’ checkouts, Affirm makes money from merchants’ fees as consumers pick up the pay-later solution. Affirm also makes money through interests earned from the consumer loans, when those are repurchased from the originating bank. In 2020 Affirm made 50% of its revenues from merchants’ fees, about 37% from interests, and the remaining from virtual cards and servicing fees.

Alipay is a Chinese mobile and online payment platform created in 2004 by entrepreneur Jack Ma as the payment arm of Taobao, a major Chinese eCommerce site. Alipay, therefore, is the B2C component of Alibaba Group. Alipay makes money via escrows transaction fees, a range of value-added ancillary services, and through its Credit Pay Instalment fees.

Betterment is an American financial advisory company founded in 2008 by MBA graduate Jon Stein and lawyer Eli Broverman. Betterment makes money via investment plans, financial advice packages, betterment for advisors, betterment for business, cash reserve, and checking accounts.

Braintree

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

Compass is a licensed American real-estate broker incorporating online real estate technology as a marketing medium. The company makes money via sales commissions (collected whenever a sale is facilitated or tenants are found for a rental property) and bridge loans (a service allowing the seller to purchase a home before the revenue from the sale of their previous home is available).

Dosh is a Fintech platform that enables automatic cash backs for consumers. Its business model connects major card providers with online and offline local businesses to develop automatic cash back programs. The company makes money by earning an affiliate commission on each eligible sale from consumers.

E-Trade is a trading platform, allowing investors to trade common and preferred stocks, exchange-traded funds (ETFs), options, bonds, mutual funds, and futures contracts, acquired by Morgan Stanley in 2020 for $13 billion. E-Trade makes money through interest income, order flow, margin interests, options, future and bonds trading, and through other fees and service charges.

Klarna is a financial technology company allowing consumers to shop with a temporary Visa card. Thus it then performs a soft credit check and pays the merchant. Klarna makes money by charging merchants. Klarna also earns a percentage of interchange fees as a commission and for interests earned on customers’ accounts.

Lemonade is an insurance tech company using behavioral economics and artificial intelligence to process claims efficiently. The company leverages technology to streamline onboarding customers while also applying a financialmodel to reduce conflicts of interest with customers (perhaps by donating the variable premiums to charity). The company makes money by selling its core insurance products, and via its tech platform, it tries to enhance its sales.

Monzo is an English neobank offering a mobile app and a prepaid debit card for consumers and businesses. It was one of the first app-based banks to enter the UK market, founded by Gary Dolman, Jason Bates, Jonas Huckestein, Paul Rippon, and Tom Blomfield in 2015. All were employees of Starling Bank, a similar neobank challenging the dominance of established financial institutions in England. The company enjoys many revenue streams: business and consumer subscriptions, interchange and overdraft fees, personal loans, and more.

NerdWallet is an online platform providing tools and tips on all matters related to personal finance. The company gained traction as a simple web application comparing credit cards. NerdWallet makes money via affiliate commissions determined according to the affiliate agreements.

Quadpay was an American fintech company founded by Adam Ezra and Brad Lindenberg in 2017. Ezra and Lindenberg witnessed the rising popularity of buy-now-pay-later service Afterpay in Australia and similar service Klarna in Europe. Quadpay collects a range of fees from both the merchant and the consumer via merchandise fees, convenience fees, late payment, and interchange fees.

Revolut an English fintech company offering banking and investment services to consumers. Founded in 2015 by Nikolay Storonsky and Vlad Yatsenko, the company initially produced a low-rate travel card. Storonsky in particular was an avid traveler who became tired of spending hundreds of pounds on currency exchange and foreign transaction fees. The Revolut app and core banking account are free to use. Instead, money is made through a combination of subscription fees, transaction fees, perks, and ancillary services.

Robinhood is an app that helps to invest in stocks, ETFs, options, and cryptocurrencies, all commission-free. Robinhood earns money by offering: Robinhood Gold, a margin trading service, which starts at $6 a month, earn interests from customer cash and stocks, and rebates from market makers and trading venues.

SoFi is an online lending platform that provides affordable education loans to students, and it expanded into financial services, including loans, credit cards, investment services, and insurance. It makes money primarily via payment processing fees and loan securitization.

Squarespace is a North American hosting and website building company. Founded in 2004 by college student Anthony Casalena as a blog hosting service, it grew to become among the most successful website building companies. The company mostly makes money via its subscription plans. It also makes money via customizations on top of its subscription plans. And in part also as transaction fees for the website where it processes the sales.

Stash is a FinTech platform offering a suite of financial tools for young investors, coupled with personalized investment advice and life insurance. The company primarily makes money via subscriptions, cashback, payment for order flows, and interest for cash sitting on members’ accounts.

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Wealthfront is an automated Fintech investment platform providing investment, retirement, and cashmanagement products to retail investors, mostly making money on the annual 0.25% advisory fee the company charges for assets under management. It also makes money via a line of credits and interests on the cash accounts.

Zelle is a peer-to-peer payment network that indirectly benefits the banks’ consortium that backs it. Zelle also enables users to pay businesses for goods and services, free for users. Merchants pay a 1% fee to Visa or Mastercard, who share it with the bank that issued the card.

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

What is Common characteristics of a neobank?

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

What are the advantages?

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch..

What are the popular neobanks?

Lastly, let’s take a look at some of the most popular neobanks on the market today:

Read Next: Fintech Business Models , IaaS, PaaS, SaaS , Enterprise AI Business Model , Cloud Business Models .

What is Introduction?

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

What is Common characteristics of a neobank?

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

What are the advantages?

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch..

What are the popular neobanks?

Lastly, let’s take a look at some of the most popular neobanks on the market today:

What is Introduction?

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

What is Common characteristics of a neobank?

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

What are the advantages?

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch.. Low Fees: Many Neobanks operate with lower overhead costs compared to traditional banks, allowing them to offer competitive fee structures.

What are the popular neobanks?

Lastly, let’s take a look at some of the most popular neobanks on the market today:

Frequently Asked Questions

What Is A Neobank??

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks. The earliest neobanks emerged from the ashes of the 2008 Global Financial Crisis as consumer confidence in the banking sector plummeted to historically low levels.

What is Introduction?

A neobank is any bank that operates online without a network of physical branches. For this reason, neobanks are also known as online banks, virtual banks, or digital banks.

What is Common characteristics of a neobank?

In fundamental terms, a neobank is a fintech company offering a banking service to tech-savvy consumers who prefer to do their banking in a mobile app.

What are the advantages?

Convenience: Neobanks offer convenient digital banking services that can be accessed anytime, anywhere, using mobile apps or online platforms. Customers can perform various banking tasks, such as account management, fund transfers, and bill payments, without the need to visit a physical branch.. Low Fees: Many Neobanks operate with lower overhead costs compared to traditional banks, allowing them to offer competitive fee structures.

What are the popular neobanks?

Lastly, let’s take a look at some of the most popular neobanks on the market today:

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.