Under the leasing business model, a company purchases a product and then leases it to a customer for a periodic fee. The seller passes the property of the item to the lessor, which is a financier, that enables a buyer (the lessee) to use the item for a given period of time. In the end, the buyer can exercise the option to buy the item at the current market rate. This agreement makes it possible for the seller to dispose of the item, for the financier to make a profit on it, and for the buyer to use it while avoiding total costs of ownership.

Aspect

Explanation

Leasing Business Model

The Leasing Business Model involves a company renting or leasing a product or asset to customers for a specified period in exchange for periodic payments, rather than selling the product outright.

Key Concept

The primary concept is that the company retains ownership of the product while allowing customers to use it for a fee, providing access to the product’s benefits without the need for a large upfront purchase.

Types of Leases

There are various types of leases, including operating leases (short-term, often for equipment) and finance leases (long-term, typically for high-value assets), each with distinct accounting and ownership implications.

Benefits for Customers

Customers benefit from leasing as it reduces the initial financial burden, provides access to the latest technology, offers flexibility to upgrade or change equipment, and may include maintenance and support in the lease agreement.

Revenue Generation

Companies generate revenue through leasing fees, often including interest or finance charges in the case of finance leases. Leasing can result in predictable, recurring income over the lease period.

Asset Management

The leasing company is responsible for asset management, including maintenance, repairs, and upgrades for the leased items, ensuring they remain in good condition and retain their value throughout the lease term.

Industries

The Leasing Business Model is common in various industries, such as automobiles, real estate, construction equipment, technology equipment, and aircraft, among others.

Tax Benefits

Depending on the region and type of lease, there may be tax benefits for both the lessor and lessee, such as depreciation deductions and potential tax credits. These can make leasing financially attractive.

Challenges

Challenges include asset depreciation, the need to manage and maintain a large inventory of leased items, and the potential for economic downturns affecting demand for leasing.

Ownership Options

At the end of a lease term, customers may have options like returning the leased item, purchasing it at fair market value, or entering into a new lease for an upgraded product.

Sustainability

Leasing can contribute to sustainability by allowing customers to access the latest, more energy-efficient products without the need for frequent purchases and disposal of outdated equipment.

Customer Considerations

Customers should carefully consider the total cost of ownership, including lease payments, maintenance costs, and end-of-lease options when evaluating the leasing model.

Companies that utilize the leasing business model sell continuous access to a product or service over an agreed period.

The model normally involves three parties:

The seller

The owner of the product or service that sells ownership of the item to a lessor in exchange for payment.

Note that the seller may or may not retake possession of the item once the contractual agreement has ended.

The buyer (lessee)

The entity that negotiates access to the product or service in exchange for a periodic payment to the lessor.

Once the lease is up, the buyer sometimes has the option of purchasing the item at the current market rate.

The financier (lessor)

A third-party that enters into an agreement with the lessee and provides it with the item for temporary possession.

In essence, the lessor serves as an intermediary or facilitator.

Where does the leasing business model occur?

The leasing business model is most often seen in transactions involving the exchange of expensive physical goods, including:

Commercial and industrial fleet vehicles – including passenger vans, buses, box trucks, tractors, trailers, and delivery vans.

Manufacturing and industrial plant equipment – in industries notorious for expensive item costs, leasing arrangements may be in place for stamping and forming machinery, welders, conveyor systems, and factory infrastructure or floor space.

Restaurant and hospitality equipment – these include exhaust hoods, tables, seating, point-of-sale (POS) systems, and stoves.

Medical and laboratory equipment – such as lasers, X-ray machines, CT scanners, and even surgical tables.

Municipal equipment – many local councils and authorities also lease equipment to reduce costs. Items include police cars, garbage trucks, and street sweepers.

Advantages of the leasing business model

Let’s now take a look at some of the advantages of the leasing business model for both the seller, lessee, and lessor.

Seller

Early revenue – leasing can help the seller meet a need for early revenue, even if some revenue must be shared with the lessee.

Relationship building – since many leasing agreements extend over long periods, the seller has time to build a sustainable and loyal relationship with a buyer.

Lessee

Affordability – the most obvious benefit for a buyer is affordability. Many buyers are not willing to expose themselves to the risk of owning an asset outright while others simply cannot meet the high upfront cost. The leasing business model enables the buyer to pay in smaller monthly installments which can be budgeted for in advance.

Continuous upgrades – businesses that rely on the latest model equipment can easily upgrade when the current lease expires. This means they are never stuck with an obsolete model.

Lessor

Increased sales – lease financing through a third party can help product manufacturers increase their sales. In these circumstances, the lessor is in a stronger position to negotiate a commission from the manufacturer.

Tax benefits – as the owner of the asset, the lessor can claim various tax benefits including depreciation and investment allowance to reduce their liabilities.

Key takeaways:

Under the leasing business model, a company purchases a product and then leases it to a customer for a periodic fee.

Leasing transactions normally involve three parties: the seller, the buyer (lessee), and the financier (lessor). The lessor purchases the product from the buyer and then sells access to the product to the lessee over a set period.

For the seller, the leasing business model gives them access to early revenue and the chance to build a loyal customer base. For the lessee, leasing allows them to avoid the risk and cost of purchasing an item outright. For the lessor, they may be able to negotiate a higher rate of commission with the product manufacturer and reduce their tax liabilities.

Key Highlights

Definition: The leasing business model involves a company purchasing a product and then leasing it to customers for a periodic fee. This arrangement allows the lessee (buyer) to use the item for a specific time frame without owning it outright.

Parties Involved:

Seller: The entity that owns the product and sells its access to the lessor (financier).

Buyer (Lessee): The customer who negotiates access to the product by paying periodic lease fees.

Financier (Lessor): A third-party that enters into an agreement with the lessee and provides temporary possession of the item, essentially acting as an intermediary.

Lease End Options: At the end of the lease term, the lessee often has the option to purchase the item at the current market rate.

Common Industries: The leasing business model is commonly seen in transactions involving expensive physical goods, such as commercial vehicles, industrial equipment, restaurant equipment, medical devices, and more.

Advantages:

Seller: Provides early revenue and an opportunity to build strong customer relationships.

Lessee: Offers affordability through smaller monthly installments, continuous upgrades, and avoids the risks of outright ownership.

Lessor: Can negotiate commission from manufacturers and benefit from tax advantages as the owner of the asset.

Tesla Case Study: leasing model to scale sales

Tesla has its own leasing arm, which is a critical distribution ingredient, to enable the company to scale its sales.

As an electric automaker and builder of sports cars and now trucks, Tesla’s competitors comprise companies like Ford, Mercedes-Benz, Porsche, Lamborghini, Audi, Rivian Lucid Motors, Toyota, and more. At the same time, Tesla is an electric energy production and storage company (SolarCity); it competes with Sunrun, SunPower, and Vivint Solar. And as an autonomous driving company, it competes with companies like Zoox, Waymo, and Baidu with self-driving software.

Indeed, Tesla’s leasing arm generated $1.6 billion in revenues in 2021, but most importantly this enables Tesla to make its products accessible to more people.

Indeed, there are a few key elements to understand why leasing matters in this case:

Make the product accessible: a first element is about distribution. By enabling customers to lease Tesla vehicles, the company can make the car affordable also to people that otherwise wouldn’t be able to afford it.

Leasing coupled with Insurance: Tesla is able to adjust the price of the lease also based on the driving behavior of drivers, thus making it possible for them to get the vehicle at a lower expense, by improving their driving.

Build a new financing arm: when you have a valuable product, it becomes easier to build a service business around that product. The financing arm, which in 2021 generated $1.6 billion in revenues, has the potential to grow many times over, coupled with the scale up of the company’s operations. And this is also a business segment with potentially high margins, that can be also used to further scale the company.

Case Studies

Nissan Motor Acceptance Corporation (Nissan Motor Co., Ltd.):

Nissan Motor Acceptance Corporation provides financing and leasing options for Nissan and INFINITI vehicles, allowing customers to lease and finance their automobiles.

Mercedes-Benz Financial Services (Mercedes-Benz):

Mercedes-Benz Financial Services offers leasing and financing solutions for Mercedes-Benz vehicles, making luxury cars more accessible to consumers.

Penske Truck Leasing (Penske Corporation):

Penske Truck Leasing provides commercial truck leasing and fleet management services, catering to businesses that need transportation solutions.

Enterprise Holdings (Enterprise Rent-A-Car):

Enterprise Holdings operates Enterprise Rent-A-Car, a rental car company that offers short-term vehicle rentals to individuals and businesses.

Hertz Global Holdings (The Hertz Corporation):

Hertz Global Holdings, through its subsidiary The Hertz Corporation, provides car rental and leasing services to travelers and businesses.

Avis Budget Group (Avis and Budget Rent a Car):

Avis Budget Group operates Avis and Budget Rent a Car, offering car rental and leasing options at various locations worldwide.

Volvo Financial Services (Volvo Group):

Volvo Financial Services provides financing and leasing solutions for Volvo trucks, construction equipment, and commercial vehicles.

Komatsu Financial (Komatsu Ltd.):

Komatsu Financial offers equipment financing and leasing options for Komatsu construction and mining equipment.

Ryder System, Inc.:

Ryder System provides commercial fleet management, truck rental, and leasing services to businesses needing transportation solutions.

CIT Group Inc. (CIT Group):

CIT Group offers commercial lending, equipment financing, and leasing services to a wide range of industries.

Sprint (T-Mobile US, Inc.):

Sprint, now part of T-Mobile US, used to provide mobile device leasing and financing options for smartphones and other wireless devices.

Dollar Thrifty Automotive Group (Thrifty Car Rental):

Dollar Thrifty Automotive Group operates Thrifty Car Rental, offering vehicle rental and leasing services at airports and other locations.

XPO Logistics, Inc.:

XPO Logistics provides transportation and logistics solutions, including the leasing of trucks and equipment for businesses.

Rentalcars.com (Booking Holdings Inc.):

Rentalcars.com, part of Booking Holdings, offers online car rental and leasing reservations from various car rental companies.

Maersk Line (A.P. Moller – Maersk Group):

Maersk Line provides container shipping services, including the leasing of shipping containers to facilitate global trade.

Trane Technologies plc (Trane):

Trane Technologies offers heating, ventilation, and air conditioning (HVAC) equipment leasing and financing solutions for commercial buildings.

Ricoh Financial Services (Ricoh Company, Ltd.):

Ricoh Financial Services provides leasing and financing options for Ricoh office equipment, document solutions, and technology services.

Caterpillar Financial Services offers financing and leasing solutions for Caterpillar machinery and equipment used in construction and mining.

Navistar Financial Corporation (Navistar International Corporation):

Navistar Financial Corporation provides financing and leasing options for Navistar’s commercial trucks and buses.

Konica Minolta Business Solutions (Konica Minolta, Inc.):

Konica Minolta Business Solutions offers leasing and financing services for Konica Minolta office imaging equipment, managed print services, and IT solutions.

Related Concepts

Description

When to Apply

Leasing Business Model

The leasing business model involves renting or leasing assets, such as equipment, vehicles, or property, to customers for a specified period in exchange for periodic payments. It enables businesses to access assets without the upfront costs of ownership.

– When offering equipment, vehicle, or real estate leasing services to customers – When seeking to provide flexible financing options to customers who prefer to lease rather than purchase – When aiming to generate recurring revenue streams through lease agreements – When managing asset utilization and lifecycle efficiently

Asset Financing

Leasing provides an alternative financing option for businesses to acquire assets without the need for large upfront capital investments. It allows businesses to access the latest equipment or technology while conserving cash flow and preserving credit lines.

– When acquiring expensive equipment, machinery, or technology for business operations – When looking to conserve capital and avoid tying up funds in asset purchases – When seeking flexible financing solutions to match cash flow and revenue cycles – When planning for equipment upgrades or replacements

Revenue Diversification

Leasing assets allows businesses to diversify their revenue streams beyond traditional product sales. By offering leasing options, businesses can generate recurring revenue from lease payments over the lease term, providing a stable income stream.

– When looking to diversify revenue sources and reduce dependency on product sales – When aiming to increase customer lifetime value by offering additional financing options – When seeking to create predictable and consistent revenue streams through lease agreements – When planning for long-term financial sustainability and growth

Customer Flexibility

Leasing provides customers with flexibility and affordability by offering them access to assets without the commitment of ownership. It allows customers to conserve capital, manage cash flow effectively, and avoid the risks associated with asset ownership.

– When targeting customers who prefer flexibility and affordability over ownership – When serving businesses with fluctuating equipment needs or usage patterns – When addressing customers’ concerns about asset depreciation, maintenance, and disposal – When offering financing solutions tailored to customer preferences and financial constraints

Asset Management

Leasing assets enables businesses to efficiently manage their asset lifecycle, including acquisition, utilization, maintenance, and disposition. It allows businesses to optimize asset usage, minimize downtime, and ensure compliance with regulatory requirements.

– When managing a diverse portfolio of leased assets across multiple customers or locations – When tracking asset usage, performance, and maintenance schedules – When planning for asset upgrades, replacements, or end-of-lease options – When ensuring compliance with leasing agreements, regulatory standards, and industry best practices

Risk Mitigation

Leasing can mitigate risks associated with asset ownership, such as depreciation, obsolescence, and maintenance costs. Lessors often assume responsibility for asset maintenance and repairs, reducing the financial and operational risks for lessees.

– When seeking to transfer risks associated with asset ownership to lessors – When addressing concerns about asset depreciation, technological obsolescence, or regulatory changes – When ensuring business continuity and operational efficiency by minimizing asset-related risks – When evaluating lease agreements to determine risk-sharing arrangements and liability allocations

Market Expansion

Offering leasing options can expand the market reach and customer base for businesses by making products or services more accessible to a broader range of customers. It allows businesses to penetrate new market segments and attract customers who prefer leasing over purchasing.

– When targeting new customer segments or industries with leasing options – When expanding into markets where leasing is a common practice or preferred financing option – When offering leasing as a competitive differentiator to attract customers from competitors – When seeking to capitalize on market trends and customer preferences for leasing solutions

Financial Flexibility

Leasing provides financial flexibility for businesses by offering customizable lease terms, payment schedules, and end-of-lease options. It allows businesses to tailor lease agreements to their specific needs, cash flow requirements, and growth objectives.

– When negotiating lease agreements with customers to accommodate their financial constraints and preferences – When structuring lease terms, payment schedules, and buyout options to align with business objectives – When offering lease financing as part of a comprehensive financial solution or package – When providing personalized financing options to meet customer needs and enhance competitiveness

Regulatory Compliance

Leasing businesses must comply with regulatory requirements governing lease agreements, accounting standards, tax implications, and consumer protection laws. Ensuring compliance with regulations helps mitigate legal and financial risks for lessors and lessees.

– When structuring lease agreements and terms in accordance with accounting standards and regulatory guidelines – When maintaining accurate records, documentation, and disclosures required by leasing regulations – When addressing legal and compliance issues related to lease agreements, tax implications, and consumer rights – When seeking legal counsel or consulting experts to ensure compliance with leasing laws and regulations

An effective business model has to focus on two dimensions: the people dimension and the financial dimension. The people dimension will allow you to build a product or service that is 10X better than existing ones and a solid brand. The financial dimension will help you develop proper distribution channels by identifying the people that are willing to pay for your product or service and make it financially sustainable in the long run.

Business model innovation is about increasing the success of an organization with existing products and technologies by crafting a compelling value proposition able to propel a new business model to scale up customers and create a lasting competitive advantage. And it all starts by mastering the key customers.

Digital and tech business models can be classified according to four levels of transformation into digitally-enabled, digitally-enhanced, tech or platform business models, and business platforms/ecosystems.

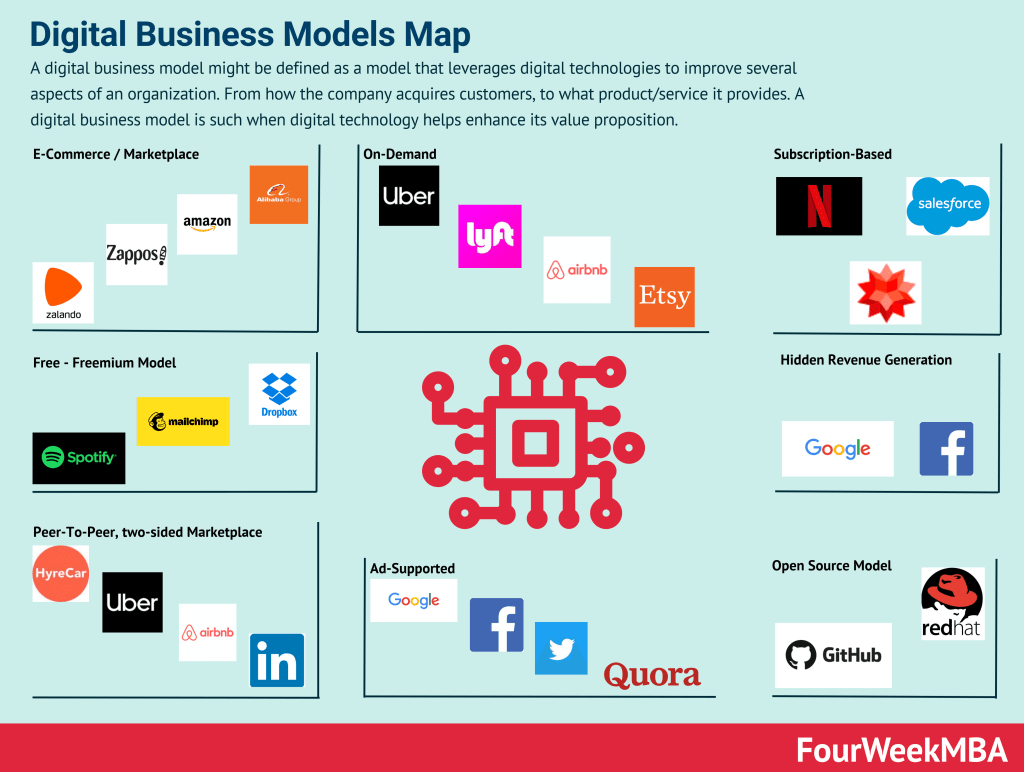

A digital business model might be defined as a model that leverages digital technologies to improve several aspects of an organization. From how the company acquires customers, to what product/service it provides. A digital business model is such when digital technology helps enhance its value proposition.

A tech business model is made of four main components: value model (value propositions, mission, vision), technological model (R&D management), distribution model (sales and marketingorganizational structure), and financial model (revenue modeling, cost structure, profitability and cash generation/management). Those elements coming together can serve as the basis to build a solid tech business model.

A platform business model generates value by enabling interactions between people, groups, and users by leveraging network effects. Platform business models usually comprise two sides: supply and demand. Kicking off the interactions between those two sides is one of the crucial elements for a platform business model success.

A Blockchain Business Model is made of four main components: Value Model (Core Philosophy, Core Value and Value Propositions for the key stakeholders), Blockchain Model (Protocol Rules, Network Shape and Applications Layer/Ecosystem), Distribution Model (the key channels amplifying the protocol and its communities), and the Economic Model (the dynamics through which protocol players make money). Those elements coming together can serve as the basis to build and analyze a solid Blockchain Business Model.

In an asymmetric businessmodel, the organization doesn’t monetize the user directly, but it leverages the data users provide coupled with technology, thus have a key customer pay to sustain the core asset. For example, Google makes money by leveraging users’ data, combined with its algorithms sold to advertisers for visibility.

In an asymmetric businessmodel, the organization doesn’t monetize the user directly, but it leverages the data users provide coupled with technology, thus having a key customer pay to sustain the core asset. For example, Google makes money by leveraging users’ data, combined with its algorithms sold to advertisers for visibility. This is how attention merchants make monetize their business models.

While the term has been coined by Andrew Lampitt, open-core is an evolution of open-source. Where a core part of the software/platform is offered for free, while on top of it are built premium features or add-ons, which get monetized by the corporation who developed the software/platform. An example of the GitLab open core model, where the hosted service is free and open, while the software is closed.

Cloud business models are all built on top of cloud computing, a concept that took over around 2006 when former Google’s CEO Eric Schmit mentioned it. Most cloud-based business models can be classified as IaaS (Infrastructure as a Service), PaaS (Platform as a Service), or SaaS (Software as a Service). While those models are primarily monetized via subscriptions, they are monetized via pay-as-you-go revenue models and hybrid models (subscriptions + pay-as-you-go).

Open source is licensed and usually developed and maintained by a community of independent developers. While the freemium is developed in-house. Thus the freemium give the company that developed it, full control over its distribution. In an open-source model, the for-profit company has to distribute its premium version per its open-source licensing model.

The freemium – unless the whole organization is aligned around it – is a growth strategy rather than a business model. A free service is provided to a majority of users, while a small percentage of those users convert into paying customers through the sales funnel. Free users will help spread the brand through word of mouth.

A freeterprise is a combination of free and enterprise where free professional accounts are driven into the funnel through the free product. As the opportunity is identified the company assigns the free account to a salesperson within the organization (inside sales or fields sales) to convert that into a B2B/enterprise account.

A marketplace is a platform where buyers and sellers interact and transact. The platform acts as a marketplace that will generate revenues in fees from one or all the parties involved in the transaction. Usually, marketplaces can be classified in several ways, like those selling services vs. products or those connecting buyers and sellers at B2B, B2C, or C2C level. And those marketplaces connecting two core players, or more.

B2B, which stands for business-to-business, is a process for selling products or services to other businesses. On the other hand, a B2C sells directly to its consumers.

A B2B2C is a particular kind of business model where a company, rather than accessing the consumer market directly, it does that via another business. Yet the final consumers will recognize the brand or the service provided by the B2B2C. The company offering the service might gain direct access to consumers over time.

Direct-to-consumer (D2C) is a business model where companies sell their products directly to the consumer without the assistance of a third-party wholesaler or retailer. In this way, the company can cut through intermediaries and increase its margins. However, to be successful the direct-to-consumers company needs to build its own distribution, which in the short term can be more expensive. Yet in the long-term creates a competitive advantage.

The C2C business model describes a market environment where one customer purchases from another on a third-party platform that may also handle the transaction. Under the C2C model, both the seller and the buyer are considered consumers. Customer to customer (C2C) is, therefore, a business model where consumers buy and sell directly between themselves. Consumer-to-consumer has become a prevalent business model especially as the web helped disintermediate various industries.

A retail business model follows a direct-to-consumer approach, also called B2C, where the company sells directly to final customers a processed/finished product. This implies a business model that is mostly local-based, it carries higher margins, but also higher costs and distribution risks.

The wholesale model is a selling model where wholesalers sell their products in bulk to a retailer at a discounted price. The retailer then on-sells the products to consumers at a higher price. In the wholesale model, a wholesaler sells products in bulk to retail outlets for onward sale. Occasionally, the wholesaler sells direct to the consumer, with supermarket giant Costco the most obvious example.

The term “crowdsourcing” was first coined by Wired Magazine editor Jeff Howe in a 2006 article titled Rise of Crowdsourcing. Though the practice has existed in some form or another for centuries, it rose to prominence when eCommerce, social media, and smartphone culture began to emerge. Crowdsourcing is the act of obtaining knowledge, goods, services, or opinions from a group of people. These people submit information via social media, smartphone apps, or dedicated crowdsourcing platforms.

In a franchained business model (a short-term chain, long-term franchise) model, the company deliberately launched its operations by keeping tight ownership on the main assets, while those are established, thus choosing a chain model. Once operations are running and established, the company divests its ownership and opts instead for a franchising model.

Businesses employing the brokerage business model make money via brokerage services. This means they are involved with the facilitation, negotiation, or arbitration of a transaction between a buyer and a seller. The brokerage business model involves a business connecting buyers with sellers to collect a commission on the resultant transaction. Therefore, acting as a middleman within a transaction.

Dropshipping is a retail business model where the dropshipper externalizes the manufacturing and logistics and focuses only on distribution and customer acquisition. Therefore, the dropshipper collects final customers’ sales orders, sending them over to third-party suppliers, who ship directly to those customers. In this way, through dropshipping, it is possible to run a business without operational costs and logistics management.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.