Uber and Lyft are both mobility ride-sharing apps. Uber generated $37.28 billion in revenue in 2023, compared with Lyft, which generated $4.4B billion in the same year. A key difference is that while Lyft has primarily stayed in the mobility industry, Uber’s business model today spans various categories beyond mobility, such as delivery (Uber Eats) and freight.

Introduction

Uber and Lyft are the two most popular car-sharing services. Yet, they are both platform business models based on alternative mobility.

As platforms, over time, can use their existing infrastructure — as explored in the economics of AI compute infrastructure — to kick off new types of businesses. Take the case of how Uber started Uber Eats on top of its existing infrastructure.

More than a comparison between Uber and Lyft, this is a set of thoughts and observations that might help understand the dynamics of innovative business models taking over established industries.

Indeed, when building up a company, a conventional strategy is to design a business model and roll it up in the business world. Or to assemble it piece by piece by gathering feedback from the market and iterating on it.

On some occasions though, a business model to be successful requires the transformation of the overall society.

When that happens, business models need to become the builder of ecosystems rather than just companies. For instance, going back to Uber and Lyft, their business models are trying to change an essential piece of our daily lives: transportation.

Mass car ownership

Both Uber and Lyft started more like movements than companies. Indeed, they both had an alternative vision compared to traditional transportation systems.

For instance, Uber ultimate goal is about “making it easier to live without owning a personal car. Achieving that goal ultimately means improving urban life by reducing congestion, pollution and the need for parking spaces.”

At the same time, Lyft started as a movement back in 2012, and its mission is to “improve people’s lives with the world’s best transportation.”

While they’re going in the same directions, those companies share different core values. Where Uber values:

- Expanding access

- Delivering reliability

- Providing choice

- Aligning needs

- Being upfront

Lyft values things like:

- Culture and values

- Brand authenticity

- A multimodal transportation

They might be using a different wordings to deliver the same message. However, from those core values different cultures form, and these cultures are a critical element to the ability of those companies to scale up.

There is a phrase attributed to Peter Drucker, “culture eats strategy for breakfast.” Whether or not he said it, we can’t know for sure. But I think this phrase raises an important point.

Strategy, in general, might sit on the same table of culture. In some occasions, when you’re rolling out an entirely new business model, that demands societal adjustments, then culture does eat strategy and business modeling for breakfast.

In Uber and Lyft case, their beginning as a sort of movement didn’t spring up from a vacuum, but it was a bottom-up movement that came from the drawbacks caused over the years by mass car ownership. Some of those significant drawbacks are:

- Underutilization of vehicles which are parked for most of the time

- The inefficiency of owning cars, which led cities to build massive parking lots in urban dwellings

- The cost of ownership is enormous compared to the benefits of a vehicle, especially within cities

Those movements started from large cities, and it’s not by chance that places like San Francisco, Los Angeles, and New York were the places where those services got first rolled out.

That brings us to the next point.

The formation of new macrotrends

Globalization, digitalization, growing urban populations and the growing precarity of jobs all led to the creation of new trends that helped Uber and Lyft enter the transportation market, to grow quickly. Some of those are:

- A growing number of people prefer to avoid ownership of cars

- The Internet has made it possible to use certain services on-demand

- The need for additional income has created a parallel underutilized “cheap job market”

- People’s growing environmental concerns are making them more aware of their transportation choices

- The inefficiency of public transportation and the taxi industry has in some cities spurred the need for new alternatives

Those macrotrends undoubtedly helped Uber and Lyft to roll out their business models, nonetheless regulation, and protests from existing industries (like the taxi industry). People pushed it for those companies success at a bottom-up level.

That also brings us to another critical point.

When business models become ecosystems-maker

While Uber and Lyft, both have two key partners (drivers and riders) their business model success depends on the ability to deal with local communities.

Thus, the overall implementation of this new transportation business model requires the understanding of complex dynamics that help build ecosystems.

Indeed, while if you’re trying to build a company in an established industry, all you have to do is to create a sustainable business model able to develop a thriving community. When you’re rolling out a business model on a whole new industry, that business model needs to plant the seeds to build a new ecosystem.

Thus, rather than looking internally, it needs to look outside, and while it starts from building a community, it then needs to be able to scale an entire ecosystem!

With new industries, new opportunities emerge

It is interesting to notice how the emergence of players like Uber and Lyft are also allowing the growth of complementary industries. For instance, Hyrecar is a peer-to-peer marketplace where owners of a car can rent their idle vehicles to drivers that want instead make an additional income by driving for Uber or Lyft.

By providing a platform that makes it easy for car owners and drivers to connect, Hyrecar is building a new business from scratch.

Why is this happening? Platforms aren’t an easy game, and Uber and Lyft have come up with clever strategies over the years, mainly to keep drivers going back to the platform.

Indeed, of the two key players (drivers and riders), probably the most important for them, to generate network effect — as explored in the emerging fifth paradigm of scaling — s are drivers. If as a rider I get on the app, but there is no rider around, or my wait time is too long I might well switch to another service or transportation mode altogether.

For that matter, both Uber and Lyft use a dynamic pricing strategy:

Lyft dynamic pricing incentivizes drivers to drive in certain areas

Uber surge pricing to keep drivers going back to the platform to earn extra income

Where Uber and Lyft are successful in attracting a broader number of drivers, companies like Hyrecar benefit from those network effects.

Platforms domination

Uber and Lyft aren’t just companies; they are platforms.

A platform at its core is a place that connects people and groups and makes their interactions as smooth as possible.

As a result of allowing those interactions and platforms to collect fees, which dynamics are not different from that of paying taxes in the long run.

Indeed, take the case of how Uber used its existing platform, to build quickly Uber Eats, now the most valuable part of the Uber Business Model.

That’s also why Uber and Lyft are not in the business of owning cars. They allow connections that spur marketplaces. From those marketplaces, they extract economic value in form of fees.

In the last two decades, the web has allowed many platforms to be formed, Uber and Lyft are no exception.

Transportation as a service

Another radical change that is going through is a broader transition from ownership to possession or use. In short, in many industries, including software (with the rise of SaaS business models) companies are transitioning from offering products or one-time services to ongoing services that can be benefited via a subscription plan.

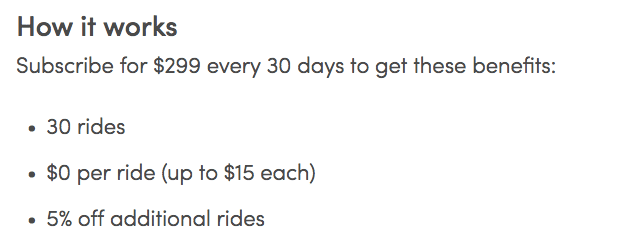

For instance, Lyft introduced subscription fees to access the network of shared bikes and scooters on the platform or to get access to special promotions.

As pointed out on the Lyft blog with a subscription fee you can get an interesting transportation package:

Source: Lyft Blog

Many companies are trying to make the switch from product-centered to customer-centered, which implies a transition from single sales touch points to a continuous stream of services and recommendations for paying subscribers.

Would this trend picks up, then it might become easier also for other businesses like Lyft to implement and improve their subscription offerings.

Key takeaway

New industries can be built on top of older and already existing ones. In the case of mass car ownership, more and more people have opted for a model where they don’t own a car anymore.

This transition is part of a more profound movement, that started almost a decade ago, and that is still ongoing.

When new entrants come in and roll out their business models, it is critical those business models also take into account the fact that a whole ecosystem needs to be built if the business model itself needs to be successful.

For that matter, companies like Uber and Lyft transition from platforms to ecosystem builders. Only when that process is completed, the business model will turn out to be successful, and the bottom line might be finally looking good!

Key Highlights

- Business Model Evolution:

- Both Uber and Lyft are platform business models centered around alternative mobility.

- Over time, Uber expanded beyond mobility, introducing Uber Eats and other services.

- Platform and Movement Origins:

- Uber and Lyft started as movements focused on changing traditional transportation systems.

- Uber’s ultimate goal is to reduce car ownership and urban congestion.

- Lyft’s mission is to improve people’s lives through better transportation options.

- Core Values and Culture:

- Uber values expanding access, reliability, choice, alignment of needs, and transparency.

- Lyft values culture, authenticity, and a multimodal approach to transportation.

- Macrotrends and Industry Entry:

- Globalization, digitalization, urbanization, and job precarity led to trends favoring Uber and Lyft’s entry into transportation.

- Growing environmental concerns, inefficiencies in public transportation, and additional income needs drove adoption.

- Formation of New Ecosystems:

- Uber and Lyft’s success relies on building ecosystems beyond drivers and riders, involving local communities.

- Transforming industries requires creating new ecosystems rather than just companies.

- Complementary Industries:

- Uber and Lyft’s success has led to the emergence of complementary industries like Hyrecar, a platform for car owners to rent their vehicles to rideshare drivers.

- Dynamic Pricing and Network Effects:

- Both platforms use dynamic pricing to keep drivers engaged, creating positive network effects.

- The availability of drivers and riders enhances user experience and platform stickiness.

- Platforms Dominance:

- Uber and Lyft are platforms connecting people and groups for seamless interactions.

- Uber extended its platform to launch Uber Eats, capitalizing on existing infrastructure.

- Transition to Possession and Use:

- Industries are shifting from ownership to possession or use, transitioning to ongoing services via subscription models.

- Lyft introduced subscription fees for accessing shared bikes, scooters, and special promotions.

- Ecosystem Builders:

- Uber and Lyft transitioned from platforms to ecosystem builders as they expand into new industries.

- Building ecosystems becomes crucial for success when introducing transformative business models.

Business Model Explorers

Visual Stories Related To Uber Business Model

In 2022, Uber mobility took 27% of each booking on the platform. At the same time, Uber Eats took 20% of each booking on the delivery platform. The take rate varies according to demand and supply but also market dynamics. In short, in periods of increased competition, the service might charge lower take rates to keep up with it. In 2022, Uber pushed on efficiency, thus raising its take rates, to move toward profitability.

Uber Platform Users

![Uber Business Model vs Lyft Business Model: Key Differences & When to Use Each [2026]](https://i0.wp.com/fourweekmba.com/wp-content/plugins/contextual-related-posts/default.png?resize=150%2C150&ssl=1 "Uber Business Model vs Lyft Business Model: Key Differences & When to Use Each [2026]")