Grab’s value proposition revolves around convenience, accessibility, and an all-in-one super app experience. For consumers, Grab offers a single app that provid

Customer Segments

Grab serves multiple customer segments: 1. Consumers: Individuals looking for ride-hailing, food delivery, digital payments, and other services. 2. Drivers and

Distribution Strategy

Grab’s distributionstrategy is mobile-centric and relies on its super app, available for smartphones. Users can download the Grab app, register, and access a r

Revenue Streams

Grab generates revenue through various streams: 1. Ride-Hailing and Delivery Fees: Grab charges users a fee for ride-hailing and food delivery services. A porti

Marketing Strategy

Grab’s marketingstrategy includes incentives, promotions, partnerships, and digital advertising. The platform offers incentives such as discounts and rewards t

Organization Structure

Grab’s organizational structure consists of specialized teams dedicated to product development, technology, marketing, partnerships, customer support, and finan

Competitive Advantage

Grab’s competitive advantage lies in its super app ecosystem, regional presence, and user-centric approach. The all-in-one super app provides a seamless and con

Grab is a Singaporean food delivery, transportation, and digital services company founded in 2012 by Anthony Tan and Tan Hooi Ling. Tan was inspired to create the platform to revitalize the Malaysian taxi industry.

The Grab app has been compared to WeChat and Alipay for its versatility and diverse product offering. Grab takes a 16-25% commission for every ride it facilitates and charges delivery fees across its food, courier, and home shopping services.

Grab charges premiums to individuals and driver-partners who desire insurance cover. The company also collects a fee every time a consumer purchases from a merchant using GrabPay.

Origin Story

Grab is a Singaporean food delivery, transportation, and digital services company founded in 2012 by Anthony Tan and Tan Hooi Ling.

Tan first had the idea for a taxi-booking mobile app in Southeast Asia while studying at Harvard Business School.

At the time, the Malaysian taxi industry had a poor reputation. Customers were frequently overcharged by drivers and the security of women using taxis was a significant concern.

Grab began as the MyTeksi app in Malaysia after Tan partnered with fellow Harvard graduate Tan Hooi Ling. The app was funded with a $25,000 grant from Harvard Business School and Tan’s personal capital.

Two years later, the company headquarters shifted from Malaysia to Singapore. There, the company invested in a fleet of 100 fully electric taxis, becoming the largest such fleet in Southeast Asia.

As the company continued to expand, Tan maintained a focus on improving the safety of women passengers in particular.

Every Grab driver was interviewed personally before they were recruited, a process Tan admitted was exhaustive but non-negotiable.

Within seven years, Grab’s ride-hailing service could be found in eight countries across Southeast Asia. In 2018, the company momentously acquired rival Uber’s entire presence in the region.

Users can now hail a range of transportation options in addition to taxis, including private vehicles, bicycles, shuttle services, bike taxis, and car-pooling.

The app then followed a similar model to so-called “super apps” such as Alipay and Wechat, offering additional services like hotel booking, ticket purchasing, food delivery, grocery shopping, and on-demand video.

In recent years, Grab has also moved into fintech with a range of insurance and loan options available to small-medium enterprises.

Grab has an extensive revenue generation strategy, owing to its diverse range of products and services.

Without further ado, let’s dive into how the company makes its money.

Ridesharing

For each successful ride Grab facilitates, the company earns a commission of 16-25% of the total fare.

The remainder of the fare is then distributed to the driver.

GrabFood and GrabMart

GrabFood is a food delivery service offered in more than 200 cities across the region. For the privilege of having their food delivered, Grab charges consumers a delivery fee.

This fee depends on the time, area, and merchant processing the order.

Food can also be ordered and delivered from GrabMart, an on-demand delivery service for everyday items such as groceries, packaged food, and healthcare products. For GrabMart customers, there is also a delivery fee.

GrabAds

GrabAds enables business owners to connect with millions of online and offline customers. The advertising service can be used to drive store traffic, boost sales, attract new customers, or promote a product.

Here, the company offers typical website advertising in the form of banners and masthead.

Alternatively, a business can also utilize the Grab taxi fleet for car wrap advertising or branding and sampling purposes. Prices are available on request and are tailored to each advertiser.

GrabExpress

GrabExpress is a courier service available to consumers for any purpose, whether that be sending a birthday gift to a friend or having an urgent document signed and sent back.

There are several GrabExpress delivery options, depending on the size of the package and how urgently it needs to be delivered.

Here, the company charges a base fare plus a fee for every kilometer the courier travels. There is also an additional fee for multiple-stop deliveries and return trips.

GrabInsure

Grab also offers insurance to individuals and rideshare drivers. Currently, the company offers travel insurance and ride cover insurance to individuals, with the latter protecting against late pickups and car accidents.

For rideshare drivers, insurance also provides accident cover, excess cover, and income protection for earnings lost because of prolonged sickness.

Again, prices are tailored to the individual and for drivers, policy rates are determined by their Grab driver-partner rating.

GrabPay

Like many similar platforms, Grab offers payment facilitation services using a digital wallet.

GrabPay can be used for in-store purchases, rides, food deliveries, and funds transfers.

For merchants that want to accept GrabPay as a form of payment, the company charges a so-called Merchant Discount Rate (MDR) for every transaction processed through their unique QR code.

Exact MDR figures are not disclosed. However, most fees are typically between 1.2-2.9%.

Key highlights

Founding and Purpose: Grab is a Singaporean company founded in 2012 by Anthony Tan and Tan Hooi Ling. It started as a taxi-booking app called MyTeksi, aiming to revitalize the Malaysian taxi industry by addressing safety and pricing concerns.

Diverse Product Offering: Grab’s app is known for its versatility and wide range of services, often compared to super apps like WeChat and Alipay. It offers services beyond ride-hailing, including food delivery, courier services, home shopping, digital payments, and more.

Expansion and Acquisitions: Starting in Malaysia, Grab expanded its services across Southeast Asia. It invested in electric taxis and prioritized safety for women passengers. In 2018, Grab acquired Uber’s operations in Southeast Asia, solidifying its presence in the region.

Super App Model: Grab evolved into a super app, offering various services within a single platform, such as ride-hailing, food delivery, grocery shopping, hotel booking, ticket purchasing, and more.

Fintech Ventures: Grab ventured into fintech by offering insurance and loan options to small-medium enterprises, diversifying its revenue streams.

Revenue Generation Strategies:

Ridesharing: Grab earns a commission of 16-25% for every successful ride it facilitates.

GrabFood and GrabMart: Grab charges consumers a delivery fee for its food delivery service (GrabFood) and on-demand delivery service for everyday items (GrabMart).

GrabAds: Businesses can use GrabAds for advertising through banners, mastheads, car wrap advertising, and more.

GrabExpress: Grab’s courier service charges a base fare and per-kilometer fee for deliveries.

GrabInsure: Grab offers insurance to individuals and rideshare drivers, covering various scenarios such as accidents and late pickups.

GrabPay: Grab’s digital wallet facilitates in-store purchases, rides, food deliveries, and funds transfers. Merchants accepting GrabPay pay a Merchant Discount Rate (MDR) for transactions.

Business Model: Grab’s revenue comes from a combination of commissions, fees, and charges across its diverse services. It aims to provide convenience and value to both consumers and businesses.

Business Model Element

Analysis

Implications

Examples

Value Proposition

Grab’s value proposition revolves around convenience, accessibility, and an all-in-one super app experience. For consumers, Grab offers a single app that provides access to a wide range of services, including ride-hailing, food delivery, payments, and more. Users can easily access these services, pay digitally, and enjoy a seamless experience. For drivers and delivery partners, Grab provides income opportunities and flexibility. GrabPay, the digital wallet, offers secure and convenient cashless transactions. Overall, Grab’s value proposition includes: – Convenience: Access multiple services within a single app. – Accessibility: Services are available in multiple Southeast Asian countries. – Safety: Measures are in place for user and driver safety. – Digital Payments: GrabPay enables cashless transactions. – Income Opportunities: Provides income opportunities for drivers and delivery partners. – Accessibility: Offers services to a broad range of users.

Offers an all-in-one super app experience for users. Provides convenience and accessibility to a wide range of services. Ensures safety and security for users and drivers. Promotes cashless transactions through GrabPay. Creates income opportunities for drivers and delivery partners. Serves a diverse user base across Southeast Asia.

– Grab’s value proposition aligns with the growing demand for digital convenience and cashless transactions. – Accessibility across multiple Southeast Asian countries expands its user base. – Income opportunities attract drivers and delivery partners to the platform.

Customer Segments

Grab serves multiple customer segments: 1. Consumers: Individuals looking for ride-hailing, food delivery, digital payments, and other services. 2. Drivers and Delivery Partners: Individuals seeking income opportunities as drivers or delivery partners. 3. Merchants: Businesses looking to partner with Grab for delivery and payment services. 4. Financial Institutions: Banks and financial institutions collaborating with Grab for financial services. Grab tailors its services to meet the unique needs of each segment, offering a user-friendly app for consumers, income opportunities for drivers, business solutions for merchants, and financial products through partnerships.

Serves four primary customer segments: 1. Consumers: Individuals seeking multiple services. 2. Drivers and Delivery Partners: Individuals seeking income opportunities. 3. Merchants: Businesses partnering for delivery and payment solutions. 4. Financial Institutions: Banks and financial institutions collaborating for financial services. Customizes services to cater to each segment’s specific needs. Offers a user-friendly app, income opportunities, business solutions, and financial products.

– Catering to multiple customer segments creates a diverse and interconnected ecosystem. – Tailoring services to each segment enhances user satisfaction and business partnerships. – Collaborations with financial institutions expand Grab’s financial offerings.

Distribution Strategy

Grab’s distribution strategy is mobile-centric and relies on its super app, available for smartphones. Users can download the Grab app, register, and access a range of services from ride-hailing to food delivery. GrabPay, the digital wallet, facilitates cashless transactions and is integrated into the app. Grab also forms partnerships with merchants and businesses to offer their products and services within the app, expanding its reach and services. Additionally, Grab leverages data analytics to personalize user experiences and promotions.

Relies on a mobile-centric distribution strategy through the super app. Users access services, including ride-hailing and food delivery, through the app. Facilitates cashless transactions through GrabPay, integrated into the app. Forms partnerships with merchants to offer products and services within the app. Utilizes data analytics for personalization and targeted promotions. Ensures convenience and accessibility for users.

– Mobile-centric distribution aligns with the increasing use of smartphones for everyday tasks. – Integrating GrabPay into the app promotes cashless transactions. – Partnerships with merchants expand the range of services available within the app.

Revenue Streams

Grab generates revenue through various streams: 1. Ride-Hailing and Delivery Fees: Grab charges users a fee for ride-hailing and food delivery services. A portion of this fee goes to drivers and delivery partners. 2. GrabPay: Grab earns from transaction fees when users make payments using GrabPay. 3. Merchants and Business Partnerships: Grab forms partnerships with businesses and charges them for the use of its platform and delivery services. 4. Advertising and Promotions: Merchants pay for advertising and promotions within the app to reach Grab users. 5. Financial Services: Grab collaborates with financial institutions to offer financial products and earns fees or commissions from these partnerships. 6. Subscription Services: Grab offers subscription-based services for added convenience and benefits, generating recurring revenue.

Relies on revenue streams from: 1. Ride-hailing and delivery fees. 2. GrabPay transaction fees. 3. Partnerships with businesses and merchants. 4. Advertising and promotions. 5. Financial services partnerships. 6. Subscription services. Diversifies income sources through various fees, commissions, and subscriptions.

– Ride-hailing and delivery fees provide a reliable source of revenue tied to service usage. – GrabPay transaction fees promote cashless transactions and revenue generation. – Partnerships with businesses and advertising offer additional revenue streams. – Financial services partnerships expand Grab’s financial offerings and income sources.

Marketing Strategy

Grab’s marketing strategy includes incentives, promotions, partnerships, and digital advertising. The platform offers incentives such as discounts and rewards to attract users and encourage repeat usage. Promotions and discounts are frequently used to boost engagement and attract new users. Grab also forms partnerships with restaurants, retailers, and businesses to expand its service offerings and reach. Digital advertising on social media, search engines, and in-app ads helps promote Grab’s services and special promotions. The app’s user interface and notifications serve as direct marketing channels, keeping users informed about promotions and new features.

Utilizes incentives, promotions, partnerships, and digital advertising for marketing. Offers discounts and rewards to attract and retain users. Uses promotions and discounts to boost engagement and attract new users. Forms partnerships with restaurants, retailers, and businesses to expand service offerings. Utilizes digital advertising on social media, search engines, and in-app ads. Leverages the app’s user interface and notifications for direct marketing. Keeps users informed about promotions and new features.

– Incentives and promotions drive user acquisition and retention. – Partnerships expand service offerings, attracting a wider audience. – Digital advertising enhances brand visibility and promotional efforts.

Organization Structure

Grab’s organizational structure consists of specialized teams dedicated to product development, technology, marketing, partnerships, customer support, and financial services. Product development and technology teams focus on improving the app’s features and functionality. Marketing teams promote Grab’s services and partnerships. Partnership teams collaborate with businesses and merchants. Customer support teams assist users and drivers. Financial services teams work with partner institutions. Grab’s structure supports innovation, user satisfaction, and business growth.

Employs specialized teams for product development, technology, marketing, partnerships, customer support, and financial services. Enhances app features and functionality through product development and technology teams. Promotes services and partnerships through marketing teams. Collaborates with businesses and merchants through partnership teams. Assists users and drivers via customer support teams. Offers financial products through partner institutions. Supports innovation, user satisfaction, and business growth.

– Specialized teams ensure a user-friendly app with evolving features. – Marketing and partnership teams drive user acquisition and brand visibility. – Customer support enhances the user and driver experience. – Financial services expand the platform’s offerings and revenue streams.

Competitive Advantage

Grab’s competitive advantage lies in its super app ecosystem, regional presence, and user-centric approach. The all-in-one super app provides a seamless and convenient experience, attracting and retaining users. Grab’s extensive regional presence in Southeast Asia gives it a strong market position and opportunities for expansion. The platform’s user-centric approach, with safety measures and income opportunities for drivers, fosters trust and loyalty. Grab also diversifies its services, creating multiple revenue streams and a resilient business model.

Derives a competitive advantage from: – All-in-one super app ecosystem. – Extensive regional presence in Southeast Asia. – User-centric approach with safety measures and income opportunities. – Diversified services creating multiple revenue streams. – Strong market position in Southeast Asia. – Opportunities for further expansion.

– The super app ecosystem offers convenience and encourages user retention. – Regional presence establishes a strong market position. – User-centric approach builds trust and loyalty. – Diversified services ensure business resilience and growth.

Grab has fundamentally transformed its business model from a simple ride-hailing platform to an AI-driven super app ecosystem by leveraging machine learning for dynamic pricing and demand prediction. A concrete example is Grab’s implementation of AI-powered surge pricing algorithms that analyze real-time data including weather patterns, traffic conditions, local events, and historical demand to automatically adjust prices and driver allocation. This system not only maximizes revenue during peak periods but also improves supply-demand matching, reducing wait times by up to 30% in major cities like Jakarta and Bangkok. The AI model processes over 2 billion data points daily to predict demand hotspots before they occur, enabling proactive driver positioning. This shift from static pricing to intelligent, predictive pricing has allowed Grab to optimize earnings per ride while expanding into complementary services like food delivery and digital payments, creating a self-reinforcing ecosystem where AI insights from one service enhance others.

Deliveroo is a British online food delivery company founded by Greg Orlowski and Will Shu in 2013. Shu developed the platform in response to a lack of high-quality food delivery in London.

Deliveroo makes money by collecting 25-45% of every order it facilitates. It also charges delivery fees and onboarding fees for restaurants that wish to be featured on the platform.

Deliveroo for Business is a service designed for corporate clients needing to order food in bulk. The company also charges a higher commission to businesses that utilize a network of digital kitchens to process orders.

DoorDash is a platform business model that enables restaurants to set up at-no-cost delivery operations. At the same time, customers get their food at home, and dashers (delivery people) earn some extra money. DoorDash makes money by markup prices through delivery fees, memberships, and advertising for restaurants on the marketplace.

Glovo is a Spanish on-demand courier service that purchases and delivers products ordered through a mobile app. Founded in 2015 by Oscar Pierre and Sacha Michaud as a way to “uberize” local services. Glovo makes money via delivery fees, mini-supermarkets (fulfillment centers that Glovo operates in partnership with grocery store chains), and dark kitchens (enabling restaurants to increase their capacity).

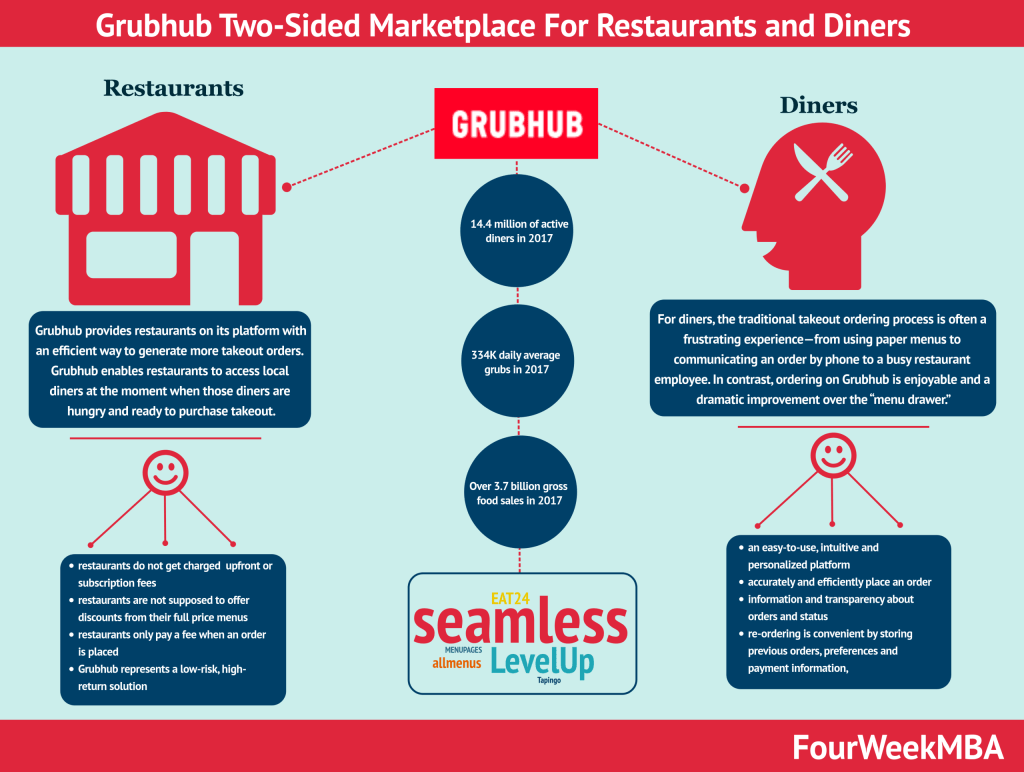

Grubhub is an online and mobile platform for restaurant pick-up and delivery orders. In 2018 the company connected 95,000 takeout restaurants in over 1,700 U.S. cities and London. The Grubhub portfolio of brands like Seamless, LevelUp, Eat24, AllMenus, MenuPages, and Tapingo. The company makes money primarily by charging restaurants a pre-order commission, and it generates revenues when diners place an order on its platform. Also, it charges restaurants that use Grubhub delivery services when diners pay for them.

Lyft is a transportation-as-a-service marketplace allowing riders to find a driver for a ride. Lyft has also expanded with a multimodal platform that gives more options like bike-sharing or electric scooters. Lyft primarily makes money by collecting fees from drivers that complete rides on the platform.

OpenTable is an American online restaurant reservation system founded by Chuck Templeton. During the late 90s, it provided one of the first automated, real-time reservation systems. The company was acquired by Booking Holding back in 2014 for $2.6 billion. Today OpenTable makes money via subscription plans, referral fees, and in-dining with its first restaurant, as an experiment in Miami, Florida.

Postmates is a food delivery service built as a last-mile delivery service platform connecting locals with shops. Postmates makes money by collecting fees (commission, delivery, service, cart, and cancellation fees). It also makes money via its subscription service (called Unlimted – $9.99/month or $99.99 annually), giving free delivery on orders of more than $12.

Uber Eats is a three-sided marketplace connecting a driver, a restaurant owner, and a customer with Uber Eats platform at the center. The three-sided marketplace moves around three players: Restaurants pay commission on the orders to Uber Eats; Customers pay small delivery charges and, at times, cancellation fees; Drivers earn through making reliable deliveries on time.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.

")