Capital adequacy refers to the sufficiency of a financial institution’s capital reserves to absorb potential losses arising from its risk-taking activities and to maintain solvency and financial stability. Adequate capitalization is essential for financial institutions to withstand adverse economic conditions, unexpected losses, and operational risks while fulfilling their role in intermediating funds and supporting economic growth.

Adequate capital levels enhance the resilience of financial institutions and contribute to overall financial stability by absorbing unexpected losses and mitigating systemic risks.

Well-capitalized banks are better equipped to withstand adverse economic shocks, credit defaults, and liquidity pressures without jeopardizing their solvency or triggering contagion effects.

Risk Management:

Capital adequacy serves as a key risk management tool, allowing financial institutions to allocate sufficient resources to cover various types of risks, including credit risk, market risk, operational risk, and liquidity risk.

Capital buffers provide a cushion against potential losses, support risk-taking activities, and help mitigate the probability of financial distress or insolvency.

Creditworthiness and Investor Confidence:

Adequately capitalized institutions signal financialstrength, stability, and creditworthiness to investors, depositors, counterparties, and regulators, enhancing market confidence and reducing funding costs.

Investors and stakeholders are more likely to trust and transact with well-capitalized institutions, leading to lower financing costs, improved access to capital markets, and enhanced liquidity.

Regulatory Compliance:

Regulatory authorities impose capital adequacy requirements on financial institutions to ensure prudential supervision, safeguard depositors’ funds, and maintain the stability of the financial system.

Compliance with regulatory capital standards, such as Basel III, ensures that banks maintain adequate capital ratios relative to their risk exposures and operate within prescribed limits to mitigate systemic risks.

Measurement of Capital Adequacy:

Capital Ratios:

Common measures of capital adequacy include capital ratios, which express a bank’s capital reserves as a percentage of its risk-weighted assets (RWAs).

Key capital ratios include the Tier 1 capital ratio, Tier 2 capital ratio, and Total Capital ratio, which assess the quality and quantity of a bank’s capital base relative to its risk exposures.

Risk-Weighted Assets (RWAs):

RWAs represent a bank’s total assets adjusted for credit, market, and operational risks, reflecting the level of capital required to cover potential losses under different risk categories.

Regulatory capital frameworks assign specific risk weights to different asset classes based on their perceived riskiness, such as corporate loans, mortgages, sovereign debt, derivatives, and off-balance-sheet exposures.

Stress Testing:

Stress testing exercises simulate adverse scenarios and evaluate a bank’s resilience to severe economic downturns, market disruptions, or systemic shocks.

Stress tests assess the impact of credit losses, market volatility, liquidity constraints, and operational failures on a bank’s capital adequacy and solvency under extreme conditions.

Regulation of Capital Adequacy:

Basel Accords:

The Basel Committee on Banking Supervision (BCBS) establishes international standards for bank capital adequacy and risk management through the Basel Accords, including Basel I, Basel II, and Basel III.

Basel III introduced stricter capital requirements, enhanced risk-weighting methodologies, and additional capital buffers to improve the resilience and stability of the global banking system.

Regulatory Capital Requirements:

Regulatory authorities impose minimum capital requirements on banks to ensure adequate capitalization relative to their risk exposures and activities.

Capital adequacy standards stipulate minimum capital ratios, capital components, risk weights, and leverage limits to promote prudential supervision and mitigate systemic risks.

Supervisory Oversight:

Regulatory agencies conduct regular supervisory assessments, examinations, and stress tests to evaluate banks’ compliance with capital adequacy standards, risk management practices, and governance frameworks.

Supervisory reviews monitor capital ratios, assess risk management policies, and address deficiencies through corrective actions, capital injections, or regulatory interventions.

Challenges and Considerations:

Pro-Cyclical Effects:

Capital adequacy requirements may exacerbate pro-cyclical tendencies by reinforcing economic downturns and limiting credit availability during periods of financial stress.

Counter-cyclical capital buffers and macro-prudential policies aim to mitigate pro-cyclical effects and enhance the resilience of the financial system over the economic cycle.

Complexity and Implementation Costs:

Compliance with capital adequacy regulations entails administrative burdens, compliance costs, and resource constraints for banks, particularly smaller institutions with limited scale and capabilities.

Regulatory reforms strive to balance the need for enhanced capital standards with the operational feasibility and cost-effectiveness of implementation across diverse banking sectors.

Global Coordination and Harmonization:

Achieving global consistency and harmonization of capital adequacy standards remains a challenge due to differences in regulatory frameworks, accounting practices, and supervisory approaches across jurisdictions.

Enhanced international cooperation, information sharing, and coordination among regulatory authorities are essential to address cross-border spillovers, regulatory arbitrage, and systemic risks.

Conclusion:

Capital adequacy is a fundamental principle in banking regulation and risk management, ensuring the stability, resilience, and soundness of financial institutions and the broader financial system. Adequate capitalization enables banks to absorb losses, manage risks, and maintain solvency under adverse conditions, promoting market confidence, investor trust, and economic stability. Regulatory authorities play a crucial role in setting and enforcing capital adequacy standards, supervising compliance, and safeguarding financial stability through prudential oversight and risk-based regulation. While capital adequacy regulations enhance the resilience and safety of the banking sector, policymakers must address challenges related to pro-cyclicality, complexity, and global coordination to achieve effective and balanced regulatory outcomes that support sustainable economic growth and financial stability.

The idea of a market economy first came from classical economists, including David Ricardo, Jean-Baptiste Say, and Adam Smith. All three of these economists were advocates for a free market. They argued that the “invisible hand” of market incentives and profit motives were more efficient in guiding economic decisions to prosperity than strict government planning.

Positive economics is concerned with describing and explaining economic phenomena; it is based on facts and empirical evidence. Normative economics, on the other hand, is concerned with making judgments about what “should be” done. It contains value judgments and recommendations about how the economy should be.

When there is an increased price of goods and services over a long period, it is called inflation. In these times, currency shows less potential to buy products and services. Thus, general prices of goods and services increase. Consequently, decreases in the purchasing power of currency is called inflation.

Asymmetric information as a concept has probably existed for thousands of years, but it became mainstream in 2001 after Michael Spence, George Akerlof, and Joseph Stiglitz won the Nobel Prize in Economics for their work on information asymmetry in capital markets. Asymmetric information, otherwise known as information asymmetry, occurs when one party in a business transaction has access to more information than the other party.

Autarky comes from the Greek words autos (self)and arkein (to suffice) and in essence, describes a general state of self-sufficiency. However, the term is most commonly used to describe the economic system of a nation that can operate without support from the economic systems of other nations. Autarky, therefore, is an economic system characterized by self-sufficiency and limited trade with international partners.

Creative destruction was first described by Austrian economist Joseph Schumpeter in 1942, who suggested that capital was never stationary and constantly evolving. To describe this process, Schumpeter defined creative destruction as the “process of industrial mutation that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one.” Therefore, creative destruction is the replacing of long-standing practices or procedures with more innovative, disruptive practices in capitalist markets.

Happiness economics seeks to relate economic decisions to wider measures of individual welfare than traditional measures which focus on income and wealth. Happiness economics, therefore, is the formal study of the relationship between individual satisfaction, employment, and wealth.

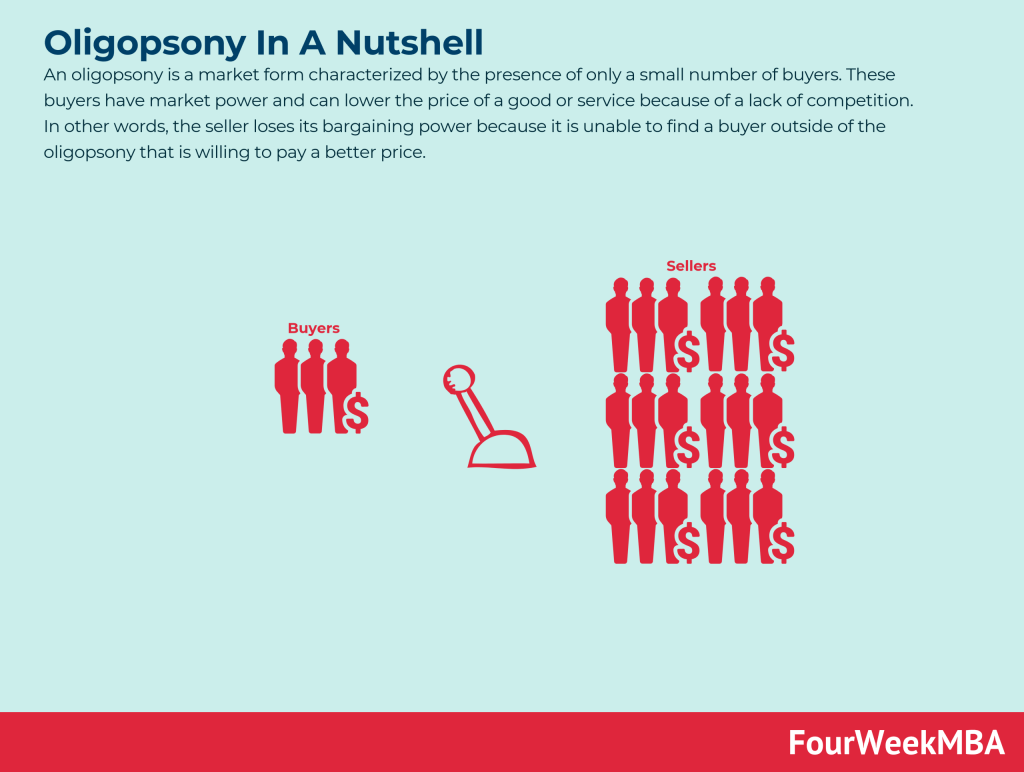

An oligopsony is a market form characterized by the presence of only a small number of buyers. These buyers have market power and can lower the price of a good or service because of a lack of competition. In other words, the seller loses its bargaining power because it is unable to find a buyer outside of the oligopsony that is willing to pay a better price.

The term “animal spirits” is derived from the Latin spiritus animalis, loosely translated as “the breath that awakens the human mind”. As far back as 300 B.C., animal spirits were used to explain psychological phenomena such as hysterias and manias. Animal spirits also appeared in literature where they exemplified qualities such as exuberance, gaiety, and courage. Thus, the term “animal spirits” is used to describe how people arrive at financial decisions during periods of economic stress or uncertainty.

State capitalism is an economic system where business and commercial activity is controlled by the state through state-owned enterprises. In a state capitalist environment, the government is the principal actor. It takes an active role in the formation, regulation, and subsidization of businesses to divert capital to state-appointed bureaucrats. In effect, the government uses capital to further its political ambitions or strengthen its leverage on the international stage.

The boom and bust cycle describes the alternating periods of economic growth and decline common in many capitalist economies. The boom and bust cycle is a phrase used to describe the fluctuations in an economy in which there is persistent expansion and contraction. Expansion is associated with prosperity, while the contraction is associated with either a recession or a depression.

The paradox of thrift was popularised by British economist John Maynard Keynes and is a central component of Keynesian economics. Proponents of Keynesian economics believe the proper response to a recession is more spending, more risk-taking, and less saving. They also believe that spending, otherwise known as consumption, drives economic growth. The paradox of thrift, therefore, is an economic theory arguing that personal savings are a net drag on the economy during a recession.

In simplistic terms, the circular flow model describes the mutually beneficial exchange of money between the two most vital parts of an economy: households, firms and how money moves between them. The circular flow model describes money as it moves through various aspects of society in a cyclical process.

Trade deficits occur when a country’s imports outweigh its exports over a specific period. Experts also refer to this as a negative balance of trade. Most of the time, trade balances are calculated based on a variety of different categories.

A market type is a way a given group of consumers and producers interact, based on the context determined by the readiness of consumers to understand the product, the complexity of the product; how big is the existing market and how much it can potentially expand in the future.

Rational choice theory states that an individual uses rational calculations to make rational choices that are most in line with their personal preferences. Rational choice theory refers to a set of guidelines that explain economic and social behavior. The theory has two underlying assumptions, which are completeness (individuals have access to a set of alternatives among they can equally choose) and transitivity.

The peer-to-peer (P2P) economy is one where buyers and sellers interact directly without the need for an intermediary third party or other business. The peer-to-peer economy is a business model where two individuals buy and sell products and services directly. In a peer-to-peer company, the seller has the ability to create the product or offer the service themselves.

The term “knowledge economy” was first coined in the 1960s by Peter Drucker. The management consultant used the term to describe a shift from traditional economies, where there was a reliance on unskilled labor and primary production, to economies reliant on service industries and jobs requiring more thinking and data analysis. The knowledge economy is a system of consumption and production based on knowledge-intensive activities that contribute to scientific and technical innovation.

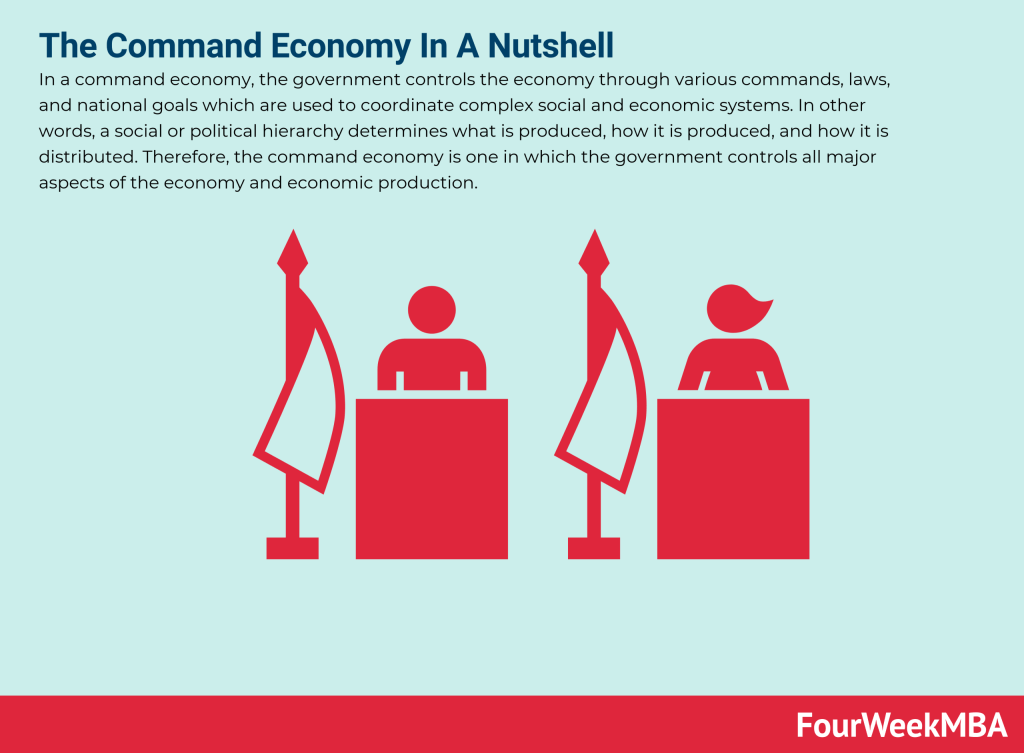

In a command economy, the government controls the economy through various commands, laws, and national goals which are used to coordinate complex social and economic systems. In other words, a social or political hierarchy determines what is produced, how it is produced, and how it is distributed. Therefore, the command economy is one in which the government controls all major aspects of the economy and economic production.

How do you protect your rights as a worker? Who is there to help defend you against unfair and unjust work conditions? Both of these questions have an answer, and it’s a solution that many are familiar with. The answer is a labor union. From construction to teaching, there are labor unions out there for just about any field of work.

The bottom of the pyramid is a term describing the largest and poorest global socio-economic group. Franklin D. Roosevelt first used the bottom of the pyramid (BOP) in a 1932 public address during the Great Depression. Roosevelt noted that – when talking about the ‘forgotten man:’ “these unhappy times call for the building of plans that rest upon the forgotten, the unorganized but the indispensable units of economic power.. that build from the bottom up and not from the top down, that put their faith once more in the forgotten man at the bottom of the economic pyramid.”

Glocalization is a portmanteau of the words “globalization” and “localization.” It is a concept that describes a globally developed and distributed product or service that is also adjusted to be suitable for sale in the local market. With the rise of the digital economy, brands now can go global by building a local footprint.

Market fragmentation is most commonly seen in growing markets, which fragment and break away from the parent market to become self-sustaining markets with different products and services. Market fragmentation is a concept suggesting that all markets are diverse and fragment into distinct customer groups over time.

The L-shaped recovery refers to an economy that declines steeply and then flatlines with weak or no growth. On a graph plotting GDP against time, this precipitous fall combined with a long period of stagnation looks like the letter “L”. The L-shaped recovery is sometimes called an L-shaped recession because the economy does not return to trend line growth. The L-shaped recovery, therefore, is a recession shape used by economists to describe different types of recessions and their subsequent recoveries. In an L-shaped recovery, the economy is characterized by a severe recession with high unemployment and near-zero economic growth.

Comparative advantage was first described by political economist David Ricardo in his book Principles of Political Economy and Taxation. Ricardo used his theory to argue against Great Britain’s protectionist laws which restricted the import of wheat from 1815 to 1846. Comparative advantage occurs when a country can produce a good or service for a lower opportunity cost than another country.

The Easterlin paradox was first described by then professor of economics at the University of Pennsylvania Richard Easterlin. In the 1970s, Easterlin found that despite the American economy experiencing growth over the previous few decades, the average level of happiness seen in American citizens remained the same. He called this the Easterlin paradox, where income and happiness correlate with each other until a certain point is reached after at least ten years or so. After this point, income and happiness levels are not significantly related. The Easterlin paradox states that happiness is positively correlated with income, but only to a certain extent.

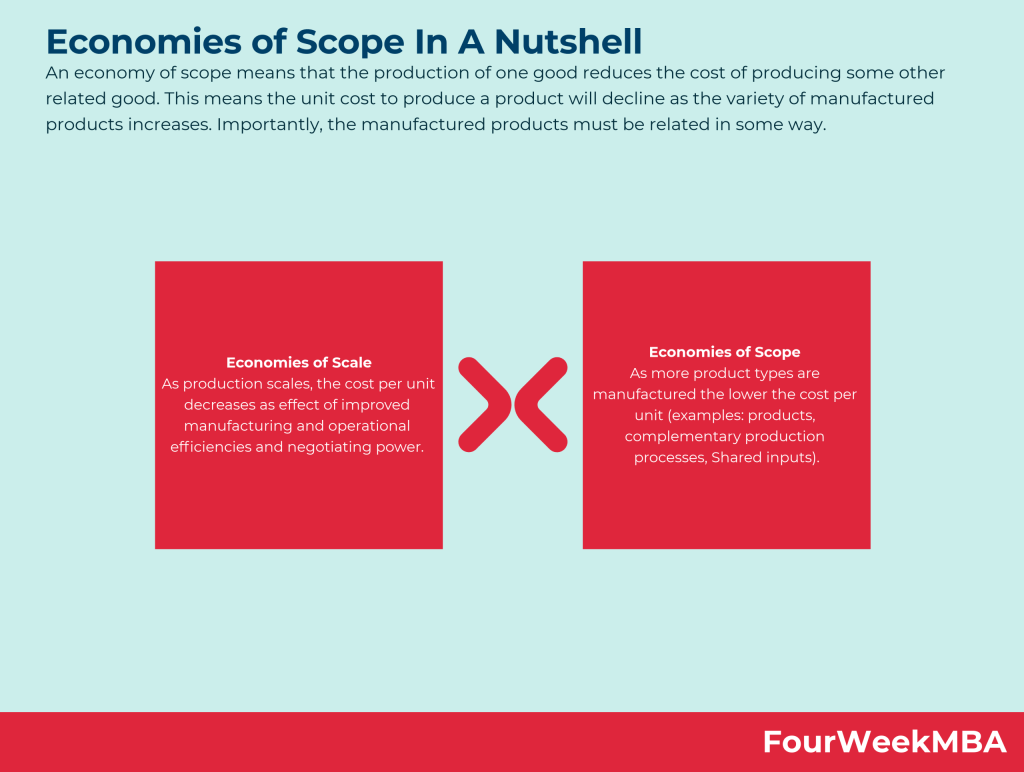

In Economics, Economies of Scale is a theory for which, as companies grow, they gain cost advantages. More precisely, companies manage to benefit from these cost advantages as they grow, due to increased efficiency in production. Thus, as companies scale and increase production, a subsequent decrease in the costs associated with it will help the organizationscale further.

In Economics, a Diseconomy of Scale happens when a company has grown so large that its costs per unit will start to increase. Thus, losing the benefits of scale. That can happen due to several factors arising as a company scales. From coordination issues to management inefficiencies and lack of proper communication flows.

An economy of scope means that the production of one good reduces the cost of producing some other related good. This means the unit cost to produce a product will decline as the variety of manufactured products increases. Importantly, the manufactured products must be related in some way.

Price sensitivity can be explained using the price elasticity of demand, a concept in economics that measures the variation in product demand as the price of the product itself varies. In consumer behavior, price sensitivity describes and measures fluctuations in product demand as the price of that product changes.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.