Currently, the predominant business model for commercial search engines is advertising. The goals of the advertising business model do not always correspond to providing quality search to users.

This is how, in 1998, in a paper entitled “The Anatomy of a Large-Scale Hypertextual Web Search Engine,” Brin and Page, two Ph.D. students, at Stanford University, expressed their frustration, with the current landscape of search.

Just a couple of years before, in 1996, the two students, working on an algorithm – called “BackRub” – leveraging backlinks (web links that looked like citations, where the site linked through a backlink gained authority over others, similarly to the citation mechanism in academia) managed to tame the exponentially growing web of pages.

By 1998, that project had now become a company, called Google.

Before we get to the story of what would later become Google, let’s dive a bit into the context of these years, and how the web (or the commercial Internet) looked like.

And how the various waves of the Internet were shaped by these companies.

The first internet wave and the first walled gardens

In the first wave of the commercial Internet (1994-1999) the first big tech players and tech giants were walled gardens. Those platforms enabled access to proprietary networks (this wasn’t really the Internet, as those were not open protocols). Instead, they were places where users could enjoy a set of controlled and closed online services (emails, news, forums, and later on search).

These first tech giants were companies like AOL, Prodigy, CompuServe, and GEnie. Their business model was straightforward, you would pay for a monthly subscription, and enjoy a few hours of access to their proprietary networks. For each additional hour, users spend on top of the subscription, they would be charged based on consumption.

The first Internet giant: AOL

AOL is a web portal and online service provider founded in 1983, by Marc Seriff, Steve Case, Jim Kimsey, and William von Meister.

AOL was one of the largest media companies of the early Internet, dominating email, internet connectivity, online news, and chat.

At its peak, in 1999, AOL had a market capitalization exceeding $200 billion. As we’ll see this milestone happened as AOL acquired Netscape, in its attempt to fully convert to the new rising wave, of Web 1.0 made of browsing first, then searching the commercial Internet.

Before closing this circle, let me give you some more context about these years.

AOL had mastered the art of attracting and then monetizing dial-up subscribers. By the mid-90s subscription business models, leveraging proprietary networks had started a fierce competition between each other.

Thus, eventually forcing, also AOL to adopt an unlimited subscription plan. Indeed, in October 1996, at the peak of its popularity, AOL announced a $19.95 flat-rate pricing plan for unlimited access to both the Internet and AOL’s private network.

As the legendary Steve Case announced at the time:

You’re seeing a much more aggressive America Online. AOL in one fell swoop is trying to meet the needs of the mainstream and also address the concerns of Wall Street. We really repriced the service to reach out to the heavy users who really want and need unlimited pricing [and] the light users who want the comfort of a relatively low monthly fee.

Yet AOL’s infrastructure — as explored in the economics of AI compute infrastructure — was unprepared for the boom in popularity of broadband internet, and it barely handled that traffic, to the point that the platform started to crash more and more often.

This also triggered a set of class actions against the company, as users got angrier.

This showed that the Internet was becoming a critical utility to those users who subscribed to AOL and that AOL itself had become an important part of those users’ lives.

Yet, the company had to start to spike its subscriptions plans, as the infrastructure was collapsing under the weight of additional traffic.

As the company peaked in 1998, Steve Case announced: “we’re not going to get complacent, but we’ve created a service that’s fun and easy to use. Those factors and the general shift in spending to new media positions AOL as the best brand in the industry.”

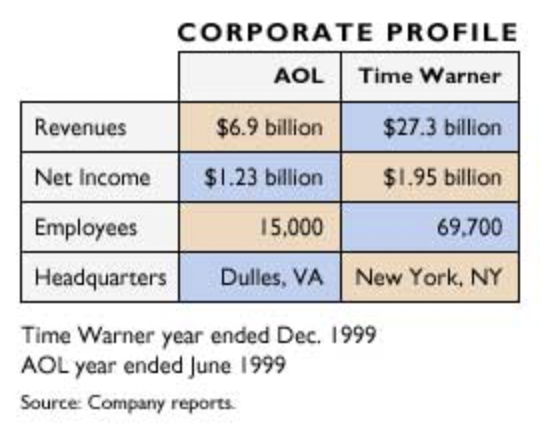

By the year 2000, AOL had generated over $6.8 billion, comprising subscription services ($4.4 billion), advertising/commerce (almost $2 billion), and $500 million from enterprise solutions.

By June 2000, AOL counted 23.2 million members!

Take into account, that in the US, in the year 2000, there were over 120 million Internet users, thus still making AOL the primary avenue to the Internet.

In the same year, AOL sealed the largest merger in United States history – after the Vodafone-Mannesmann merger which reshaped the whole mobile telecom industry – which would play a key role in shaping the Internet, as we know it.

At the time, AOL acquired Time Warner for $111 billion in 2000. The result was a $360 billion multimedia conglomerate comprised of Time Warner’s vast media empire and AOL’s 30 million dial-up Internet subscribers.

As CNN Money highlighted back then, the deal was so big that it worried also Microsoft, which, as the merger was going through, started to engage with the Federal Trade Commission, to restrict the deal, and block it, because it claimed it would restrict competition on the Internet.

It’s critical – as we’ll see – to understand that AOL had been helping regulators in the preparation of the Microsoft antitrust case in the early 2000s, thus Microsoft was looking for revenge.

Yet, the deal went through, but it set a condition:

AOL Time Warner must offer its subscribers the option to sign up to at least one nonaffiliated cable, high-speed Internet service provider via Time Warner’s cable system before AOL itself begins offering such service.

In short, while AOL could merge with Time Warner, it still had to guarantee open access to the Internet, to prevent it to become only a proprietary network, controlled by the newly formed giant.

Unfortunately, the merger occurred just three months before the dot-com bubble burst and the economy fell into a recession.

The relationship between Time Warner and AOL was often acrimonious. This hindered AOL’s ability to make serious inroads into broadband, which was then largely controlled by cable companies. In the years following the merger, the dot-com recession and a lack of broadband integration lead to a serious decline in AOL subscribers.

AOL and Time Warner were two fundamentally different companies. AOL was primarily an online player, where Time Warner had tried but failed to enter the space.

The envisioned synergies between the two giants not only did not materialize. But these two companies never really managed to get along and create a unified culture. This also was a critical lesson in business history.

It doesn’t matter how much firepower you have, sometimes, in order to dominate a new industry, you need to completely change the business playbook. And AOL was soon to learn this lesson, which would cost it its leadership, while new startups, like Google, would take over.

In 2003, AOL Time Warner posted an almost $100 billion loss – at the time the largest in U.S. corporate history. The dot-com bubble had crashed the valuation of the newly formed company.

In the meantime, by 2003, Google had turned into a web giant. When it showed its financials, the whole tech industry was taken aback by its incredible success. Not only was Google profitable, but it was a rocket ship, generating almost a billion in revenue in 2003, with a net profit of over $106 million.

Before we get into the incredible rise of Google, we need to take another step back.

Indeed, you can hardly understand search if you don’t have a grasp of the “browser wars” of the 1990s!

The fall of proprietary networks, the browser wars, and the rise of Web 1.0

As AOL took over the Internet in the first wave of the mid-90s, it also opened up its platform to more and more people, by changing its revenue model. From the subscription and consumption model, AOL had to adapt to the unlimited subscription model where users could enjoy unlimited access to AOL’s proprietary network.

Founded in 1983, as we saw, AOL became the first web Internet giant, using a “walled-garden business strategy.” By early 2000, this strategy had become obsolete, since players like Google wrecked these walls off!

On paper, the merger of AOL and Time Warner formed a large and powerful company with the right mix of assets but AOL had already lost most of its value by the early 2000s.

With this new model, the AOL users base grew even further. But it also showed some of its weaknesses, as the platform became unstable, with a wide number of new members.

In this time period, the Internet also grew exponentially, favoring the birth of a few tech players. In this period, something very counterintuitive happened. Search, which seemed a feature to offer on top of the proprietary networks, became a killer commercial application!

How did search become a commercial killer application? The browser market had laid the foundation for the search market to thrive.

When Microsoft spent billions to bring TV online – the complete failure of the Information Superhighway

Grasping how new industries will evolve is one of the most difficult aspects of high-tech business. And even the smartest people that dominated an industry, can hardly imagine what the future will look like.

This is the reality of the business world. Indeed, back in the mid-90s, when the commercial Internet was finally taking over, most luminaries, gurus, and tech experts projected it as a sort of Information Superhigly (similarly to how today we talk about the Metaverse, and how Mark Zuckerberg’s vision for it might turn to be completely off).

As you can see, the vision at the time, was about an “interactive entertainment center.”

While, by 1995, Microsoft had tried to rewrite business history, as if Bill Gates and his company had grasped in full the Internet phenomenon. In reality, things looked quite different!

As explained by Jim Clark (co-founder of Netscape) in his book “Netscape Time: The Making of the Billion-Dollar Start-Up That Took on Microsoft,“ in 1994, Netscape was launching the browser which would conquer the whole browser market share, thus, becoming, for a short period of time, the Internet!

In the same year, Microsoft was still trying to figure things out. Microsoft, a native player of the PC era, had risen during the 1970s when Intel had created a whole new industry. Thanks to Intel’s family of chips, with the development of the 8080 – led by Federico Faggin – going forward the computer industry was born.

As we saw, the turning point for Microsoft came when, IBM, in1980, was about to launch its IBM Personal Computer. The IBM Personal Computer, contrary to what IBM had done in its whole history, followed an open architecture.

Microsoft on the other hand could license that same operating system to other PC makers, beyond IBM. The microcomputer space, which in the late 1970s was dominated by Tandy, Commodore, and Apple, was taken by surprise as the IBM Personal Computer became a huge success.

Yet, by the early 1990s, IBM lost its leadership and didn’t manage to capture the value of the PC market.

On the other hand, Microsoft became the de facto operating system of the PC industry and within a decade the company became a tech giant. In 1982, Microsoft recorded over $24 million in revenues, in 1985 over $140 million, and by1990 Microsoft had passed a billion dollars in revenue, the first tech company to do so, and becoming the de facto operating system of the PC market.

Where IBM had created the PC standard in the early 1980s, Microsoft surfed it for decades!

Where IBM had lost its leadership, the PC had become a standard that would last for decades, spurring a market that gave rise to new players, competing on price. The hardware had been commoditized, where software, in the form of the operating system first, then applications would be monetized at a premium.

Microsoft followed a platform strategy, were on top of the operating system, it added applications (the first launch of Microsoft Office 1.0 happened in November 1990 and it comprised three applications: Word, Excel, and PowerPoint). Over the years Microsoft bundled everything up, creating de facto the dominant operating system and PC applications provider in the world.

IBM’s mistake would become one of the most studied in the history of high-tech business. As David Bradley, one of the teams of 12 who produced the PC at IBM highlighted:

At the time, we didn’t think it was going to be a revolutionary change, we knew we were working on an exciting project and we certainly hoped it was going to be successful, but we never imagined it was going to take over the world the way it did.

In short, IBM had grasped the importance of the project, but it missed how revolutionary it would be. And that is fine because, in foresight, it’s hard to determine which projects will become new industries.

However, IBM, which at the time, was still a big corporation (they called it “Big Blue“) had first approached a young Bill Gates, in July of 1980 (he was 24 at the time), to develop an operating system, to what became the IBM Personal Computer.

Why did they do it? First, IBM was in a rush. In fact, back then, typical product cycles lasted four years. Instead, IBM wanted to bring the PC to market, as quickly as possible. In addition, IBM was playing a different game. For IBM at the time, it wasn’t about the software, it was about the hardware. Indeed, back then, the software industry didn’t exist as the software was treated as a commodity to be given for free on top of the hardware.

It would be Microsoft that successfully commercialized software. This mindset and philosophy would stick in Microsoft’s culture for decades (the matra for Microsoft under Bill Gates was “we are a software company”), so much so, that when Microsoft tried to manufacture an alternative to the iPhone (its Windows Phone) in the 2010s, it failed miserably.

While on the one hand, IBM had a team of 12 technical people working on the project and a legal and procurement team. Bill Gates and Paul Allen were mostly doing things on their own.

As Bill Gates highlighted, remembering those days, “we had to be very clever, we actually did not get a royalty from IBM but we kept the rights so we were getting royalties from other people.”

By 1993, IBM shocked the business world by reporting quarterly losses of $8bn, primarily caused by increased competition and a changing market. IBM had created a whole new industry, and yet it had failed miserably in dominating, and profiting from it. Microsoft, on the other hand, had become the scariest tech giant of the 1990s.

Also, other players like Apple, which had dominated the computer industry in the late 1970s (though computers were still for niches), refused to license its operating system to others, thus making Microsoft the uncontested PC standard for decades!

Anyone, trying to enter the software space, was a threat to Microsoft, and therefore, was to be killed as quickly as possible, as any potential new sub-industry that would be created in software, which Bill Gates could not control, needed to be suppressed, or taken over by Microsoft.

And in 1994-95, the Internet was the industry that Microsoft needed to dominate if it wanted to keep its dominance, in the long run!

The interesting part was, that some of these Internet competitors, would use Microsoft’s platform strategy, to take over this new market.

#The commercial killer application of the early Internet: Browsing

Accessing the web in the early 1990s wasn’t an easy fit. If it wasn’t for proprietary networks, like AOL, accessing the Internet in the first place was very very hard.

Mosaic, the first web browser, changed that! For the first time, with a very simple and straightforward setup, users could access the Internet. The browser had been developed by a smart group of very young developers, at NCSA. NCSA or the National Center for Supercomputing Applications was a research project unit, set up at the University of Illinois Urbana-Champaign.

As the story goes, in 1992, Joseph Hardin and Dave Thompson, who worked at the NCSA, learned about Tim Berners-Lee’s work at CERN. In the fall of 1990, Tim Berners-Lee had developed the first browser on a NeXT machine (the company Steve Jobs had created after being ousted from Apple), together with an editor to create hypertext documents.

Text-based browsers started to spring up and by 1992, Joseph Hardin and Dave Thompson downloaded the ViolaWWW browser, which had some extended functionalities compared to the first browsers.

Two students at the University of Illinois Urbana-Champaign, Marc Andreessen and Eric Bina started to work on a new browser, for X-Windows on Unix computers, releasing the first version in 1993. This browser was called Mosaic, and it was the first browser to allow images embedded in the text, thus making for the first time, the Internet, way more interactive.

Yet, by August 1994, rather than enabling the development team to take over the project and commercialize it (as Stanford had been doing for decades) NCSA took over the Mosaic project, and it assigned its commercial rights to Spyglass, a corporation that was formed to profit from the Mosaic browser (in 1995 to kick off the launch of Internet Explorer and to kill Netscape dominance, Microsoft licensed Spyglass’ Mosaic technology).

In this context, in early 1994, Jim Clark, an entrepreneur, who had left his previous company, called Silicon Graphics, was looking to create his next big thing, and he was also looking for revenge, as he, the founder of Silicon Graphics had become a marginal player within the company, and barely managed to make a tiny fortune, compared to the multi-billion dollar success he had built.

Jim Clark also looked at the Internet as the potential new business frontier. Yet, he, like Bill Gates, initially thought about bringing TV online. Little did he know, that shortly, he would have met Marc Andreessen, the young kid behind the development of Mosaic.

At the same time, Microsoft and its founder, Bill Gates, understood the importance of the internet. Back in January 1996, Bill Gates wrote one of the most quoted pieces, still nowadays “Content is King:”

One of the exciting things about the Internet is that anyone with a PC and a modem can publish whatever content they can create. In a sense, the Internet is the multimedia equivalent of the photocopier. It allows material to be duplicated at low cost, no matter the size of the audience.

The main problem of Gates’ vision at the time was the fact that Microsoft had tried to linearly apply TV to the Internet, as if, the two technologies would follow the same pattern of development.

Over the years, streaming took over the Internet (see Netflix), but in reality, it evolved in completely different ways, and formats (see Netflix binge-watching).

Yet, while Microsoft realized the potential of the Internet early on, it had executed badly on it. And by 1996, it was clear, that “browsing” was the killer commercial application of the Internet and it had a new king.

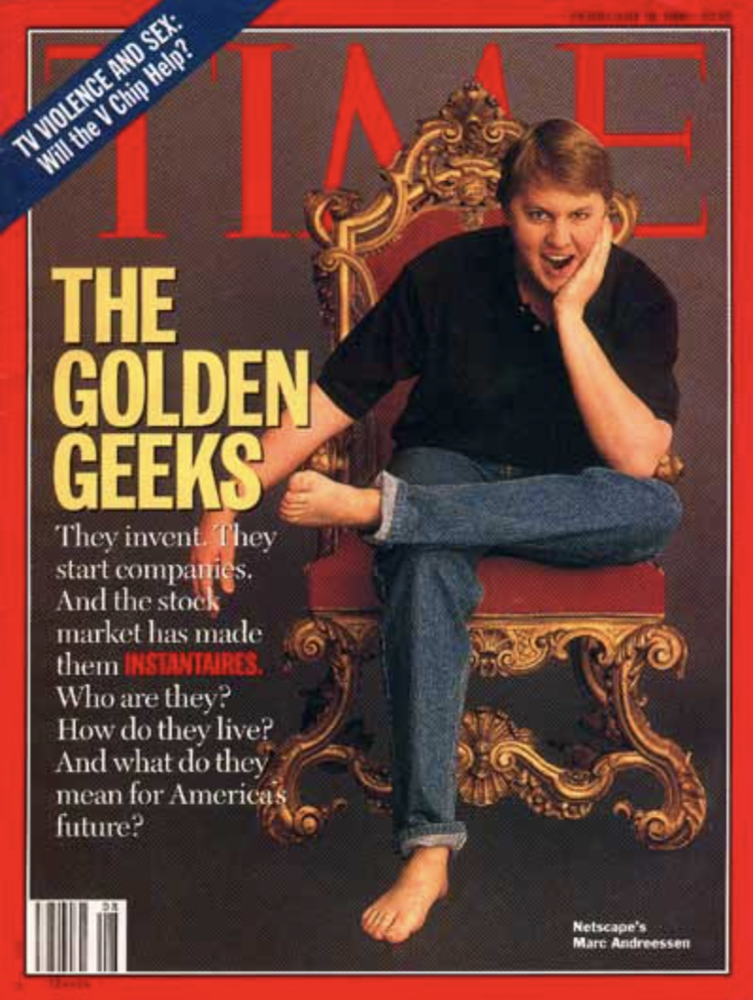

Time Magazine Archive

A featured in Time Magazine in February 1996, a shoeless Marc Andreessen (at the time 24) was featured as the new king of the Internet, an image that Bill Gates didn’t like at all.

The Browser wars

A young Marc Andreessen, co-founder of Netscape, together with Jim Clark, after months of tinkering, had come to the conclusion that the next big thing would be a “Mosaic killer.”

As the story went, back in 1994, as Clark had left Silicon Graphics, he had met, through a common friend, Marc Andreessen, which Clark recognized right on, as a person worth betting on.

Initially, the two brainstormed ideas about potential ventures to start. But suddenly things became clear. They could develop a Mosaic killer. In fact, the initial developers’ team (of which Andreessen was part) was now working on other projects (Andreessen had moved to California) as NCSA took credit for the development of Mosaic.

Andreessen, together with Clark, convinced the team of developers that had worked on Mosaic, to develop from scratch, a Mosaic killer. This would later become Netscape. The most successful Internet browser.

Netscape was a further improvement on Mosaic’s capabilities. For one thing, Marc Andreessen was a software guy by inclination, and he knew that on the Internet, fast development cycles were the rule. Things didn’t need to be perfect, as new software releases could fix bugs or things that didn’t work, while quickly gathering users’ feedback, and making the product way better, not in the matters of months, but weeks.

This was the new paradigm of the software industry, as the Internet playbook took over. While the first version of Netscape was slightly better than Mosaic, in its later releases, it improved many times over.

By 1997, the browser industry had become a pro game, where Netscape and Microsoft had brought large development teams together. In January 1997, NCSA stopped developing Mosaic.

On the other hand, in 1995 Netscape IPOed, creating the first multi-billion dollar Internet startup. After only sixteen months since the company’s inception. Netscape showed a skyrocketing revenue path, even though its losses kept mounting, and things didn’t look better, as Microsoft went all in!

Clark’s reasoning was that once Netscape had become the market leader, they could go on and monetize that leadership, in the long run, through enterprise deals, similarly to how Microsoft had done, thus creating a strong distribution advantage, that would last.

While Clark’s strategy proved to be correct, as Netscape ramped up its enterprise deals, it also showed Microsoft that they needed to act fast!

And by 1995, Microsoft finally launched its browser: Internet Explorer.

To be quick, and copy what had already worked for Netscape (a standard playbook of Bill Gates, which resembles a lot of the playbook of Mark Zuckerberg in the last decade), Microsoft had licensed the code of Internet Explorer from NCSA.

In short, the codebase Microsoft used to kick off its browser, Internet Explorer, was that of Mosaic, the same browser, that a few years before, Andressen and the core development team, had built at NCSA!

One of the famous quotes from Marc Andreessen was to “reduce Windows to a set of poorly debugged device drivers.”

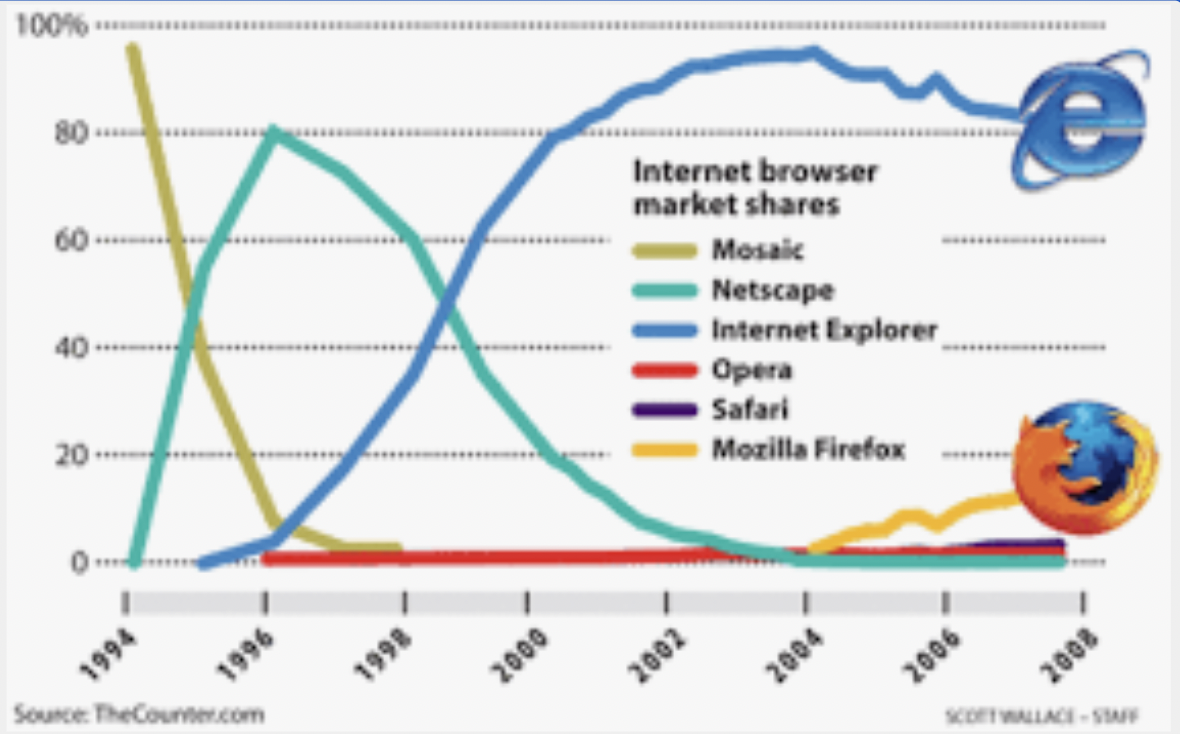

That Netscape’s threat further created a sense of urgency for Microsoft’s top leadership, who started to invest massively in its browser. By 1995, Netscape had the most successful browser on the market and had developed it by bringing together the original team of Mosaic. Netscape truly became a Mosaic killer. From over 90% browser market shares of Mosaic, in 1994, by 1995-6 the situation had turned upside down.

Netscape had reached 80% of the market share, where Mosaic adoption had stalled (Netscape took a growing pie of the exponentially growing Internet users’ base). Netscape did that through fast releases and built-in network effect — as explored in the emerging fifth paradigm of scaling — s.

By 1996-98, Internet Explorer, thanks to the incredible distribution strength of Microsoft, was stealing market shares from Netscape, thus stealing its market leader position.

Indeed, Microsoft was simply bundling its Internet Explorer within its Office Package, thus making it the default choice for users to browse the Internet. Nothing new to Microsoft, which had used the “bundling strategy” for years now.

Yet things looked different in the late 1990s. Microsoft was now the undisputed dominant player in the PC industry, and it was trying to stiffen the competition through distribution in the newly formed Internet industry.

The Microsoft bundling strategy, would, later on, cost the company a famous antitrust case, in which, Bill Gates would be called, in 1998, for hours of deposition, that drained Gates, and might have determined his decision to step down as company’s CEO in 2000.

To be sure, we don’t know what really happened backstage in that antitrust case. And my assumption is that Gates was implicitly threatened to leave the reins of Microsoft if he wanted to avoid the whole company’s breakdown (this is pure speculation on my side).

This was the business context, in the late 1990s, when Google entered the picture.

If browsers wrecked down the walls of the proprietary networks, search engines completely shattered them

As the number of sites on the Internet grew exponentially (by the year 2000 more than 360 million users had joined it), this opened up the need for a tool that enabled one to surf the web to find the most relevant web pages. In parallel to the development of proprietary networks, like AOL, other tools had turned out to be congenial to the Internet.

The first was the browser, with a player like Mosaic, which is a short time span, became very popular.

Yet, as we saw, by 1994, a group of young people that had also worked at Mosaic (among which venture capitalist Marc Andreessen, founder of a16z), also built a browser called Netscape, which by 1995 became the market leader.

Netscape drew the attention of Microsoft’s Bill Gates, which understood how browsers could become the gatekeepers of the Internet. This spurred a war between Microsoft and Netscape, which culminated in Microsoft’s release of Internet Explorer, bundled in its Microsoft Office products.

Thus, Microsoft leveraged its position in the market, to quickly gain market shares, against Netscape. This drew the attention of the regulators who called Microsoft for abusing its dominating position. This led to the parallel development of another commercial killer application: search.

As the Browser wars went on, search became the most important application of the Internet, enabling users to surface the growing numbers of pages on the Web, which was growing at an untamable pace.

Search, therefore, was essential. However, the first search engines, while useful, they were still too much focused on paid placements, and also much easier to game, by webmasters who could easily have their pages show up as relevant, even if not. This paved the way for new players. One epitome of that was GoTo.com, created by the legendary Bill Gross. GoTo.com not only mixed paid results as if they were organic results.

It enabled everyone to bid and compete on its advertising platform. Thus, making the paid search a primary feature. While this model, called CPC was revolutionary, it was also skewed substantially toward paid vs organic results. In that period, toward the end of the 1990s, another player had developed a search engine able to index, and rank the growing mole of web pages.

This was first called Backrub, out of a P.h.d. project at Stanford. And later it was called Google! Google picked up quickly, becoming de facto the most popular search engine at the time. Its ability stood in enabling websites to rank organically without having to pay.

This opened up an industry of practitioners, called SEO (search engine optimization experts) which tried to understand the growing intricacies of search, to make their content distributed across the web. In fact, ranking a site organically had become way more intricate, through PageRank, than it was before, and SEO over the years would turn into a multi-billion dollar industry.

Initially, Google’s founders were quite skeptical of the advertising model for search engines, as they thought this would be intrinsically biased toward paid ads, thus not giving relevant results. Yet, over time they set to change that. They, therefore, started to build an advertising machine, able to also rank paid results based on various factors. Thus, Google borrowed from the GoTo.com CPC model and improved on it. This formula turned out to be extremely powerful.

Google’s deal that made it the tech giant we know today

While Google’s user base was scaling quickly in its early years. Its advertising machine pieces were assembled later on (between 2001-and 2004). Thus, in the early years, Google had to rely on business development deals to further scale up, strengthen its position, and become the market leader.

In the early days, Google’s destiny was all but determined. Indeed, in the early years (1998-2000) the company was not profitable, recording only $220K in revenue in 1999, and over $6 million in losses in the same year.

In 1999, Brin and Page were still thinking to go back to their PhDs at Stanford. Indeed, they approached various competing search engines and platforms, among which Excite, trying to sell Google for $1 million!

Yet, apparently, the Excite executive team eventually didn’t go for it, as the basic premise of Google was to invite users to click on the blue links the tool offered as search results, thus inviting users to leave their search page, and navigate the web.

While this is given for granted today, back then, most search engines were making money by keeping users on their search pages (more similar to what Google has evolved into today), thus, Google posed a threat to their business model.

The same deal was rejected by other players like AltaVista and Yahoo.

In 2000, Google had become very popular, yet it still recorded over $14 million in losses, on a $19 million turnover. Yet Google had been backed by Sequoia Capital, led by John Doerr. Indeed, in 1999 Google had received $25 million in equity funding, from Sequoia Capital and Kleiner Perkins.

As Larry Page announced at the time:

We are delighted to have venture capitalists of this caliber help us build the company, we plan to aggressively grow the company and the technology so we can continue to provide the best search experience on the web.

At the time, PageRank solved an equation of 500 million variables and two billion terms to serve proper search results. The market was still small (one hundred million web searches per day compared to the over eight billion web searches.) that today go through Google).

Venture capitalist, John Doerr explained in his book, “Measure What Matters” how in 1999, he had placed a bet on Google of $11.8 million, for 12% of the company.

While Google was not a first-mover (the search engine at the time was the 18th to enter the market, as Doerr explained), two months later, in the new Google’s offices Larry Page was lecturing Doerr on the poor quality of results of the existing search engines, and how Google would improve, at least of 10x, compared to existing players.

As a venture capitalist, Doerr’s main job was to guess the potential market size of a new industry (this is the obsession of venture capitalists).

And as the story goes, Doerr posed the question to Larry Page:

How big do you think this could be?

Larry Page responded:

Ten billion dollars.

This seemed a crazy market cap to Doerr, who in his mind, had considered a potential market size of Google of one billion dollars maximum.

So Doerr asked:

You mean market cap, right?”

And Page swiftly replied,

No, I don’t mean market cap, I mean revenues.

That seemed crazy enough to Doerr, as with ten billion in revenues, Google would be worth at least a hundred billion in market cap, which was the size of Microsoft, IBM, or Intel, at the time.

Six years later, to that conversation, by 2005, Google had reached a hundred billion market cap. By 2021, the Google advertising machine would generate twice that, in revenues alone, making Google (now called Alphabet) a 1.8 trillion dollar company!

Among the most important deals Google sealed in the early years, there was the deal with AOL. Indeed, AOL saw search as a feature within its proprietary network, thus featuring a search engine that enabled users to surf the web.

Initially, GoTo.com (later called Overture) had a deal with AOL to be featured as the main search engine. Yet as this contract expired by the late 90s, Google jumped on it, managing to get the deal with AOL, in place of Overture! This deal was a very important one, which put Google on a further growth trajectory.

Over the years and going into the early 2000s, proprietary networks had become less and less relevant, as more Internet/Web players had spurred up. From e-commerce to search, platforms like AOL had lost traction. In that scenario, Google became the new King in town.

From then on Google became the new dominant player on the Internet. From wrecking the walls of closed proprietary networks. Over the years (the 2010s – present) Google, then become Alphabet, turned into a sort of Walled Garden itself.Being a first-mover is no more the trick?

Technologies can give an important advantage in the very short term. However, those advantages can be lost pretty easily, if a technology is not leveraged fast. Yet implementing new, unproven technology is also risky, initially very expensive, and often requires the ability to develop a whole new market.

To make things worse, even when this new market has been developed, that doesn’t give you a long-term competitive advantage. In fact, new players that come in can do the same, by simply copying part of the strategy that turned out to be successful.

In short, the first player laid the foundation, for the latecomers to leverage the existing technology, and by improving on it to gain an advantage. But if being first is not giving a long-term advantage, what’s the key ingredient there?

The value of network effects

Many tech companies, from the rise of Microsoft going forward, understood the value of a platform strategy. A platform strategy consists in creating value for users by enabling an entrepreneurial ecosystem on top of it.

The essence of network effects stands in the fact that the service becomes exponentially more valuable for each additional user as more users join in. Of course, building network effects isn’t easy either. As many platforms like Uber and Airbnb figured out at the beginning when they needed to understand how to kick off these networks’ effects.

Thus, when it comes to creating a lasting competitive advantage in this digital landscape, even if you are a first-mover you got to think in terms of network effects.

The first-scaler advantage matters only if you can dominate a market in the long-term

When Netscape built the most valuable commercial browser, back in the mid-90s, the company gave up profits, to grow as quickly as possible. The bet was if Netscape grew large enough to have the most shares of the browsers market it could eventually enjoy also wide profit margins in the long term.

Yet, Netscape awoke Microsoft too early. And while Microsoft did leverage its dominating position to crush Netscape, it also managed to overtime destroy its market leadership. Indeed, while Netscape became a multi-billion dollar success, it never turned a profit, and it eventually sold to AOL, as the pressure from Microsoft was becoming unsustainable.

Thus, even when you do scale, and you do it first, you still need to make sure to stably control that market. Otherwise, like in the case of Netscape vs. Microsoft you might be taken over. Of course, in this particular case, Netscape was crashed by a tech monopoly that took advantage of its dominating position. And Microsoft would pay that many times over.

In fact, while the company survived the subsequent waves of the Internet, it was substantially slowed down by the antitrust case, which for years, would be a threat to Microsoft. Today, under the change in leadership, and under the direction of Satya Nadella, Microsoft has also become an over 2 trillion-dollar company.

Changing business playbooks

When browsing took over the early Internet, that was quite unexpected for many. Also, very smart people, like Bill Gates had envisioned a more linear evolution of the Internet, almost as if that was supposed to bring TV online. While this vision would be in part realized through the 2010s (see Netflix) in reality, it also shows that the model of entertainment on the Internet evolved in a whole different way than TV.

The same applied to search. When Google took over, existing giants like AOL, who had successfully dominated in the previous decade, were taken aback by the success of the latecomers in the Internet revolution.

First, players like AOL thought that search was not a commercial killer application, but rather a feature to be added on top of their services. Second, they didn’t necessarily envision, initially, how search engines would change the whole Internet playbook altogether. No more, based on conventional marketing, a tool like Google took over, as it combined product, marketing, and distribution as if they were a whole.

Third, even when consumers were quickly shifting to these new tools, it was very hard to acknowledge existing/dominating players.

In short, things might work the same for a long-time and then suddenly change. And when things do change, they do it so quickly that the dominating market position might be swept away pretty quickly.

Google: the King of the Web 1.0

Bach in the days, Brin and Page didn’t hide their resentment toward the advertising business model, which was the prevalent model for search. Indeed, in the paper “The Anatomy of a Large-Scale Hypertextual Web Search Engine” where Page and Brin presented their first prototype of Google.

With full text and hyperlink database of at least 24 million pages, in a paragraph dedicated to advertising, they explained: “We expect that advertising funded search engines will be inherently biased towards the advertisers and away from the needs of the consumers.“

The main issue they had toward advertising was the fact that it was biased and it caused a lot of spam in search results. Indeed, when they met Bill Gross, founder of GoTo, which would later become Overture, the encounter might not have been among the most cordial.

That’s because Bill Gross had figured the market for advertising had massive potential, as he introduced an auction-based system for bidding businesses, based on performance and clicks.

However, this was still back when Page and Brin were two academics completing their Ph.D. at Stanford University. The transition to becoming entrepreneurs would take soon to arrive. Indeed, as venture money was soon to be over a plan B was needed.

In addition, as Google managed to rank advertising based on relevance (for instance, by ranking higher those ads that got more clicks) advertising became a possible option. As Larry Page pointed out in the first Google letter to shareholders:

Advertising is our principal source of revenue, and the ads we provide are relevant and useful rather than intrusive and annoying.

Google revenues start to take off, yet the company would take a few years to become a “unicorn”

By 2000 Google was already a key player in the search industry. However, it wasn’t yet in the safe zone at a financial level. Indeed, in 2000 Google made $20 million in revenue. Even though it had launched its AdWords network, which would allow it to speed up its growth Google’s business model was still transitioning.

Some pieces of the puzzle were still missing. However, the first massive deal came into the door.

Overture was the father of pay-per-click advertising

By the end of the 1990s Bill Gross, founder of Idealab, an incubator where he could execute all his ideas, had also founded GoTo a search engine that for the first time used the pay-per-click business model.

In other words, in the past web portals, like AOL or Yahoo just sent undifferentiated traffic to websites. GoTo introduced a different logic. That of getting paid by the business advertising only when users clicked through it. Thus, only when there was relevant traffic.

The logic behind the GoTo business model might seem trivial today, but it was revolutionary at the time. In fact, with his pay-per-click Bill Gross would buy undifferentiated traffic from web portals at a low cost and sell that traffic for a much higher price.

GoTo soon changed its name to become Overture; while GoTo was both a search engine and an advertising network. Overture instead became merely an advertising network able to arbitrage the price difference between undifferentiated traffic and qualified traffic. Thus, Overture was the first to invent and prove the fact that the pay per click would be the business model of the internet.

At the time AOL was among the most prominent web portals, and among the most significant deals Overture had closed for its distribution strategy. At the time although Google was growing at a super-fast speed, it wasn’t any closer to being the market dominator it would become soon.

Google copied – part of – Overture’s business model and stole the AOL deal

By 2002 Google had finally launched its Google AdWords network that replicated that pay-per-click business model, and it improved on it. While it also figured out that if he wanted to scale up fast, it had to close large deals with web portals like AOL. Although nowadays AOL doesn’t sound to have any importance.

At the time it was among the most popular portals on the web. Known as America Online in 1998 it purchased Netscape, the dominant browser of that time. In short, there was a time when AOL was almost synonymous with the Internet.

In May 2002 the deal between AOL and Overture was expiring, and it was time for Google to take swift action. As reported in the book “Googled: The End of the World As We Know It” at the time Page said in relation to the AOL deal “I want us to bid to win,” while Kordestani in charge of business development and sales warned, “You’re betting the company if you do that.” According to Auletta’s account in the book Page replied to Kordestani “we should be able to monetize the pages, if not we deserve to go out of business.”

Whether or not those words are accurate that deal points out a critical aspect. At that point, Page and Brin were not only the engineers that had created PageRank but most of all shrewd entrepreneurs that understood the importance to close the right deals to kill competitors and dominate the market!

Overture sued for patent infringement then Yahoo settled the lawsuit with Google

Not long after the adoption of Google AdWord Overture sued it for patent infringement. The claim was that Google had copied the Overture model. However, after losing the AOL deal

Overture stock plunged 36 percent, with its stock at $21.99. Although the company would keep making high profits margins, it would never recover from that. In fact, in 2003 Yahoo bought Overture for $1.63 billion, valuing it at $24.63, roughly a 15 percent premium compared to its closing at the time of the deal.

Now part of Yahoo, in 2004, Google settled the Overture dispute. As reported in NY Times“Google agreed to give Yahoo 2.7 million shares, worth $291 million to $365 million if the shares sell within the range of $108 to $135 that Google has estimated for its initial offering price.”

It was the end of Overture and the rise of the most influential tech giant, today worth more than eight hundred billion dollars.

Google was primarily targeting technology from Applied Semantics called AdSense. It was the missing piece of the puzzle. In fact, with AdSense, Google could finally offer targeted ads on the websites of partners that joined the program. In short, Google would provide businesses with the chance to show their banners on the estate of those blogs which had become the heart of the web back in the 2000s.

It would also allow those blogs to jump from being amateurs to making some money via advertising. It was all tracked and based on the context of the page.

The AdSense value proposition was quite compelling. As pointed out in a 2004 financial report Google would “generate revenue by delivering relevant, cost-effective online advertising. Businesses use the AdWords program to promote their products and services with targeted advertising. Also, the thousands of third-party websites that comprise our Google Network use our Google AdSense program to deliver relevant ads that generate revenue and enhance the user experience.“

AdSense would become a critical part of the business.

Google embraced the whole web with its business model

At that stage, Google was ready to take off. Back in 2003 when Google had finally fine-tuned its business model, it had three primary constituencies:

Users: Google provided users with products and services that enabled them to find any information, quickly.

Advertisers: Google AdWords program, the auction-based advertising program allowed businesses to deliver ads both to customers on Google sites (for instance, the search page) and through the Google Network (any blog or site part of the AdSense program).

Websites: Google free products, Google AdWords and Google AdSense embraced the whole web. While users get information for free and quickly. Businesses could make money by sponsoring their products on Google and via the Google network. Publishers could also quickly monetize their content.

Once the business model had all the pieces, needed growth became the norm. If at all, Page and Brin had to make sure not to have Google implode for hypergrowth. Thus, the hardest challenge might have been managing hypergrowth that would continue for over two decades.

In 2014 Google restructured the company as Alphabet, with Google as a subsidiary. Beyond Search, today Alphabet offers services like YouTube, Maps, Play, Gmail, Android, and Chrome to billion of people worldwide.

The Google business model is way more diversified today than it was back in 2000. By 2017 Advertising still represented 86% of its revenues. Google – now Alphabet – also devoted part of its revenues to investing in bets which might become its next cash cow. Today those bets only represent over 1% of the total Google turnover.

In 2017, in the founders’ letter, Google explained how it started to roll out AI for several aspects comprised of its products:

understand images in Google Photos;

enable Waymo cars to recognize and distinguish objects safely;

significantly improve sound and camera quality in hardware;

understand and produce speech for Google Home;

translate over 100 languages in Google Translate;

caption over a billion videos in 10 languages on YouTube;

improve the efficiency of data centers;

suggest short replies to emails;

help doctors diagnose diseases, such as diabetic retinopathy;

discover new planetary systems;

create better neural networks (AutoML);

… and much more.

By 2019, Google confirmed its “AI-first” strategy. Indeed, on a stage at the Google I/O conference, Pichai highlighted:

We are moving from a company that helps you find answers to a company that helps you get things done, we want our products to work harder for you in the context of your job, your home and your life.

This change was critical, as it moved the mission of the company from “organizing the world’s information and making it universally accessible and useful” to “helping you get things done.”

This is a critical move, from a business standpoint, as Google highlighted its focus on generating revenues based on its productivity tools. The segment that for decades had helped Microsoft remain among the largest tech players.

No wonder then, that Google free tools play a key role in that.

Today Google employs sophisticated language models, trained on billions of parameters, which in the future might be used to enable the search engine to generate more and more specific answers to users’ queries.

Let’s keep in mind, that after almost 25 years after the company’s inception, Google still has many challenges ahead.

Google’s business model today

As we saw, Google is a platform, and a tech media company running an attention-based business model. As of 2021, Alphabet’s Google generated over $257 billion in revenue.

Over $209 billion (more than 81% of the total revenues) came from Google Advertising products (Google Search, YouTube Ads, and Network Members sites).

They were followed by over $28 billion in other revenues (comprising Google Play, Pixel phones, and YouTube Premium), and by Google Cloud, which generated over $19 billion in 2021.

While Google, now Alphabet, has been diversifying its business model for more than a decade. Its main revenue stream is Google’s search engine, which generated about $149 billion in revenue in 2021.

Followed by the network members’ websites (the sites that adhere to Google AdSense for a revenue share on top of the advertising revenues generated on their properties).

And YouTube Ads, which generated about $29 billion (this excludes YouTube Prime Memberships, which are comprised of the other revenues).

Among the bets which Alphabet has placed over the years, there are ventures in the seld-driving industry, robotics, sustainable/renewable energies, and more.

Google’s Alphabet is one of the most successful tech players of our time. While Alphabet now is a vertically integrated company that goes beyond Google’s search engine. In reality, the Google search engine still plays a key role in the overall organization. In fact, Google is the main asset that provides resources to Alphabet to keep investing in new areas, keep integrating its supply chain, and also placing bets in completely new and unrelated areas.

Google in numbers today

Google’s profitability has slightly improved in 2021, thanks to the fact it managed to increase its revenue faster than it increased its operational costs, as traffic on its platforms increased substantially during 2020-2021.

For the first time in its history, Google generated over $257 billion in revenue. And the company almost reached a two trillion market capitalization.

For some context, when Google IPOed in 2004, it recorded almost a billion in revenues, and it was worth about $23 billion, as it popped at its IPO date to $85 per share (On April 7th, 2022, a Google stock is worth $2,743.52).

At the time, in 2004, Google had just managed to scale its advertising machine comprised mainly of Google AdWords (today Google Ads) and Google AdSense. At the time the advertising machine was primarily based on Internet traffic from desktop devices. That was a completely different world.

As we’ll see throughout this analysis, today most traffic comes from mobile. And Google’s mobile ads platforms (Google AdMob) play a key role. So let’s dive a bit into the main financial segments of Google.

Google’s main segments in 2021

In 2021, the Google advertising machine generated over $209 billion in revenue. This represented an over 42% growth, year over year! This is a massive improvement for a company worth almost two trillion. In a market landscape that is no anymore in favor of digital advertising.

How did Google pull this off?

We’ll see this shortly. But for now, let’s emphasize a few key points.

Today the Google advertising machine is comprised of three main products:

Google Search/Properties: This represents the set of products that Google owns, from the search engines to all the other vertical platforms that the company operates (Google Discover, Google News, Google Travel, and more). In 2021, this segment generated over $148 billion!

YouTube: This is of course one of the most successful business acquisitions ever done. It was acquired by Google for $1.65 billion in 2006. It’s important to notice that Google was able to integrate YouTube and scale it up. A feat that not every other company would have been able to achieve. At the time YouTube was getting sued for various copyright infringements (the platform is comprised of user-generated content, often posting copyrighted materials) that would have most probably bankrupted it if it had stayed a startup without Google’s backing. By 2021, YouTube has become an advertising machine generating over $28 billion (this doesn’t count the YouTube memberships, which are reported separately).

And Google Network Members’ properties: this is the set of publishers that decide to opt into Google’s advertising network (either AdSense for desktop, or AdMob for in-app advertising). Here Google shows advertising on the network members’ properties, thus splitting the revenues with them. In 2021, Google’s network members generated over $31 billion of revenue.

As we’ll see understanding the difference among these segments helps us understand how Google manages its cost structure for each segment.

What determines the growth of each segment?

Google’s search advertising has been driven by growth in search queries. In fact, since the pandemic hit, more and more users started to use Google’s products. This trend has continued. However, most of it was driven by mobile users’ growth. This is an important aspect, as it shows that Google’s main driver of growth is based on mobile traffic. This changes the way the company needs to prioritize its product developments efforts, its ad formats served to users, and also how it experiments.

YouTube growth was driven primarily by improved ad formats. This means that Alphabet (as it’s evident to anyone going on YouTube) has ramped up the advertising operations on YouTube. In short, on YouTube now there are way more ads than before. This “improved ad formats” is the result of YouTube’s extreme stickiness with users, which enables Alphabet to play with its ad formats.

Google’s network members’ properties were primarily driven by AdMob. In short, the mobile advertising platform, powered up by Android devices through the Google Play store, was the main driver of revenue growth in 2021. This shows how Google has shifted also its focus on the mobile advertising platform.

Let’s see how, a little bit more in detail, ad monetization changed for Google.

The Google advertising machine today

In 2021, three main factors determined the improvement in ad monetization by Google.

First, Google recorded an increase in paid clicks (driven by an increase in user adoption and search queries primarily on mobile devices).

Second, this also drove more paid clicks in AdMob through the Google Play store.

Third, as we saw Google is testing various ad formats (we can argue it’s showing more ads) both on Google’s products and YouTube, which slightly improved monetization.

Among the other revenues, instead, Google Cloud also recorded an important growth thanks to the Google Cloud Platform.

Where instead, both the Google Cloud platform and the other Google Bets run at negative margins. Important to distinguish here.

The Google Cloud platform is critical for the future success of the Google AI platform.

At the end of it all, Google remains a machine transforming traffic into revenues, how?

The traffic acquisition cost represents the expenses incurred by an internet company, like Google, to gain qualified traffic – on its pages – for monetization. Over the years Google has been able to reduce its traffic acquisition costs and in any case, keep it stable. In 2021 Google spent 21.75% of its total advertising revenues (over $45.56 billion) to guarantee its traffic on several desktop and mobile devices across the web.

The traffic acquisition cost represents the expenses incurred by an internet company, like Google, to gain qualified traffic – on its pages – for monetization.

Over the years Google has been able to reduce its traffic acquisition costs and in any case, keep it stable. In 2021 Google spent 21.75% of its total advertising revenues (over $45.56 billion) to guarantee its traffic on several desktop and mobile devices across the web.

When you look at a business model like that of Google, which is primarily a software/digital/tech company, it’s easy to fall into the trap of thinking it’s an asset-light business.

Indeed, a software company is asset-light compared to much more traditional industries (for instance manufacturing) but they do have massive expenses to guarantee their distribution strategy.

For instance, in 2021, Google spent over $45 billion in traffic acquisition costs, which comprise costs incurred to cut distribution deals with other companies (like the multi-billion deal Google has to be the default search engine on Apple’s Safari), and many other deals, together with the money paid to partners to bring traffic back to the Google’s properties.

Now, keeping this number stable over time, is critical, to assessing the health of the advertising machine. In fact, on top of the traffic that Google generates, the company is able to monetize it many times over.

For instance, in 2021, Google spent over $45 billion in traffic acquisition costs, but it generated over $209 billion in advertising revenues.

This means that Google was able to monetize its traffic 4.6 times its traffic acquisition costs.

Companies like Google have to cut distribution deals and split revenues with content partners to bring traffic back to their main properties online. For instance, in 2021, Google spent over $45 billion in traffic acquisition costs, but it generated over $209 billion in advertising revenues.

This means that Google could monetize its traffic 4.6 times its traffic acquisition costs. An increased monetization multiple over the years is a good sign. It means that Google was able to keep its advertising machine competitive. On the opposite side, a negative monetization multiple means the advertising machine is losing traction.

As you can notice from the above, this is a purely financial metric, which needs to be balanced out with a qualitative analysis of why the metric increased in the first place.

Indeed, it’s critical to keep into account these questions:

Has monetization increased thanks to an improved UX? Or is monetization worsening the UX?

Has monetization improved thanks to an increased customer base? Or has it increased due to higher prices per ad?

Lastly, how is monetization balanced with legal risks posed by increased tracking?

All these questions are critical to answer, because, financially Google’s advertising machine seems as strong as ever. There are hidden risks underlying it, which might, all of a sudden threaten its overall business model.

In fact:

On a positive note, Google has managed to further scale, as a consequence of the pandemic. Thus, bringing its products to hundreds of millions of new users. Yet. this further scale (especially on mobile devices) has created new challenges for the company. Which is finding it harder and harder to properly index a web made of billions and billions of pages, and growing. This poses a threat in the long term, as it might reduce the quality of organic search results.

To monetize this expanded user base, Google is serving more ads. This might work in the short term to squeeze the advertising machine. But it might make the overall experience bad in the long term. So it’s critical to balance these things out.

To further expand its revenues, the company has also increased the price per ad. While, in the short-term, the strategy works, in the long-term, this might substantially reduce the customer base.

Where is the next wave headed?

When Google wrecked apart the tech giants of the early Internet era, it built its competitive advantage by enabling users to find information around the exponentially growing number of web pages. This balance was broken when back in the 2015s Google started to roll out more and more features to keep users on its search results pages.

In February 2009, about twenty years from the first version of the Hypertext project, Tim Berners-Lee stood on a TED stage in Long Beach, California. As he opened the speech he remarked how 20 years had passed since the inception of the project that would lead to the web, and yet for 18 months that project, back in 1989 stood on a desk at the CERN, without anyone doing anything about it.

Until Tim Berners-Lee volunteered to do it as a side project!

In that time span, Tim Berners-Lee had laid the foundation for HTML, and the idea of URLs that stood behind HTTP. As he remarked in 2009, he felt compelled to take that side project, as he worked in a large research lab and felt extremely frustrated by the fragmentation that existed at the time.

There was no single protocol or framework that could connect all the various programs and make them talk. That is how the web was conceived, as a massive document that connected all other documents via hyperlinks. And yet by 2009, Tim Berners-Lee highlighted another frustration, that of connecting data. Up until that point, therefore, the web connected text and documents but failed to connect data.

Tim Berners-Lee explained that concept with these words:

So I want us now to think about not just two pieces of data being connected or six like he did, but I want to think about a world where everybody has put data on the web and so virtually everything you can imagine is on the web and then calling that linked data.

This would give the rise to the Semantic Web, which has already become a reality. Indeed, if we look at Google itself a good chunk of queries that it serves to users are served from its Knowledge Graph, a massive database made (as of 2020) of more than 500 billion facts about five billion entities (an entity is anything that exists on the web, it can be a person, a place, an event and so forth).

It’s important to note that already now, Google (with the Knowledge Graph), Facebook (with the Social Graph), and all the other tech giants, in a form, have already converted their “databases” into powerful Graphs.

Yet while these companies put together massive amounts of data about anything on the web, their algorithms are still siloed, walled, and managed as “proprietary data.”

Thus, while these semantic technologies did turn into advanced features for users at scale (think of how voice assistants can give answers to millions of questions) they do not talk to each other, and they might never talk to each other (why would Google, now Alphabet cooperate with Amazon? Or vice versa? when perhaps they are fighting against each other for advertising revenues? – which might also be relevant for the future digital marketing landscape – the only exception is they might come together only to fight regulation).

This is also where the Blockchain ecosystem becomes interesting. As the data that sits on the Blockchain protocols, this is usually open and accessible. In this sense, Web 3.0, as also intended by Ethereum’s co-founder Gavin Wood (who also built Solidity, which is the native language of the Ethereum Blockchain) would achieve its vision:

Web 3.0 is an inclusive set of protocols to provide building blocks for application makers. These building blocks take the place of traditional web technologies like HTTP, AJAX and MySQL, but present a whole new way of creating applications. These technologies give the user strong and verifiable guarantees about the information they are receiving, what information they are giving away, and what they are paying and what they are receiving in return. By empowering users to act for themselves within low-barrier markets, we can ensure censorship and monopolization have fewer places to hide. Consider Web 3.0 to be an executable Magna Carta — ‘the foundation of the freedom of the individual against the arbitrary authority of the despot.

The Unexpected Disruptor: OpenAI!

Back in 2005, Sam Altman founded a startup called Loopt (a location-based social app), which was accepted into the first batch of YCombinator.

Loopt wouldn’t turn to be a tech giant (it was sold for $43.4M in 2012), yet Sam Altman was hooked by the experience.

Once he understood that as an entrepreneur he could create a major impact into the world, he never got back to Stanford!

Over the years he took the role of president at YCombinator, successfully placing angel bets into companies like Airbnb, Pinterest, Reddit, and many others.

And yet he kept an eye on the AI field.

Indeed, as a computer science student at Stanford, he got passionate about AI, even though the field was stuck.

Something excited him, at the point of starting to devote a good chunk of his time to that, it was Imagenet (we’re in 2012).

A large scale AI engine, which for the first time in years, showed that neural nets might be able to achieve great things.

From that point forward, Sam Altman started to think in ways he could contribute to this revolution.

So together with Elon Musk, Ilya Sutskever, Greg Brockman and Wojciech Zaremba they started OpenAI.

A research lab with the mission to build AGI (artificial general intelligence).

The turning point for OpenAI came in 2018, when thanks to a new AI architecture (called transformer) neural nets started to do interesting thing.

This lead to the release of GPT (Generative Pre-trained Transformer), a massive text-to-text language model, that via prompting (give it a natural language instruction) could successfully predict the next lines it was generating, thus starting to become extremely good in text generation.

That was a revelation that none expected! From the sheer force of scaling up these models, interesting things started to happen, and GPT didn’t just get slightly better, it improved exponentially from 2018-2022.

Which also led, in 2019 to an important business transition. OpenAI turned, from, a research lab into a for-profit organization, partnering up with players like Microsoft to build the next AI revolution!

OpenAI has built the foundational layer of the AI industry. With large generative models like GPT-3 and DALL-E, OpenAI offers API access to businesses that want to develop applications on top of its foundational models while being able to plug these models into their products and customize these models with proprietary data and additional AI features. On the other hand, OpenAI also released ChatGPT, developing around a freemium model. Microsoft also commercializes opener products through its commercial partnership.

From there, OpenAI released GPT-2.

In 2020, it then released GPT-3.

And when in November 2022, OpenAI released ChatGPT it blew away the world, and opened up the greatest challenge to the entire history of Google to these days!

InstructGPT is the successor to the GPT-3 large language model (LLM) developed by OpenAI.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.