Peer-to-peer lending is a form of online marketplace lending where individuals or businesses seeking loans are connected directly with investors willing to fund those loans. These platforms, also known as P2P lending platforms or online lending marketplaces, act as intermediaries that facilitate the lending process. P2P lending differs from traditional lending models, where financial institutions like banks serve as intermediaries between borrowers and lenders.

Key characteristics of peer-to-peer lending include:

Online Platforms: P2P lending operates through online platforms, which provide a marketplace for borrowers and lenders to connect.

Diverse Borrowers: Borrowers on P2P platforms can range from individuals seeking personal loans to small businesses in need of working capital.

Investor Diversification: Investors can fund a portion of multiple loans, spreading their risk across a diverse portfolio.

Risk Assessment: P2P platforms typically assess borrowers’ creditworthiness and assign them a risk grade, helping investors make informed decisions.

Interest Rates: Interest rates are determined through a competitive bidding process, allowing borrowers to secure loans at potentially lower rates than traditional lenders.

To fully grasp the mechanics of P2P lending, let’s explore how the process typically works:

1. Borrower Application

A borrower applies for a loan through a P2P lending platform by filling out an online application. The application includes information about the borrower’s credit history, financial situation, loan amount, and purpose.

2. Credit Assessment

The P2P platform assesses the borrower’s creditworthiness using various data points, including credit reports, income verification, and other relevant information. Borrowers are assigned a risk grade or credit rating.

3. Loan Listing

Once approved, the loan is listed on the platform’s marketplace, where registered investors can review loan details, risk assessments, and interest rates associated with the loan.

4. Investor Participation

Investors can fund loans in fractional amounts, allowing them to diversify their investments across multiple loans. Investors may choose loans based on their risk tolerance and return expectations.

5. Competitive Bidding

Interest rates for loans are determined through a competitive bidding process. Investors place bids specifying the interest rate at which they are willing to fund the loan.

6. Loan Funding

When enough investors have bid on a loan to meet the requested loan amount, the loan is considered fully funded. Borrowers receive the funds directly from the investors.

7. Loan Repayment

Borrowers make regular monthly payments, including principal and interest, to the P2P platform. The platform then distributes these payments to the investors who funded the loan.

8. Returns for Investors

Investors earn returns on their investments through the interest payments made by borrowers. Returns are influenced by the interest rates set during the bidding process and the loan’s performance.

9. Default and Collections

In cases of borrower default, P2P platforms typically have collection procedures in place to recover funds on behalf of investors. This may include working with collection agencies or pursuing legal action.

Significance of Peer-to-Peer Lending

Peer-to-peer lending has brought about significant changes in the financial landscape, offering numerous advantages and benefits to both borrowers and investors. Understanding its significance helps individuals and businesses appreciate the impact of P2P lending. Here are some key aspects of its significance:

Accessibility

P2P lending provides access to financing for individuals and small businesses that may have difficulty obtaining loans through traditional banks or financial institutions.

Competitive Interest Rates

Borrowers on P2P platforms can often secure loans at competitive interest rates, as interest rates are determined through a transparent and competitive process.

Diversification for Investors

Investors can diversify their portfolios by funding multiple loans across different risk grades, potentially reducing overall risk.

Higher Returns

P2P lending can offer attractive returns for investors, especially when compared to traditional savings accounts or fixed-income investments.

Efficiency and Speed

The online nature of P2P lending platforms streamlines the borrowing and lending process, reducing paperwork and approval times.

Risk Assessment

P2P platforms typically employ robust risk assessment algorithms, helping to match borrowers with suitable investors.

Innovation and Disruption

P2P lending has disrupted traditional lending models, fostering innovation and competition in the financial sector.

Types of Peer-to-Peer Lending

Peer-to-peer lending has expanded to encompass various types of loans and borrowers. Some common types of P2P lending include:

1. Personal Loans

Individuals may seek personal loans through P2P lending platforms for various purposes, such as debt consolidation, home improvement, or unexpected expenses.

2. Business Loans

Small businesses often use P2P lending to secure working capital, purchase inventory, or fund expansion plans.

3. Student Loans

P2P platforms offer student loans to finance higher education expenses, serving as an alternative to traditional student loans.

4. Real Estate Loans

Real estate crowdfunding platforms leverage the P2P lending model to allow investors to participate in real estate projects, including residential and commercial properties.

5. Auto Loans

Borrowers may use P2P lending to finance the purchase of vehicles, whether new or used.

6. Green Loans

Some P2P platforms specialize in loans for eco-friendly and sustainable projects, supporting environmentally conscious initiatives.

Participating in Peer-to-Peer Lending

Participating in P2P lending can be a rewarding financial endeavor, but it requires careful consideration and due diligence. Here are practical insights for both borrowers and investors:

For Borrowers:

Assess Your Needs: Determine the purpose and amount of the loan you need, as well as your ability to make regular payments.

Compare Platforms: Research and compare different P2P lending platforms, considering factors such as interest rates, fees, and user reviews.

Complete the Application: Fill out the loan application accurately and provide all required documentation.

Review Offers: Once your loan is listed on the platform, review offers from investors, including the interest rates and terms.

Select Offers: Choose the offers that best meet your needs and accept them to secure your loan.

Make Timely Payments: Commit to making timely monthly payments to repay the loan.

For Investors:

Understand Your Risk Tolerance: Assess your risk tolerance and investment goals before participating in P2P lending.

Diversify Your Portfolio: Diversify your investments by funding multiple loans across different risk grades to spread risk.

Conduct Due Diligence: Review loan listings thoroughly, considering borrower profiles, risk assessments, and loan purposes.

Set Investment Criteria: Establish criteria for the types of loans you are willing to fund, including minimum interest rates and risk grades.

Monitor Your Portfolio: Regularly monitor the performance of your loan portfolio and reinvest returns to maintain diversification.

Be Prepared for Defaults: Acknowledge that defaults may occur, and have a strategy in place for dealing with them.

Risks and Challenges

While P2P lending offers various advantages, it is not without risks and challenges. Borrowers and investors should be aware of the following considerations:

Credit Risk

There is a risk of borrowers defaulting on loans, which can result in a loss of principal for investors.

Lack of Liquidity

Investors may not have immediate access to their invested funds, as loan terms can range from months to years.

Platform Risk

P2P lending platforms themselves may face financial or operational challenges, impacting the overall health of the investment.

Regulatory Changes

Changes in regulations can affect the operations of P2P lending platforms and the protection of investors and borrowers.

Marketplace Saturation

The popularity of P2P lending has led to increased competition among investors, potentially impacting returns.

Economic Conditions

Economic downturns or financial crises can affect the creditworthiness of borrowers and the performance of loans.

Conclusion

Peer-to-peer lending has emerged as a transformative force in the world of finance, offering individuals and businesses new opportunities for borrowing and investing. Its significance lies in its accessibility, efficiency, and potential for diversification and returns. However, participants in P2P lending, whether borrowers or investors, should approach it with careful consideration, thorough research, and an awareness of the associated risks. By understanding the mechanics, types, and challenges of P2P lending, individuals can make informed decisions that align with their financial goals and needs. Peer-to-peer lending represents a notable chapter in the ongoing evolution of the financial industry, one that empowers individuals to take control of their financial future.

Key Highlights:

Definition: Peer-to-peer (P2P) lending involves online platforms that connect borrowers directly with lenders, bypassing traditional financial institutions like banks.

Characteristics: P2P lending operates online, offers diverse borrowers, allows investor diversification, conducts risk assessment, and determines interest rates through competitive bidding.

Mechanics: The process includes borrower application, credit assessment, loan listing, investor participation, competitive bidding, loan funding, repayment, returns for investors, and default handling.

Significance: P2P lending provides accessibility to financing, competitive interest rates, diversification for investors, higher returns, efficiency, risk assessment, and fosters innovation in the financial sector.

Types: Common types include personal loans, business loans, student loans, real estate loans, auto loans, and green loans.

Participation: Borrowers should assess needs, compare platforms, complete applications, review and select offers, and make timely payments. Investors should understand risk tolerance, diversify portfolios, conduct due diligence, set investment criteria, monitor portfolios, and be prepared for defaults.

Risks and Challenges: Risks include credit risk, lack of liquidity, platform risk, regulatory changes, marketplace saturation, and economic conditions.

Conclusion: P2P lending offers transformative opportunities but requires careful consideration and understanding of mechanics, types, participation, and associated risks for both borrowers and investors.

In a functional organizational structure, groups and teams are organized based on function. Therefore, this organization follows a top-down structure, where most decision flows from top management to bottom. Thus, the bottom of the organization mostly follows the strategy detailed by the top of the organization.

In a flat organizational structure, there is little to no middle management between employees and executives. Therefore it reduces the space between employees and executives to enable an effective communication flow within the organization, thus being faster and leaner.

Project portfolio management (PPM) is a systematic approach to selecting and managing a collection of projects aligned with organizational objectives. That is a business process of managing multiple projects which can be identified, prioritized, and managed within the organization. PPM helps organizations optimize their investments by allocating resources efficiently across all initiatives.

Harvard Business School professor Dr. John Kotter has been a thought-leader on organizational change, and he developed Kotter’s 8-step change model, which helps business managers deal with organizational change. Kotter created the 8-step model to drive organizational transformation.

The Nadler-Tushman Congruence Model was created by David Nadler and Michael Tushman at Columbia University. The Nadler-Tushman Congruence Model is a diagnostic tool that identifies problem areas within a company. In the context of business, congruence occurs when the goals of different people or interest groups coincide.

McKinsey’s Seven Degrees of Freedom for Growth is a strategy tool. Developed by partners at McKinsey and Company, the tool helps businesses understand which opportunities will contribute to expansion, and therefore it helps to prioritize those initiatives.

Mintzberg’s 5Ps of Strategy is a strategy development model that examines five different perspectives (plan, ploy, pattern, position, perspective) to develop a successful business strategy. A sixth perspective has been developed over the years, called Practice, which was created to help businesses execute their strategies.

The COSO framework is a means of designing, implementing, and evaluating control within an organization. The COSO framework’s five components are control environment, risk assessment, control activities, information and communication, and monitoring activities. As a fraud risk management tool, businesses can design, implement, and evaluate internal control procedures.

The TOWS Matrix is an acronym for Threats, Opportunities, Weaknesses, and Strengths. The matrix is a variation on the SWOT Analysis, and it seeks to address criticisms of the SWOT Analysis regarding its inability to show relationships between the various categories.

Lewin’s change management model helps businesses manage the uncertainty and resistance associated with change. Kurt Lewin, one of the first academics to focus his research on group dynamics, developed a three-stage model. He proposed that the behavior of individuals happened as a function of group behavior.

OpenAI is an artificial intelligence research laboratory that transitioned into a for-profit organization in 2019. The corporate structure is organized around two entities: OpenAI, Inc., which is a single-member Delaware LLC controlled by OpenAI non-profit, And OpenAI LP, which is a capped, for-profit organization. The OpenAI LP is governed by the board of OpenAI, Inc (the foundation), which acts as a General Partner. At the same time, Limited Partners comprise employees of the LP, some of the board members, and other investors like Reid Hoffman’s charitable foundation, Khosla Ventures, and Microsoft, the leading investor in the LP.

Airbnb follows a holacracy model, or a sort of flat organizational structure, where teams are organized for projects, to move quickly and iterate fast, thus keeping a lean and flexible approach. Airbnb also moved to a hybrid model where employees can work from anywhere and meet on a quarterly basis to plan ahead, and connect to each other.

The Amazon organizational structure is predominantly hierarchical with elements of function-based structure and geographic divisions. While Amazon started as a lean, flat organization in its early years, it transitioned into a hierarchical organization with its jobs and functions clearly defined as it scaled.

The Coca-Cola Company has a somewhat complex matrix organizational structure with geographic divisions, product divisions, business-type units, and functional groups.

Costco has a matrix organizational structure, which can simply be defined as any structure that combines two or more different types. In this case, a predominant functional structure exists with a more secondary divisional structure.

Costco’s geographic divisions reflect its strong presence in the United States combined with its expanding global presence. There are six divisions in the country alone to reflect its standing as the source of most company revenue.

Compared to competitor Walmart, for example, Costco takes more a decentralized approach to management, decision-making, and autonomy. This allows the company’s stores and divisions to more flexibly respond to local market conditions.

Dell has a functional organizational structure with some degree of decentralization. This means functional departments share information, contribute ideas to the success of the organization and have some degree of decision-making power.

eBay was until recently a multi-divisional (M-form) organization with semi-autonomous units grouped according to the services they provided. Today, eBay has a single division called Marketplace, which includes eBay and its international iterations.

Facebook is characterized by a multi-faceted matrix organizational structure. The company utilizes a flat organizational structure in combination with corporate function-based teams and product-based or geographic divisions. The flat organization structure is organized around the leadership of Mark Zuckerberg, and the key executives around him. On the other hand, the function-based teams are based on the main corporate functions (like HR, product management, investor relations, and so on).

Goldman Sachs has a hierarchical structure with a clear chain of command and defined career advancement process. The structure is also underpinned by business-type divisions and function-based groups.

Google (Alphabet) has a cross-functional (team-based) organizational structure known as a matrix structure with some degree of flatness. Over the years, as the company scaled and it became a tech giant, its organizational structure is morphing more into a centralized organization.

IBM has an organizational structure characterized by product-based divisions, enabling its strategy to develop innovative and competitive products in multiple markets. IBM is also characterized by function-based segments that support product development and innovation for each product-based division, which include Global Markets, Integrated Supply Chain, Research, Development, and Intellectual Property.

McDonald’s has a divisional organizational structure where each division – based on geographical location – is assigned operational responsibilities and strategic objectives. The main geographical divisions are the US, internationally operated markets, and international developmental licensed markets. And on the other hand, the hierarchical leadership structure is organized around regional and functional divisions.

McKinsey & Company has a decentralized organizational structure with mostly self-managing offices, committees, and employees. There are also functional groups and geographic divisions with proprietary names.

Microsoft has a product-type divisional organizational structure based on functions and engineering groups. As the company scaled over time it also became more hierarchical, however still keeping its hybrid approach between functions, engineering groups, and management.

Nestlé has a geographical divisional structure with operations segmented into five key regions. For many years, Swiss multinational food and drink company Nestlé had a complex and decentralized matrix organizational structure where its numerous brands and subsidiaries were free to operate autonomously.

Nike has a matrix organizational structure incorporating geographic divisions. Nike’s matrix structure is also present at the regional and sub-regional levels. Managerial responsibility is segmented according to business unit (apparel, footwear, and equipment) and function (human resources, finance, marketing, sales, and operations).

Patagonia has a particular organizational structure, where its founder, Chouinard, disposed of the company’s ownership in the hands of two non-profits. The Patagonia Purpose Trust, holding 100% of the voting stocks, is in charge of defining the company’s strategic direction. And the Holdfast Collective, a non-profit, holds 100% of non-voting stocks, aiming to re-invest the brand’s dividends into environmental causes.

Samsung has a product-type divisional organizational structure where products determine how resources and business operations are categorized. The main resources around which Samsung’s corporate structure is organized are consumer electronics, IT, and device solutions. In addition, Samsung leadership functions are organized around a few career levels grades, based on experience (assistant, professional, senior professional, and principal professional).

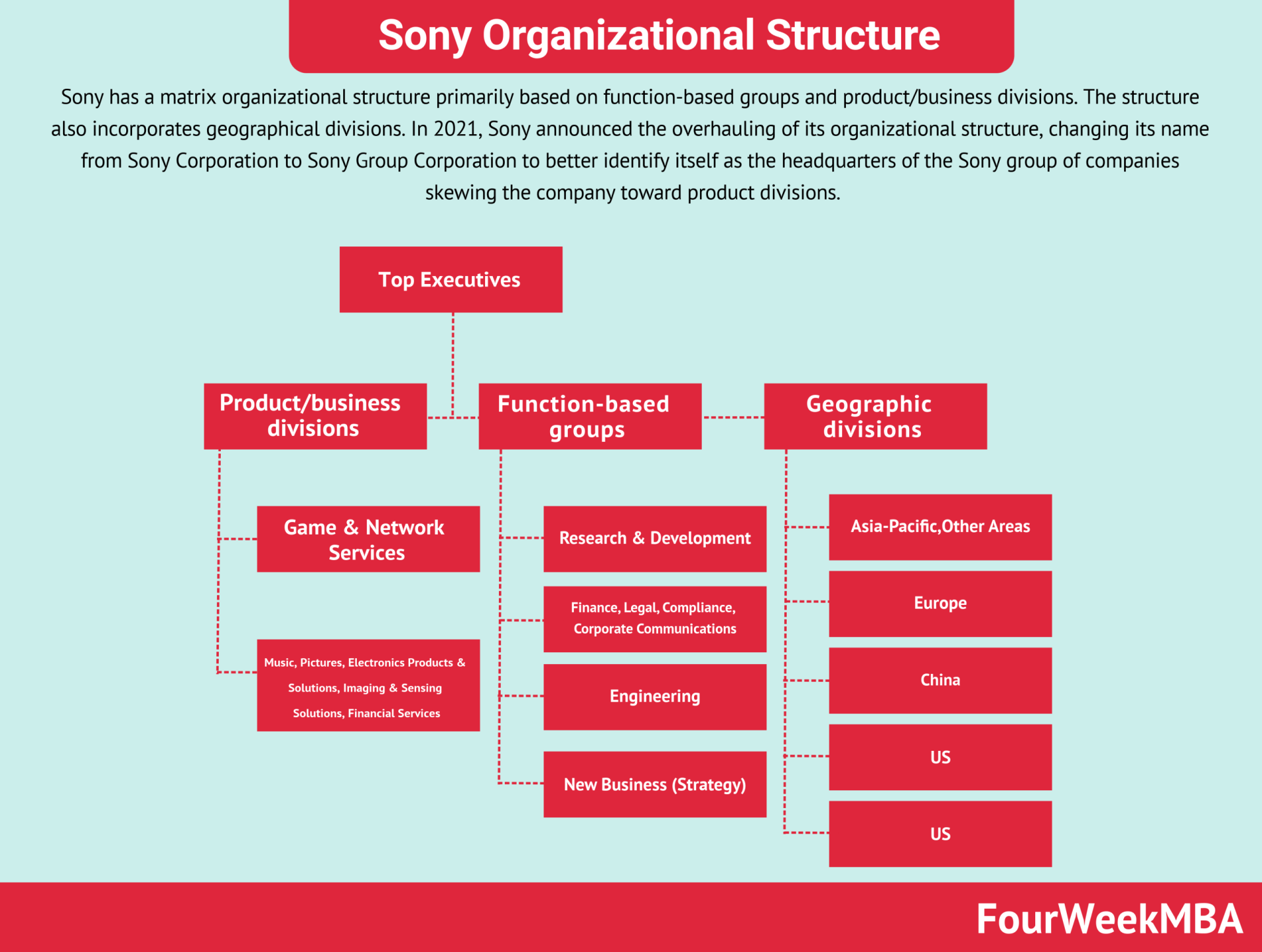

Sony has a matrix organizational structure primarily based on function-based groups and product/business divisions. The structure also incorporates geographical divisions. In 2021, Sony announced the overhauling of its organizational structure, changing its name from Sony Corporation to Sony Group Corporation to better identify itself as the headquarters of the Sony group of companies skewing the company toward product divisions.

Starbucks follows a matrix organizational structure with a combination of vertical and horizontal structures. It is characterized by multiple, overlapping chains of command and divisions.

Tesla is characterized by a functional organizational structure with aspects of a hierarchical structure. Tesla does employ functional centers that cover all business activities, including finance, sales, marketing, technology, engineering, design, and the offices of the CEO and chairperson. Tesla’s headquarters in Austin, Texas, decide the strategic direction of the company, with international operations given little autonomy.

Toyota has a divisional organizational structure where business operations are centered around the market, product, and geographic groups. Therefore, Toyota organizes its corporate structure around global hierarchies (most strategic decisions come from Japan’s headquarter), product-based divisions (where the organization is broken down, based on each product line), and geographical divisions (according to the geographical areas under management).

Walmart has a hybrid hierarchical-functional organizational structure, otherwise referred to as a matrix structure that combines multiple approaches. On the one hand, Walmart follows a hierarchical structure, where the current CEO Doug McMillon is the only employee without a direct superior, and directives are sent from top-level management. On the other hand, the function-based structure of Walmart is used to categorize employees according to their particular skills and experience.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.