Risk pooling is a fundamental concept in finance, insurance, and risk management. It involves the practice of aggregating various individual risks or exposures into a larger, more diversified pool to reduce the impact of adverse events on any single entity or individual. This risk management strategy plays a crucial role in ensuring financial stability, providing insurance coverage, and optimizing resource allocation.

Risk pooling is a strategy used to manage and mitigate risk by combining the risks of multiple entities or individuals. By aggregating these risks, the overall variability and impact of individual risks are reduced, leading to more predictable outcomes. This concept is widely used in various fields, including insurance, supply chain management, and finance.

Key Characteristics of Risk Pooling

Risk Aggregation: Combining risks from multiple sources to reduce the impact of individual risks.

Predictability: Increasing the predictability of outcomes by spreading risks across a larger group.

Risk Sharing: Distributing the impact of risks among all participants in the pool.

Importance of Understanding Risk Pooling

Understanding and effectively using risk pooling is crucial for enhancing risk management, reducing variability, and improving decision-making.

Enhancing Risk Management

Risk Mitigation: Reduces the impact of individual risks by spreading them across a larger group.

Stability: Provides stability and resilience by managing uncertainties collectively.

Reducing Variability

Predictable Outcomes: Leads to more predictable and stable outcomes by averaging out individual risks.

Reduced Volatility: Minimizes the volatility associated with individual risk factors.

Improving Decision-Making

Informed Choices: Enables better decision-making by providing a clearer understanding of aggregated risks.

Resource Allocation: Facilitates efficient allocation of resources by reducing uncertainty.

Components of Risk Pooling

Risk pooling involves several key components that contribute to its effectiveness in managing and mitigating risk.

1. Risk Identification

Risk Assessment: Identifying the types of risks faced by individual entities or participants.

Risk Categories: Categorizing risks based on their nature and potential impact.

2. Risk Aggregation

Combining Risks: Aggregating risks from multiple entities to form a risk pool.

Pooling Mechanisms: Establishing mechanisms for combining and managing the aggregated risks.

3. Risk Sharing

Distribution: Distributing the impact of risks across all participants in the pool.

Equitable Sharing: Ensuring that the sharing of risks is fair and proportionate.

4. Risk Management

Strategies: Developing strategies to manage the aggregated risks effectively.

Mitigation Measures: Implementing measures to mitigate the impact of pooled risks.

Methods of Risk Pooling

Several methods can be used to implement risk pooling effectively, each offering different strategies and tools.

1. Insurance

Premiums: Collecting premiums from policyholders to create a pool of funds for covering losses.

Claims: Paying out claims from the pooled funds to compensate for individual losses.

2. Supply Chain Risk Pooling

Inventory Pooling: Combining inventory from multiple locations to reduce stockouts and excess inventory.

Demand Aggregation: Aggregating demand across different markets to stabilize supply chain operations.

3. Financial Risk Pooling

Diversified Portfolios: Creating diversified investment portfolios to spread financial risks.

Risk Sharing Agreements: Establishing agreements to share financial risks among participants.

4. Health Care Risk Pooling

Health Insurance Pools: Creating health insurance pools to spread medical costs across a large group.

Public Health Initiatives: Implementing public health initiatives that pool resources for disease prevention and treatment.

5. Cooperative Arrangements

Cooperatives: Forming cooperatives where members pool resources and share risks collectively.

Mutual Aid Agreements: Establishing mutual aid agreements to support each other in times of need.

Risk Reduction: Reduces the impact of individual risks by spreading them across a larger group.

Stability: Provides stability and resilience in managing uncertainties.

Increased Predictability

Stable Outcomes: Leads to more predictable and stable outcomes by averaging out individual risks.

Reduced Volatility: Minimizes the volatility associated with individual risk factors.

Cost Efficiency

Economies of Scale: Achieves economies of scale by pooling resources and risks.

Cost Sharing: Reduces the cost burden on individual participants through collective sharing.

Improved Resource Allocation

Efficient Use: Facilitates efficient allocation of resources by reducing uncertainty.

Informed Decisions: Enables better decision-making by providing a clearer understanding of aggregated risks.

Challenges of Risk Pooling

Despite its benefits, implementing risk pooling presents several challenges that need to be managed for successful implementation.

Adverse Selection

Risk Imbalance: Higher-risk individuals or entities may be more likely to join the risk pool, leading to an imbalance.

Premium Setting: Difficulty in setting appropriate premiums or contributions to reflect individual risk levels.

Moral Hazard

Behavior Change: Participants may take on more risks knowing that the impact is shared with others.

Monitoring: Difficulty in monitoring and controlling risk-taking behavior among participants.

Administrative Complexity

Coordination: Coordinating and managing the risk pool can be complex and resource-intensive.

Regulation: Ensuring compliance with regulatory requirements and standards.

Equity Issues

Fair Distribution: Ensuring that the distribution of risks and benefits is fair and equitable.

Contribution Levels: Setting appropriate contribution levels that reflect individual risk levels without being prohibitive.

Best Practices for Implementing Risk Pooling

Implementing best practices can help effectively manage and overcome challenges, maximizing the benefits of risk pooling.

Ensure Proper Risk Assessment

Comprehensive Analysis: Conduct thorough risk assessments to identify and understand individual risks.

Risk Categorization: Categorize risks based on their nature and potential impact to facilitate pooling.

Set Appropriate Contributions

Risk-Based Contributions: Set contribution levels based on individual risk levels to ensure fairness.

Regular Reviews: Regularly review and adjust contributions to reflect changes in risk levels.

Monitor and Manage Behavior

Incentive Structures: Develop incentive structures to discourage excessive risk-taking.

Monitoring Mechanisms: Implement monitoring mechanisms to track and manage participant behavior.

Foster Transparency

Open Communication: Ensure open communication about the risk pooling process and its benefits.

Transparent Operations: Maintain transparency in the management and operation of the risk pool.

Promote Equity

Fair Distribution: Ensure that the distribution of risks and benefits is fair and equitable.

Inclusive Practices: Implement inclusive practices to ensure all participants are treated fairly.

Future Trends in Risk Pooling

Several trends are likely to shape the future of risk pooling and its applications.

Digital Transformation

Data Analytics: Leveraging data analytics to enhance risk assessment and management.

Blockchain Technology: Using blockchain for secure and transparent management of risk pools.

Collaborative Platforms

Online Platforms: Developing online platforms to facilitate risk pooling and resource sharing.

Crowdsourcing: Utilizing crowdsourcing to aggregate risks and resources from a larger community.

Sustainable Practices

Green Insurance: Promoting green insurance products that pool environmental risks.

Sustainable Investments: Creating investment pools that focus on sustainable and socially responsible projects.

Global Cooperation

International Risk Pools: Developing international risk pools to manage global risks, such as pandemics and climate change.

Cross-Border Collaboration: Enhancing cross-border collaboration to share risks and resources effectively.

Behavioral Insights

Nudge Theory: Applying nudge theory to encourage participation and responsible behavior in risk pools.

Behavioral Economics: Using insights from behavioral economics to design effective risk pooling strategies.

Conclusion

Risk pooling is a powerful strategy for managing and mitigating risks by combining the risks of multiple entities to reduce the impact of individual risks. By understanding the key components, methods, benefits, and challenges of risk pooling, organizations and individuals can develop effective strategies to enhance risk management, reduce variability, and improve overall outcomes. Implementing best practices such as ensuring proper risk assessment, setting appropriate contributions, monitoring and managing behavior, fostering transparency, and promoting equity can help maximize the benefits of risk pooling.

In a functional organizational structure, groups and teams are organized based on function. Therefore, this organization follows a top-down structure, where most decision flows from top management to bottom. Thus, the bottom of the organization mostly follows the strategy detailed by the top of the organization.

In a flat organizational structure, there is little to no middle management between employees and executives. Therefore it reduces the space between employees and executives to enable an effective communication flow within the organization, thus being faster and leaner.

Project portfolio management (PPM) is a systematic approach to selecting and managing a collection of projects aligned with organizational objectives. That is a business process of managing multiple projects which can be identified, prioritized, and managed within the organization. PPM helps organizations optimize their investments by allocating resources efficiently across all initiatives.

Harvard Business School professor Dr. John Kotter has been a thought-leader on organizational change, and he developed Kotter’s 8-step change model, which helps business managers deal with organizational change. Kotter created the 8-step model to drive organizational transformation.

The Nadler-Tushman Congruence Model was created by David Nadler and Michael Tushman at Columbia University. The Nadler-Tushman Congruence Model is a diagnostic tool that identifies problem areas within a company. In the context of business, congruence occurs when the goals of different people or interest groups coincide.

McKinsey’s Seven Degrees of Freedom for Growth is a strategy tool. Developed by partners at McKinsey and Company, the tool helps businesses understand which opportunities will contribute to expansion, and therefore it helps to prioritize those initiatives.

Mintzberg’s 5Ps of Strategy is a strategy development model that examines five different perspectives (plan, ploy, pattern, position, perspective) to develop a successful business strategy. A sixth perspective has been developed over the years, called Practice, which was created to help businesses execute their strategies.

The COSO framework is a means of designing, implementing, and evaluating control within an organization. The COSO framework’s five components are control environment, risk assessment, control activities, information and communication, and monitoring activities. As a fraud risk management tool, businesses can design, implement, and evaluate internal control procedures.

The TOWS Matrix is an acronym for Threats, Opportunities, Weaknesses, and Strengths. The matrix is a variation on the SWOT Analysis, and it seeks to address criticisms of the SWOT Analysis regarding its inability to show relationships between the various categories.

Lewin’s change management model helps businesses manage the uncertainty and resistance associated with change. Kurt Lewin, one of the first academics to focus his research on group dynamics, developed a three-stage model. He proposed that the behavior of individuals happened as a function of group behavior.

OpenAI is an artificial intelligence research laboratory that transitioned into a for-profit organization in 2019. The corporate structure is organized around two entities: OpenAI, Inc., which is a single-member Delaware LLC controlled by OpenAI non-profit, And OpenAI LP, which is a capped, for-profit organization. The OpenAI LP is governed by the board of OpenAI, Inc (the foundation), which acts as a General Partner. At the same time, Limited Partners comprise employees of the LP, some of the board members, and other investors like Reid Hoffman’s charitable foundation, Khosla Ventures, and Microsoft, the leading investor in the LP.

Airbnb follows a holacracy model, or a sort of flat organizational structure, where teams are organized for projects, to move quickly and iterate fast, thus keeping a lean and flexible approach. Airbnb also moved to a hybrid model where employees can work from anywhere and meet on a quarterly basis to plan ahead, and connect to each other.

The Amazon organizational structure is predominantly hierarchical with elements of function-based structure and geographic divisions. While Amazon started as a lean, flat organization in its early years, it transitioned into a hierarchical organization with its jobs and functions clearly defined as it scaled.

The Coca-Cola Company has a somewhat complex matrix organizational structure with geographic divisions, product divisions, business-type units, and functional groups.

Costco has a matrix organizational structure, which can simply be defined as any structure that combines two or more different types. In this case, a predominant functional structure exists with a more secondary divisional structure.

Costco’s geographic divisions reflect its strong presence in the United States combined with its expanding global presence. There are six divisions in the country alone to reflect its standing as the source of most company revenue.

Compared to competitor Walmart, for example, Costco takes more a decentralized approach to management, decision-making, and autonomy. This allows the company’s stores and divisions to more flexibly respond to local market conditions.

Dell has a functional organizational structure with some degree of decentralization. This means functional departments share information, contribute ideas to the success of the organization and have some degree of decision-making power.

eBay was until recently a multi-divisional (M-form) organization with semi-autonomous units grouped according to the services they provided. Today, eBay has a single division called Marketplace, which includes eBay and its international iterations.

Facebook is characterized by a multi-faceted matrix organizational structure. The company utilizes a flat organizational structure in combination with corporate function-based teams and product-based or geographic divisions. The flat organization structure is organized around the leadership of Mark Zuckerberg, and the key executives around him. On the other hand, the function-based teams are based on the main corporate functions (like HR, product management, investor relations, and so on).

Goldman Sachs has a hierarchical structure with a clear chain of command and defined career advancement process. The structure is also underpinned by business-type divisions and function-based groups.

Google (Alphabet) has a cross-functional (team-based) organizational structure known as a matrix structure with some degree of flatness. Over the years, as the company scaled and it became a tech giant, its organizational structure is morphing more into a centralized organization.

IBM has an organizational structure characterized by product-based divisions, enabling its strategy to develop innovative and competitive products in multiple markets. IBM is also characterized by function-based segments that support product development and innovation for each product-based division, which include Global Markets, Integrated Supply Chain, Research, Development, and Intellectual Property.

McDonald’s has a divisional organizational structure where each division – based on geographical location – is assigned operational responsibilities and strategic objectives. The main geographical divisions are the US, internationally operated markets, and international developmental licensed markets. And on the other hand, the hierarchical leadership structure is organized around regional and functional divisions.

McKinsey & Company has a decentralized organizational structure with mostly self-managing offices, committees, and employees. There are also functional groups and geographic divisions with proprietary names.

Microsoft has a product-type divisional organizational structure based on functions and engineering groups. As the company scaled over time it also became more hierarchical, however still keeping its hybrid approach between functions, engineering groups, and management.

Nestlé has a geographical divisional structure with operations segmented into five key regions. For many years, Swiss multinational food and drink company Nestlé had a complex and decentralized matrix organizational structure where its numerous brands and subsidiaries were free to operate autonomously.

Nike has a matrix organizational structure incorporating geographic divisions. Nike’s matrix structure is also present at the regional and sub-regional levels. Managerial responsibility is segmented according to business unit (apparel, footwear, and equipment) and function (human resources, finance, marketing, sales, and operations).

Patagonia has a particular organizational structure, where its founder, Chouinard, disposed of the company’s ownership in the hands of two non-profits. The Patagonia Purpose Trust, holding 100% of the voting stocks, is in charge of defining the company’s strategic direction. And the Holdfast Collective, a non-profit, holds 100% of non-voting stocks, aiming to re-invest the brand’s dividends into environmental causes.

Samsung has a product-type divisional organizational structure where products determine how resources and business operations are categorized. The main resources around which Samsung’s corporate structure is organized are consumer electronics, IT, and device solutions. In addition, Samsung leadership functions are organized around a few career levels grades, based on experience (assistant, professional, senior professional, and principal professional).

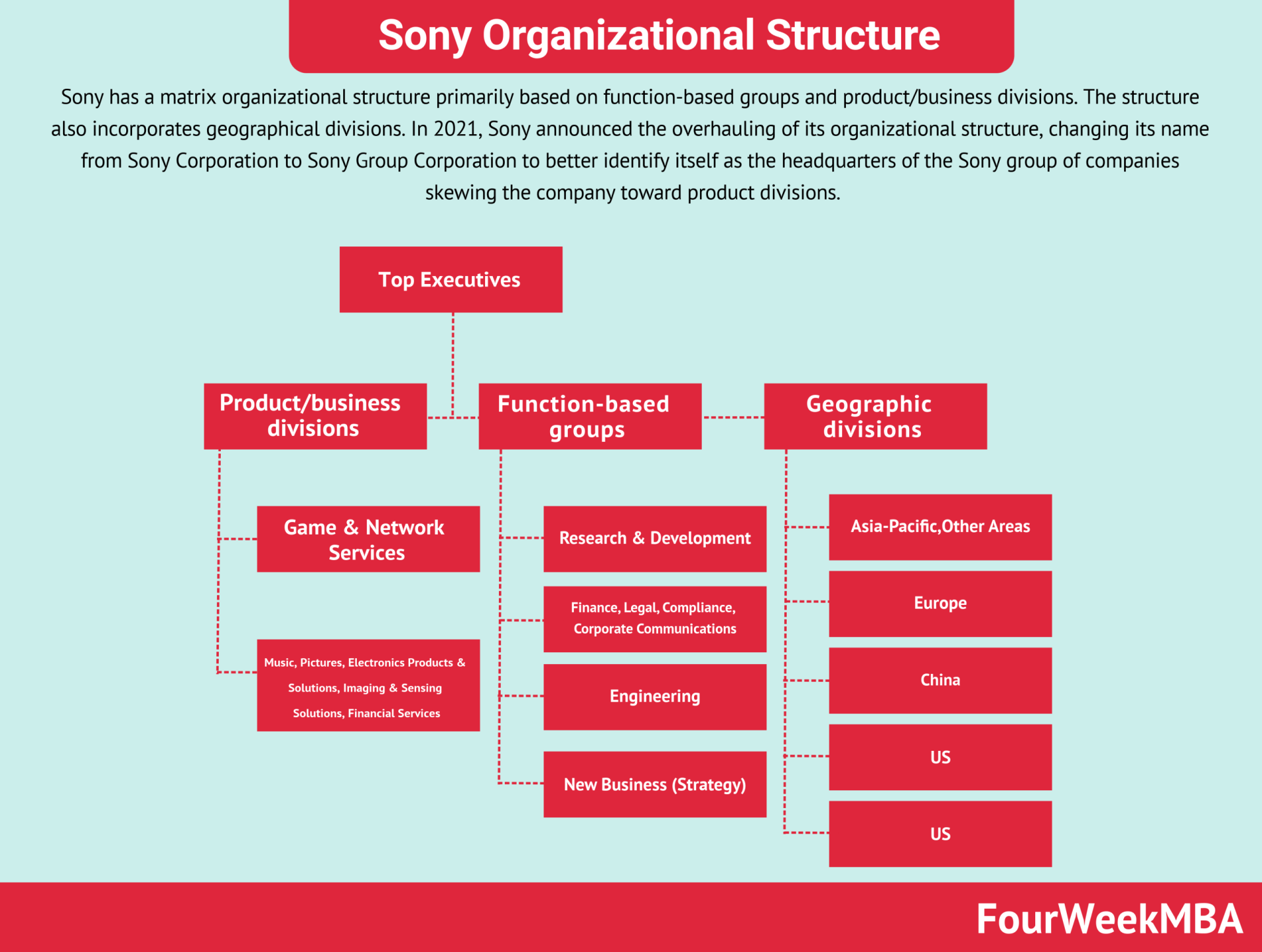

Sony has a matrix organizational structure primarily based on function-based groups and product/business divisions. The structure also incorporates geographical divisions. In 2021, Sony announced the overhauling of its organizational structure, changing its name from Sony Corporation to Sony Group Corporation to better identify itself as the headquarters of the Sony group of companies skewing the company toward product divisions.

Starbucks follows a matrix organizational structure with a combination of vertical and horizontal structures. It is characterized by multiple, overlapping chains of command and divisions.

Tesla is characterized by a functional organizational structure with aspects of a hierarchical structure. Tesla does employ functional centers that cover all business activities, including finance, sales, marketing, technology, engineering, design, and the offices of the CEO and chairperson. Tesla’s headquarters in Austin, Texas, decide the strategic direction of the company, with international operations given little autonomy.

Toyota has a divisional organizational structure where business operations are centered around the market, product, and geographic groups. Therefore, Toyota organizes its corporate structure around global hierarchies (most strategic decisions come from Japan’s headquarter), product-based divisions (where the organization is broken down, based on each product line), and geographical divisions (according to the geographical areas under management).

Walmart has a hybrid hierarchical-functional organizational structure, otherwise referred to as a matrix structure that combines multiple approaches. On the one hand, Walmart follows a hierarchical structure, where the current CEO Doug McMillon is the only employee without a direct superior, and directives are sent from top-level management. On the other hand, the function-based structure of Walmart is used to categorize employees according to their particular skills and experience.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.