Resource planning is identifying, estimating, and scheduling resources needed to complete a project. It involves analyzing the scope of the project, determining what resources are required, and then efficiently allocating those resources. This includes assessing the availability of personnel, materials, equipment, and other resources necessary for the successful completion of the project.

| Aspect | Explanation |

|---|---|

| Definition | Resource Management is the process of efficiently and effectively planning, allocating, and utilizing an organization’s or project’s resources to achieve specific goals and objectives. It encompasses various assets, including human resources, financial resources, equipment, time, and materials, and involves optimizing their allocation to maximize productivity and minimize waste. Effective resource management is essential for ensuring the success and sustainability of organizations and projects. |

| Key Concepts | – Resource Allocation: The process of assigning available resources to specific tasks, projects, or activities based on priority and need. – Resource Optimization: Ensuring that resources are used efficiently to maximize output and minimize costs. – Capacity Planning: Identifying and planning for future resource needs to meet organizational objectives. – Resource Tracking: Monitoring and managing the usage of resources throughout their lifecycle. – Resource Constraints: Recognizing limitations in resources and finding ways to work within those constraints. |

| Characteristics | – Efficiency: Resource management aims to use resources optimally, reducing waste and inefficiency. – Strategic Planning: It involves aligning resource allocation with strategic goals and objectives. – Flexibility: Resource management adapts to changing needs and priorities. – Resource Tracking: Monitoring and evaluating resource usage in real-time to make informed decisions. – Cost Control: Managing costs associated with resource acquisition and utilization. |

| Implications | – Cost Reduction: Effective resource management can lead to cost savings by eliminating unnecessary expenses and optimizing resource usage. – Improved Productivity: Proper allocation of resources can boost productivity and output. – Strategic Advantage: Organizations that excel in resource management gain a competitive edge by efficiently utilizing their resources. – Risk Mitigation: Resource management helps identify and address potential resource shortages or bottlenecks that could jeopardize project or organizational goals. – Sustainability: Sustainable resource management practices contribute to environmental responsibility and long-term viability. |

| Advantages | – Efficiency: Efficient resource management reduces waste and ensures resources are used effectively. – Cost Savings: It leads to cost reduction by eliminating unnecessary expenses. – Improved Productivity: Optimized resource allocation enhances productivity and output. – Strategic Alignment: Resource management aligns resource allocation with organizational objectives. – Competitive Edge: Organizations that excel in resource management gain a competitive advantage. |

| Drawbacks | – Complexity: Resource management can be complex, particularly in large organizations or projects with diverse resource needs. – Resource Constraints: Limited resources can pose challenges in meeting all demands and priorities. – Technological Dependencies: Reliance on technology for resource tracking and allocation may introduce vulnerabilities. – Resistance to Change: Implementing resource management processes may face resistance from employees accustomed to existing practices. – Risk of Overallocation: Poor resource management can lead to overallocation of resources, resulting in burnout or inefficiency. |

| Applications | – Project Management: Resource management is critical in project planning to allocate personnel, time, and materials effectively. – Human Resource Management: Ensuring the right people with the right skills are in the right roles. – Financial Management: Managing budgets and financial resources to meet strategic objectives. – Supply Chain Management: Optimizing the flow of materials and products within supply chains. – Asset Management: Tracking and maintaining physical assets such as equipment and facilities. |

Resource Planning

Identifying Resources

The first step in resource planning is to identify all available resources that can be used for a given project.

This includes personnel such as team members or contractors who will be working on the project; materials such as raw materials or supplies; equipment such as compute — as explored in the economics of AI compute infrastructure — rs or tools; and any other relevant assets that may be needed to get the job done.

Estimating Resource Requirements

Once you have identified all available resources it’s important to estimate how much of each resource will be needed for your particular project.

For example if you need 10 people working on a task then you should estimate how many hours they will need to work per day/week/month etc., so that you can plan accordingly.

You should also consider factors like cost when estimating resource requirements so that you don’t overspend on unnecessary items or services.

After estimating your resource requirements, it’s time to schedule them appropriately so that tasks are completed within deadlines and budgets are not exceeded.

Scheduling requires careful consideration of timelines, dependencies between tasks (e.g., one task must finish before another can begin), holidays or peak times when certain tasks cannot be completed due to lack of staff availability etc., thus it is important to take these into account when creating schedules for projects with multiple components and stakeholders involved in order ensure success overall.

Resource planning is a crucial part of project management in any startup, and it requires careful consideration of the resources available to ensure successful execution.

With proper resource planning, you can effectively allocate your resources and optimize their use for maximum efficiency. Next up: Scheduling Resources.

Resource Allocation

Resource allocation is the process of assigning available resources to tasks in order to achieve project objectives.

This involves prioritizing tasks based on importance and urgency, assigning personnel or other resources to each task, and monitoring progress and performance against established goals.

Prioritizing Tasks

Prioritizing tasks helps ensure that the most important activities are completed first.

It also allows for better resource utilization by focusing efforts on those activities with the highest return on investment (ROI).

When prioritizing tasks, it’s important to consider factors such as timeline, cost, risk level, complexity of work involved and any dependencies between tasks.

Assigning Resources To Tasks

Once priorities have been established, resources can be assigned accordingly.

This includes personnel as well as equipment or materials needed for completion of a task.

It’s important to consider skillset when making assignments so that team members are able to complete their assigned duties efficiently and effectively.

After assigning resources, it is essential to monitor progress regularly in order to identify potential issues early on before they become major problems later.

Monitoring should include tracking milestones achieved along with budget spent versus allocated budget, as well as any changes made during the execution phase which may affect the overall outcome of project objectives set at the beginning stage of planning process.

Resource allocation is an essential part of project management and should be carefully monitored to ensure the successful completion of projects. The next heading will focus on monitoring progress and performance.

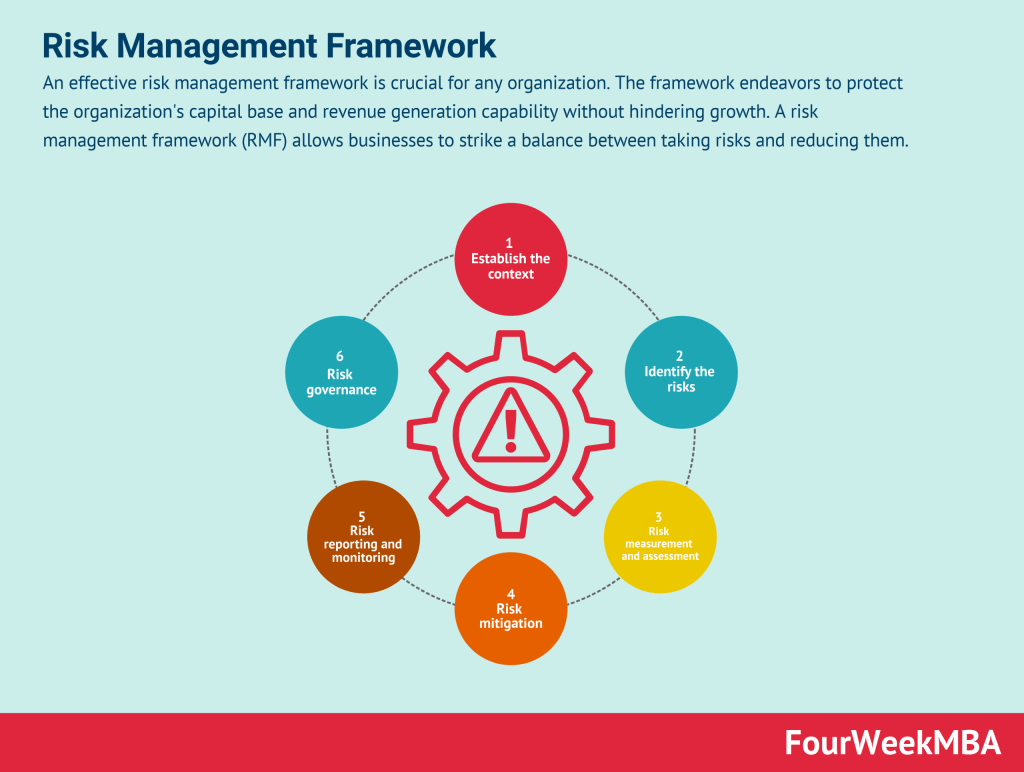

Risk Management

Risk management is an important part of any project plan. It helps identify potential risks that could affect the success of a project and develop strategies for mitigating them.

Identifying risks and mitigation strategies involves assessing each task or activity within a project to determine what potential issues may arise, then developing plans to address those issues if they occur.

This includes researching possible solutions, creating contingency plans in case something goes wrong, and determining how resources can be allocated to minimize risk exposure.

Developing contingency plans is essential for managing risk effectively.

These plans should outline specific steps that will be taken in the event of an unexpected issue arising during implementation, such as additional resources being needed or changes needing to be made to existing processes.

Tracking risk status throughout the duration of the project is also important; this ensures that any issues are identified quickly so corrective action can be taken promptly before it has too much impact on progress or performance.

Finally, reporting any issues that arise during implementation allows stakeholders to stay informed about potential risks and take appropriate measures when necessary.

Resource allocation plays an important role in minimizing risk exposure as well; prioritizing tasks according to their importance and assigning resources accordingly helps ensure projects are completed efficiently with minimal disruption from unforeseen events or delays due to lack of resources.

Monitoring progress and performance regularly also helps identify areas where improvements can be made before they become major problems down the line.

Quality assurance management is another key component of successful risk management; setting quality standards and goals gives teams clear objectives for measuring success while evaluating performance against these standards provides insight into how well projects are progressing relative to expectations set at the outset.

Implementing corrective actions when necessary further reduces chances of failure by ensuring all tasks meet established criteria before moving forward with implementation stages like testing or deployment phases.

Risk management is an essential part of any successful project, and it’s important to ensure that risks are identified and managed effectively. Now let’s look at how to develop effective contingency plans for unexpected events.

Communication Management

Communication management is an essential part of any successful project. Establishing communication channels and protocols between team members, stakeholders, and other relevant parties helps ensure that everyone is kept informed about progress and changes during implementation.

This includes setting up a system for sharing information such as emails, video conferences, or instant messaging platforms.

Additionally, it’s important to have clear expectations for when and how each party should communicate with one another so that everyone can stay on the same page throughout the duration of the project.

Facilitating collaboration among team members is also key in ensuring success.

This involves creating an environment where all participants feel comfortable voicing their opinions while respecting those of others. It’s important to encourage open dialogue between all involved parties in order to foster creativity and innovation within the group which will ultimately lead to better results for the project at hand.

Finally, managing conflict resolution processes when disagreements arise between stakeholders or team members is necessary in order to keep progress moving forward towards completion of the project.

This requires having a plan in place beforehand on how disputes should be handled as well as being prepared with strategies for resolving them quickly and efficiently without compromising quality standards or goals set out by management prior to beginning work on the project itself.

Communication Management is essential for successful project management within a startup.

The next heading will focus on resource management and how to best utilize resources for optimal results.

Quality Assurance Management

Quality assurance management is a key component of any successful project.

It involves setting quality standards and goals at the beginning of a project, evaluating performance against these standards throughout its duration, and implementing corrective actions when necessary in order to maintain high levels of quality throughout its life cycle.

Setting Quality Standards and Goals

The first step in quality assurance management is establishing clear expectations for the project’s deliverables.

This includes defining what constitutes acceptable results, as well as outlining criteria for measuring success or failure.

These standards should be realistic yet challenging enough to ensure that all stakeholders are held accountable for their contributions to the overall outcome.

Evaluating Performance Against Standards and Goals

Once established, it’s important to regularly evaluate performance against these standards throughout the course of the project.

This can include conducting regular reviews with team members or customers, analyzing data from surveys or tests, or simply keeping an eye on progress towards meeting deadlines and other milestones set out during planning stages.

Doing so will help identify potential issues early on before they become major problems down the line.

If discrepancies between actual results and expected outcomes are identified through evaluation processes outlined above, then corrective action must be taken in order to get back on track towards achieving desired goals within budget constraints while maintaining high levels of quality across all deliverables produced by the team over time.

This could involve making changes to existing procedures or processes; providing additional training; introducing new tools or technologies; revising timelines; reallocating resources; etc., depending on what has been identified as being necessary in order to bring about improvement where required most urgently.

Quality Assurance Management is a crucial part of any project, as it helps ensure that the desired results are achieved. Next, we will look at how to plan and manage resources effectively.

What are the three types of resource management?

Human Resource Management

This involves managing the people involved in a project, including recruiting and training personnel, assigning tasks, evaluating performance, and providing feedback.

Financial Resource Management

This involves budgeting for projects, tracking expenses and revenue associated with the project, monitoring cash flow to ensure sufficient funds are available to complete the project on time and within budget.

Material Resource Management

This involves procuring materials needed for a project such as raw materials or equipment that is necessary for completion of the work at hand.

It also includes ensuring proper storage of these resources until they are needed during implementation of the project plan.

What are the five elements of resource management?

Planning

This involves setting objectives, developing strategies and creating a timeline for the project.

Scheduling

Establishing deadlines and assigning tasks to team members based on their availability and skill set.

Budgeting

Allocating resources within the given budget to ensure that all necessary activities are completed in a timely manner without exceeding the allocated funds.

Monitoring & Control

Keeping track of progress, identifying potential issues or risks, and taking corrective action when needed to stay on schedule and within budget limits.

Reporting & Documentation

Creating reports that provide an overview of project performance including cost analysis, timeline updates, resource utilization data etc., as well as maintaining accurate records for future reference or audit purposes if required by stakeholders or clients

Key takeaways

In conclusion, resource management is an essential part of project management within a startup.

It involves planning and allocating resources to ensure the successful completion of projects while managing risks and ensuring quality assurance.

Effective communication is also key in order to ensure that all stakeholders are on the same page throughout the entire process.

By taking these steps, startups can be better equipped to grow and succeed in their respective markets.

Key Highlights

- Resource Planning:

- Identifying, estimating, and scheduling resources for project completion.

- Analyzing project scope and allocating resources efficiently.

- Includes personnel, materials, equipment, and other necessities.

- Resource Allocation:

- Assigning resources to tasks based on priority and urgency.

- Prioritizing tasks for better resource utilization.

- Monitoring progress and performance against goals.

- Risk Management:

- Identifying potential project risks and developing mitigation strategies.

- Assessing tasks, creating contingency plans, and tracking risk status.

- Implementing corrective actions to reduce disruptions.

- Communication Management:

- Establishing communication channels among team members and stakeholders.

- Encouraging open dialogue, collaboration, and conflict resolution.

- Keeping all parties informed and aligned throughout the project.

- Quality Assurance Management:

- Setting quality standards and goals for project deliverables.

- Evaluating performance against standards and goals regularly.

- Implementing corrective actions to maintain high quality.

- Three Types of Resource Management:

- Human Resource Management: Involves personnel management, training, and performance evaluation.

- Financial Resource Management: Focuses on budgeting, expense tracking, and revenue monitoring.

- Material Resource Management: Includes procurement and storage of necessary materials.

- Five Elements of Resource Management:

- Planning: Setting objectives, strategies, and timelines.

- Scheduling: Assigning tasks and deadlines based on team availability.

- Budgeting: Allocating resources within budget constraints.

- Monitoring & Control: Tracking progress and addressing issues.

- Reporting & Documentation: Creating reports and maintaining records.

Read Next: Portfolio Management, Program Management, Product Management, Project Management.

FourWeekMBA Business Toolbox

Asymmetric Betting

Other business resources:

- What Is Business Model Innovation

- What Is a Business Model

- What Is Business Strategy

- What is Blitzscaling

- What Is Market Segmentation

- What Is a Marketing Strategy

- What is Growth Hacking