The AI Gold Rush Has a Fatal Flaw: Every Prospector Uses the Same Pickaxe

While Silicon Valley celebrates the AI revolution, the entire industry has quietly painted itself into a corner that would make any risk manager’s blood run cold. Every major AI company—from NVIDIA’s GPU dominance to Google’s TPU ambitions—depends on a single manufacturer located on a geopolitically volatile island 100 miles from mainland China.

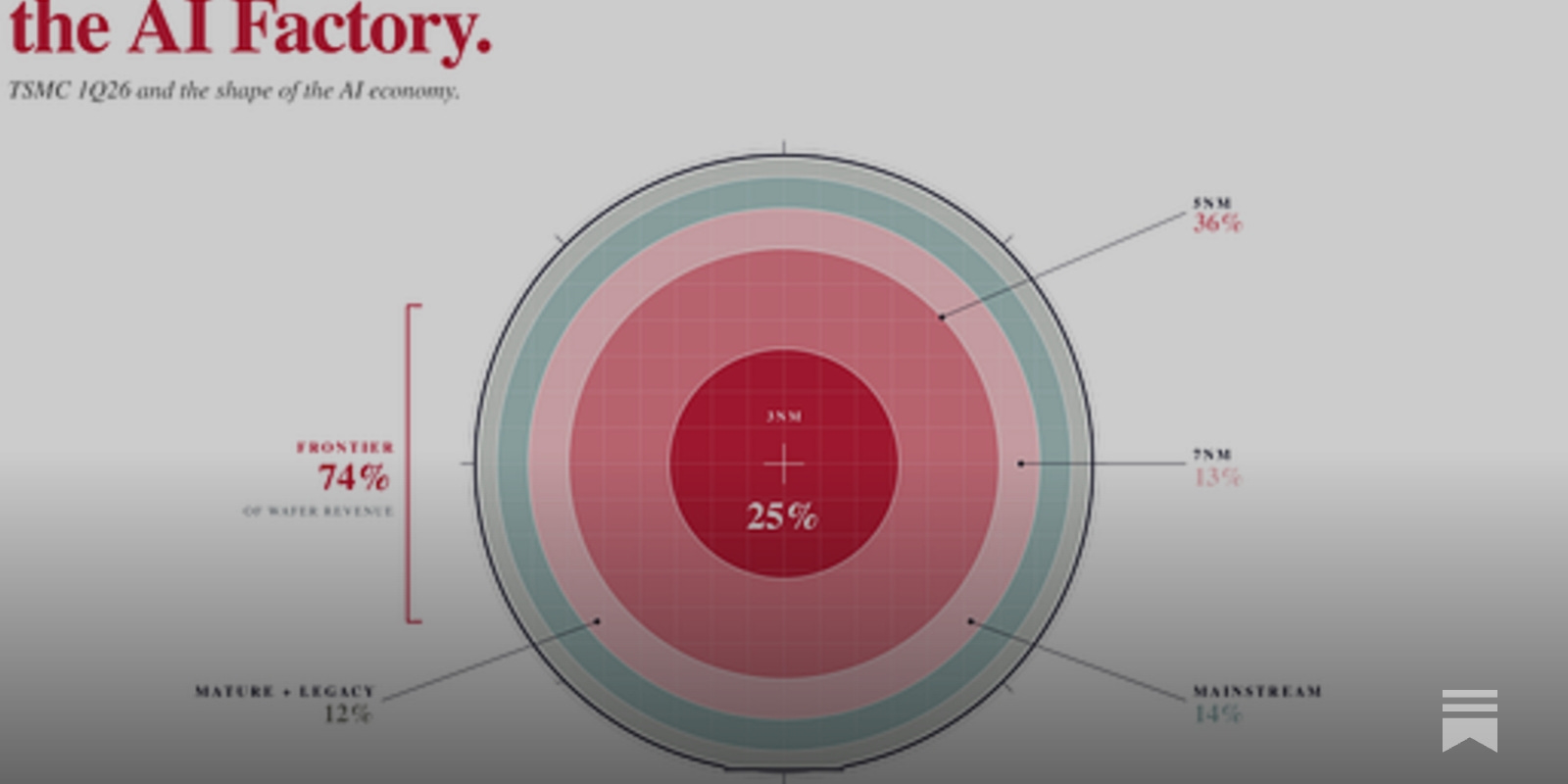

Taiwan Semiconductor Manufacturing Company doesn’t just make chips; it holds the AI economy hostage. With 74% of TSMC’s wafers now at 7nm or below—the precise manufacturing nodes required for cutting-edge AI processors—the company has become an unavoidable chokepoint. High-performance computing, which includes AI chips, now represents a staggering 61% of TSMC’s total revenue, up from practically nothing a decade ago.

Source: The Business Engineer

The dependency web is breathtaking in its scope. NVIDIA’s H100 chips, the workhorses powering ChatGPT and most large language model — as explored in the intelligence factory race between AI labs — s, roll off TSMC production lines. Google’s custom TPU chips that give the company its AI edge? TSMC. Apple’s Neural Engine processors that enable on-device AI features? TSMC. Qualcomm’s latest AI-optimized mobile chips? Also TSMC.

This isn’t just market concentration—it’s strategic recklessness disguised as efficiency. Intel, once the undisputed king of semiconductors, now finds itself scrambling to rebuild domestic manufacturing capabilities through its foundry services, but currently lacks the advanced process technology to compete at the bleeding edge. Samsung Foundry, TSMC’s closest rival, produces roughly 20% of the world’s contract semiconductors compared to TSMC’s commanding 60% market share, and struggles particularly with yield rates on advanced nodes.

The numbers reveal an industry sleepwalking toward systemic risk. TSMC’s advanced packaging revenue—critical for AI chip performance—jumped 20% year-over-year, while the company’s capex spending hit $36 billion in 2023, mostly focused on expanding 3nm and 2nm capacity. These investments lock in TSMC’s technological lead for the next five years, meaning AI companies have no viable alternative even if they wanted one.

Consider the absurdity: Amazon Web Services and Microsoft Azure, bitter cloud computing rivals, both depend on the same Taiwanese fab for their AI acceleration chips. If TSMC’s operations faced disruption—whether from natural disaster, geopolitical conflict, or supply chain crisis—both companies would simultaneously lose their competitive advantage. It’s like Coca-Cola and Pepsi sourcing their secret formulas from the same supplier.

The AI industry’s TSMC dependency creates a unique form of systemic risk that traditional business models never anticipated. Unlike software, where companies can pivot quickly, semiconductor manufacturing requires years-long development cycles and billions in capital investment. TSMC’s 92% gross margin on advanced nodes reflects not just technological superiority, but the absence of meaningful competition.

Smart money should be positioning for the inevitable correction. Within 18 months, we’ll see the first major AI company announce a significant diversification strategy away from TSMC—likely through massive investments in Intel’s foundry services or emergency partnerships with Samsung. The company that moves first to reduce TSMC dependency won’t just survive the next supply shock; they’ll gain permanent strategic advantage while competitors remain trapped in Taiwan’s shadow. The AI revolution’s next chapter won’t be written by whoever builds the smartest algorithms, but by whoever secures the most resilient supply chain.

How AI Is Reshaping This Business Model

AI is fundamentally reshaping the semiconductor fabrication industry by creating unprecedented demand concentration that exposes critical vulnerabilities in global chip supply chains. TSMC’s dominance in advanced node manufacturing—controlling over 90% of chips below 10 nanometers—has become both more valuable and more precarious as AI workloads drive exponential growth in high-performance processor requirements.

The AI boom has transformed TSMC from a traditional contract manufacturer into the singular chokepoint for the entire artificial intelligence ecosystem. Companies like NVIDIA, which saw AI chip revenues surge from $3 billion to over $60 billion annually, depend entirely on TSMC’s 4nm and 3nm processes for their most advanced GPUs. This dependency extends beyond hardware manufacturers to every AI company building large language models, autonomous vehicles, or machine learning platforms.

This concentration creates a cascading risk structure where geopolitical tensions, natural disasters, or operational disruptions at TSMC could simultaneously cripple OpenAI’s infrastructure — as explored in the economics of AI compute infrastructure — , Tesla’s autonomous driving capabilities, and Google’s AI services. The company’s monopolistic position in cutting-edge fabrication means that AI innovation timelines, scaling capabilities, and competitive advantages across the entire industry now hinge on a single facility’s capacity and stability. As AI computational demands continue growing exponentially, this dependency will only intensify, making supply chain diversification the defining strategic challenge for the next decade.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

Scroll to Top

Discover more from FourWeekMBA

Subscribe now to keep reading and get access to the full archive.