I read an interesting article about the sudden move of Wall Street Quant Traders from banks to creating tech startups.

In short, as the story goes, to prevent breaking non-compete agreements, many brilliant minds were moving in – what seemed – completely unrelated fields, like self-driving or robotics.

In other words, a built-in disincentive by Wall Street is creating whole new industries, which might be completely unrelated in the short term but that might become competitors in the long run.

It struck me how the system’s built-in disincentives trying to stiff competition – in the short-term – actually create whole new markets in the long term. In this case, intelligent people move to new industries to prevent legal issues.

And when assessing long-term competition, it’s vital to look at the sudden moves of very skilled and intelligent people.

In other words, competition in the tech industry is linear in short but pretty much non-linear in the long.

New industries that might seem unrelated might swallow old industries in the long.

Another example I like a lot is when innovative players (those who see the market as a whole without clear boundaries) enter new spaces.

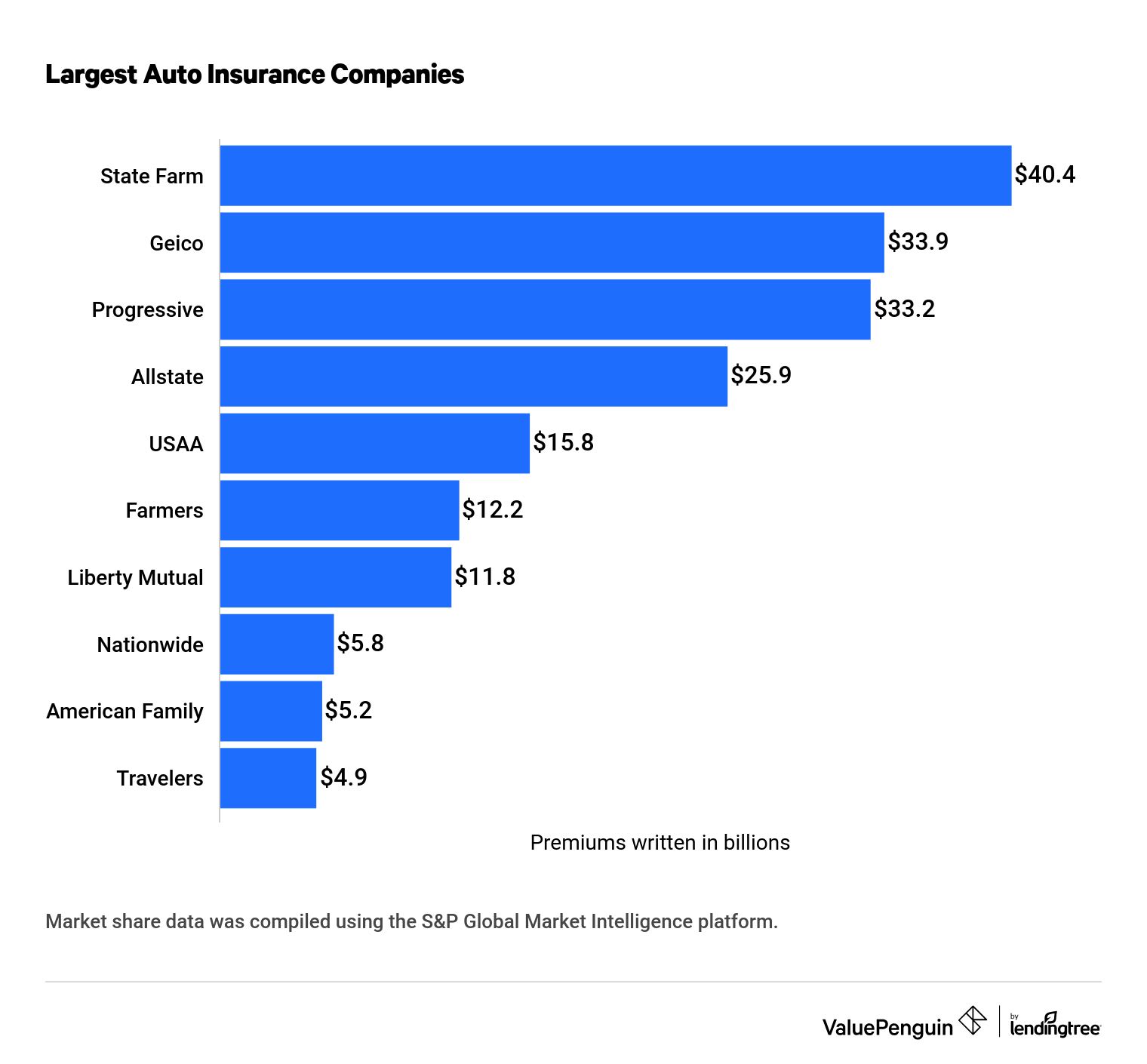

Take the case of Tesla, entering into the insurance business.

Would you even put Tesla on the competitor’s map if you were Geico?

Chances are, you won’t, and probably you won’t do that because competition seems linear in the short term.

Thus, your competition might look like the following graph:

There is also another interesting point to make.

When you look at Tesla’s insurance business, you know that, for now, it’s part of the service business, but you’re not sure how much it generates for the company.

Indeed, in 2021, the service business generated $3.8 billion in revenues for Tesla, and we can assume that the insurance arm drove a good chunk of its growth!

Thus, it might be too late when we finally have accurate data about the Tesla insurance business revenues and, most importantly, margins.

Take another case, that of Amazon, which left everyone flabbergasted, when it showed its AWS numbers, in 2016:

When Amazon opened up its AWS numbers (as they had to comply with SEC’s requirements), AWS was the fastest growing segment, speeding up at a double-digit rate of growth per year.

For instance, when Amazon finally shared the data for AWS, it had already become a giant in the cloud space, and companies like Google and Microsoft had to rush and ramp up their cloud operations to keep up!

It was also becoming more profitable than Amazon’s core business!

Keep in mind that executives in the industry, who were well positioned to see this coming, didn’t see it!

Interviewed by Charlie Rose in October 2014 (when AWS was already generating over $4 billion in revenues), asked about what he thought of Amazon AWS, former Microsoft CEO Steve Ballm — as explored in the intelligence factory race between AI labs — er said:

“They make no money, Charlie! In my world, you’re not a real business until you make some money!”

It’s, of course, too easy to pick on Steve Ballmer, but you get the point.

He completely missed the fact that not only AWS was making money, but it was also making it at wide margins, actually, higher margins than the core Amazon business!

Therefore, good businesses are often hidden and hard to predict, and when you realize it might be too late, the time window to catch up might be very, very tight!

To sum things up:

1. Competition seems linear only in the short term.

Indeed, while you might be able as a dominant player to stiff competition in the short term, your future competitor might come from an unexpected place.

Take the case of Tesla entering the insurance business.

If you were a traditional insurance player, like Geico, operating since 1936, would you even place Tesla on your competitors’ map?

When looking at the business world, you want to keep an open eye on what niches are developing, which might, non-linearly, develop as take-all industries!

2. One way is to look at where highly skilled people are moving to.

3. Another way is to look at built-in disincentives in large, existing industries and what other sectors these incentives are making emerge.

4. The last and critical point. In the long-term – what in the short term seemed an utterly unrelated industry – might end up becoming larger and eat you up!

How do you prevent that?

Keep an open eye on the few data points that matter.

If you were Steve Ballmer in 2014, instead of laughing at Amazon AWS, you would have sent around some of your key people to ask what startups were building their business on top of Amazon AWS.

You would have figured out that upstarts – at the time – like Netflix had been migrating their whole infrastructure — as explored in the economics of AI compute infrastructure — s on AWS.

Netflix completed the full migration to the AWS cloud in 2016 when it became way more expensive for Microsoft to pick up (even though it did manage to gain traction through Microsoft Azure, it might have been way cheaper if it had acted before).

Key Highlights

- Built-In Disincentives Creating New Industries: Wall Street’s built-in disincentives can lead to the creation of entirely new industries by pushing skilled individuals to explore unrelated fields, such as self-driving cars or robotics.

- Competition in Tech Industry: Competition in the tech industry may appear linear in the short term but is non-linear in the long term. New industries that seem unrelated at first can eventually disrupt and overtake existing ones.

- Tesla’s Entry into Insurance: Tesla’s move into the insurance business, initially seen as unrelated to its core automotive business, is an example of how innovative players can enter new spaces and disrupt traditional industries.

- Importance of Data: Data plays a crucial role in understanding emerging trends and competitors in the market. Traditional players must keep an eye on data points that matter to stay competitive.

- Amazon’s AWS Success: Amazon’s AWS (Amazon Web Services) initially went unnoticed by industry insiders, but it became a dominant and highly profitable player in the cloud computing market, surprising many.

- Unpredictability of Good Businesses: Identifying successful businesses can be challenging and often hidden until it’s too late for competitors to catch up. Therefore, it’s essential to stay vigilant and adapt to emerging trends.

- Long-Term vs. Short-Term Competition: While dominant players may appear to stifle competition in the short term, unexpected challengers can emerge from unrelated industries in the long run, reshaping the competitive landscape.

- Following Highly Skilled Individuals: Tracking where highly skilled individuals are moving can provide insights into emerging industries and potential disruptors.

- Built-In Disincentives: Examining built-in disincentives within established industries can reveal emerging sectors driven by these incentives.

- Constant Vigilance: To prevent being overtaken by seemingly unrelated industries, businesses must remain vigilant and adapt to changing landscapes.

- Importance of Data Points: Focusing on key data points can help identify emerging trends and potential threats to traditional businesses.

- Learning from History: The example of Amazon AWS shows that successful businesses can be easily missed, emphasizing the importance of learning from history and staying open to new possibilities.

Additional Case Studies

- Amazon AWS (Amazon Web Services): As mentioned earlier, Amazon AWS entered the cloud computing market and became a dominant player, even though it was initially seen as unrelated to Amazon’s core e-commerce business. It disrupted traditional IT infrastructure providers and reshaped the cloud computing industry.

- Tesla’s Entry into Energy: Tesla, primarily known for electric vehicles, ventured into the energy sector with products like the Powerwall and solar panels. By integrating energy storage and renewable energy solutions, Tesla disrupted traditional energy companies and created new market opportunities.

- Google’s Diversification: While Google’s core business is search and advertising, the company has expanded into various unrelated areas, including autonomous vehicles (Waymo), life sciences (Verily), and smart home devices (Nest). These ventures position Google in diverse markets, potentially disrupting industries beyond its initial scope.

- Apple’s Expansion into Wearables: Apple, originally known for its computers and later iPhones, entered the wearables market with products like the Apple Watch and AirPods. The success of these wearables has made Apple a dominant player in the health and fitness tech space.

- Facebook’s Acquisition of Oculus: Facebook, a social media giant, acquired Oculus, a virtual reality (VR) company. This move allowed Facebook to enter the VR market, creating new opportunities in areas like VR gaming, communication, and virtual experiences.

- IBM’s Transition to Services: IBM, once known for its hardware products like mainframes, shifted its focus to services and consulting. This transition allowed IBM to remain relevant in the tech industry and provide a wide range of solutions beyond hardware.

- Netflix and Content Production: Netflix started as a DVD rental service and later transitioned into a streaming platform. Beyond streaming, Netflix began producing its original content, becoming a major player in the entertainment industry and challenging traditional studios and networks.

- Microsoft’s Azure Cloud: Microsoft, a software giant, entered the cloud computing market with Azure. While its core business remains software (Windows and Office), Azure has become a significant revenue driver, competing with Amazon AWS in the cloud space.

- SpaceX’s Satellite Internet: SpaceX, founded by Elon Musk, initially focused on space exploration. However, with the Starlink project, SpaceX entered the satellite internet market, aiming to provide high-speed internet access globally, disrupting traditional internet service providers.

- Alphabet’s Healthcare Ventures: Alphabet, Google’s parent company, has invested in healthcare initiatives such as Verily (life sciences) and Calico (aging research). These ventures aim to address health-related challenges and explore new opportunities in the healthcare sector.

Read Next: Business Model.

Related Business Concepts