Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Elements

Analysis

Implications

Examples

Peer-to-Peer Payments

Venmo offers a peer-to-peer (P2P) payment platform that allows users to send money to friends and family quickly and easily through their mobile devices.

Facilitates convenient and secure money transfers between individuals. Enhances social interactions and eliminates the need for cash transactions. Attracts a user base looking for P2P payment solutions.

Users can send money to friends for shared expenses, such as dining, entertainment, or rent, using the Venmo app, making transactions simple and cashless.

Mobile Payment App

Venmo operates primarily as a mobile payment app, available for iOS and Android devices. Users link their bank accounts or credit/debit cards to Venmo for seamless transactions.

Provides users with a convenient and accessible payment tool on their smartphones. Enables easy integration with existing financial accounts. Encourages mobile-first payment behavior.

Users can download the Venmo app, link their preferred payment methods, and use it to make payments, split bills, or request money from their contacts, all from their mobile devices.

Social Integration

Venmo incorporates a social feed feature that allows users to share their transactions and interact with friends by adding comments and emojis. The social aspect adds an element of fun and engagement to payments.

Enhances the user experience by making payments a social activity. Drives user engagement and encourages regular app usage. Creates network effects as users invite friends to join Venmo.

Users can see their friends’ transactions and leave comments or emojis on payments in their Venmo feed, making payments more interactive and enjoyable.

Payment Card

Venmo offers a physical payment card, known as the Venmo Debit Card, which is linked to users’ Venmo accounts and allows them to make purchases at physical stores and withdraw cash from ATMs.

Expands Venmo’s usability beyond digital transactions to physical retail locations. Provides a physical representation of the digital wallet. Encourages users to use Venmo for everyday spending.

Users can request and use the Venmo Debit Card for in-store purchases and cash withdrawals, making their Venmo balance accessible in the physical world.

Business Partnerships

Venmo partners with various businesses to enable users to make payments within popular apps and websites. These partnerships enhance Venmo’s ecosystem and extend its reach to e-commerce and other industries.

Increases Venmo’s utility by allowing users to make payments within partner apps and websites. Drives adoption and usage among partner businesses’ customer bases. Boosts Venmo’s transaction volume.

Users can use Venmo to pay for services and products within partner apps and websites, such as Uber, Grubhub, and many online retailers.

In-App Purchases

Venmo allows users to shop and pay for products directly within the app through partnerships with e-commerce platforms. Users can discover and buy items, making the app a shopping and payment hub.

Expands Venmo’s offerings to include shopping capabilities, creating a comprehensive financial ecosystem. Increases user engagement by providing a one-stop solution for payments and shopping.

Users can browse and buy products from various merchants within the Venmo app, making payments for online shopping more convenient.

Value Proposition

Venmo’s value proposition centers on providing users with a user-friendly and social P2P payment platform that simplifies money transfers, enhances social interactions, and offers additional financial services such as in-app shopping and the Venmo Debit Card.

Offers users a convenient, social, and comprehensive financial solution for P2P payments and more. Enhances the ease of money transfers and provides a seamless integration of social and financial activities.

Customer Segments

Venmo serves a wide range of customer segments, including individuals who want a convenient P2P payment solution, social users looking to engage with friends through payments, and shoppers who seek an integrated payment and shopping experience.

Addresses the diverse needs and preferences of users seeking a mobile payment app with various features. Captures a user base interested in social interactions, mobile payments, and digital shopping.

Distribution Strategy

Venmo distributes its services primarily through mobile app stores, making the app accessible to iOS and Android users. The Venmo Debit Card is distributed physically, while partnerships with businesses expand its reach further.

Ensures widespread accessibility to the Venmo app through mobile devices. The Venmo Debit Card is physically distributed to users. Partnerships with businesses enable in-app and online payments.

Competitive Advantage

Venmo’s competitive advantage lies in its user-friendly mobile app, social payment features, seamless integration of payment and shopping, and a strong user base. Venmo’s focus on social engagement sets it apart in the P2P payment industry.

Offers a distinct social payment experience that appeals to users seeking both convenience and social interaction. Leverages a strong user base and strategic partnerships to maintain competitiveness.

Today Venmo is part of the PayPal ecosystem. In fact, PayPal was acquired by eBay in 2002, ever since it started an acquisition campaign of several brands, including Braintree (in 2013).

For PayPal expanding its product line has been a critical move. Thus, Venmo has directly contributed to PayPal’s growth in the last years.

Within PayPal “Payments Platform” there are combined payment solutions, like PayPal, PayPal Credit, Braintree, Venmo, Xoom, and iZettle products.

Venmo generates revenue through transaction fees. While most free-to-use mobile apps turn to advertisements for revenue purposes, Venmo has managed to avoid this path.

In a way, Venmo can afford to be free as part of the PayPal ecosystem. In fact, Venmo is the mobile app that allows PayPal to enter a market, those of the millennials.

After several complaints about how the company handled privacy disclosures, there was a settlement with PayPal, as reported by Tech Crunch.

As claimed by Venmo in terms of security, “Your personal and financial data is encrypted and protected on our secure servers to guard against unauthorized transactions.”

As of 2017, the person-to-person transactions (P2P) represented an important growth driver for PayPal. In fact, as specified in the 2017 annual report:

Transaction revenues grew more slowly than both TPV and number of payment transactions in 2017 due primarily to a higher proportion of person-to-person (“P2P”) transactions, primarily from our PayPal and Venmo products from which we earn lower rates and foreign exchange hedging losses. The percentage growth in transaction revenues was lower than the percentage growth in TPV and payment transactions in 2016 primarily due to a higher proportion of P2P transactions (including our Venmo products) for which we earn lower rates, and a higher portion of TPV generated by large merchants who generally pay lower rates with higher transaction volume. The impact of increases or decreases in prices charged to our customers did not significantly impact transaction revenuegrowth in 2017 or 2016 .

Even though the margins on P2P transactions have lower rates and carry foreign exchange hedging losses compared to large merchants accounts which make up most of the so-called Total Payment Volume (this is a key financial metric for PayPal long-term success), the P2P market is massive:

The use of mobile peer-to-peer (P2P) payment apps such as Venmo in the US will continue to grow by double digits through 2021, according to eMarketer’s latest mobile banking and payments forecast.

Thus, besides the current amount of revenue provided by Venmo to affect PayPal’s bottom line, the strategic importance of this mobile app will also have a long-term financial impact.

Venmo origin story

As recounted by Andrew Kortina, Venmo co-founder viakortina.nyc:

We noticed that we were still using cash and checks to pay each other back and thought this was silly. Everyone should be using PayPal to pay each other back, but no one we knew was. We thought something must be not quite right about the PayPal experience for casual use, and we decided to design something that felt “right,” something that felt consistent with all of the other mobile tools we used to interact with our friends, like SMS, Gmail, Facebook, etc.

As roommates at the University of Pennsylvania in 2001 with Iqram Magdon-Ismail, a friendship was born.

During my senior year, Iqram and Andrew built their first real project; a college classifieds site called My Campus Post.

Then, the two started to build websites for local small businesses, at any price that would allow them to survive.

It was a real door-to-door selling experience that taught them about rejection and how to make things work.

After that, they joined an NYC-based company called iminlikewithyou.com, which Y Combinator-backed.

When the company pivoted to become a games company, the two young men left and temporarily split.

Iqram Magdon-Ismail joined Ticketleap as the VP of Engineering for a few years. Andrew Kortina bounced around and spent time working at Betaworks on Bit.ly.

They knew they wanted to do something together. They just didn’t know yet what would become their next venture.

When they browsed several ideas, they also thought of a music app. This is a scatch of the music app idea shared by Andrew Kortina via kortina.nyc:

Some interesting Venmo campaigns are funny and compelling:

Let’s not make it awkward, just ___ me,” and “If you ___ the wrong person tonight, you’ll regret it in the morning,

Venmo voice search command for Siri

Just like Google is continuing millions of people to talk with its voice assistants with a simple command that says “Hey, Google!”

Venmo is using a similar strategy for Siri, the voice assistant for Apple devices:

Make the brand Venmo fresh, fun, and cool

Other branding campaigns have been used to address millennials:

Why do millennials like it so much? As reported by millennials interviewed via clickondetroit.com:

“Venmo has essentially eliminated the use of checks for our generation,”

said recent Michigan State University graduate Nick Bognar.

“Having the ability to immediately pay a friend at dinner or split a bill with roommates over the phone is extremely convenient.”

Bognar, 25, said the social aspect of Venmo is a huge selling point.

“I also enjoy the network effect they have created. Venmo has a live feed similar to your Facebook timeline, and I can quickly see my friends paying each other,” Bognar said.

How much money does Venmo make?

As we’ve seen, Venmo is now part of the product offering for PayPal. Thus, although we don’t have any sales breakdown.

Venmo continues to be an incredibly powerful platform for engaging consumers. We processed more than $27 billion in volume for the quarter, growing 64%. That’s almost $300 million in payments per day and an annual run rate that now exceeds $100 billion. The Venmo team has made tremendous strides in enhancing the use cases of Venmo including a recently signed deal with Synchrony to provide a Venmo credit card. All of this is producing very strong monetization results. We ended Q3 with Venmo just shy of a $400 million annual revenue run rate.

Even though P2P transactions might have lower margins for PayPal, they bring benefits concerning market reach, product offering, and brand recognition.

Indeed, as of 2019, Venmo is not profitable yet, and its user base might be around 40 million digital users, as reported by CNBC.

How does Venmo work?

Whit Venmo, you can primarily perform a few activities like:

Make and Share Payments

Connect with people

Make purchases

Quickly transfer money to your bank

As claimed on the Venmo website:

Pay family and friends with Venmo accounts using a phone number or email. If they don’t have a Venmo account, they’ll just need to create one. Find friends automatically by syncing your Facebook or phone contacts.

Venmo is free unless you pay with credit cards:

When you send money using your Venmo balance, bank account, debit card or prepaid card, we waive fees so it’s free. Our standard 3% fee applies to credit cards. Receiving money and making purchases in other apps is always free.

Key takeaways

Venmo is a peer-to-peer mobile app, trendy among millennials, and part of the PayPal ecosystem.

Its popularity is also based on the ability of the company to make its name become a verb among millennials.

The app also allows PayPal to enhance its product offering and make it more suited for younger generations.

Venmo and other apps, part of the PayPal ecosystem, has taken over the peer-to-peer transaction industry.

Key Highlights

Venmo Overview:

Venmo is a peer-to-peer payments app that enables users to make payments and share money with friends for various services.

Venmo is part of the PayPal ecosystem and was acquired by Braintree in 2012, which was then acquired by PayPal in 2013.

The app offers a debit card in partnership with Mastercard.

Ownership and PayPal:

Venmo is owned by PayPal and is a critical part of PayPal’s expansion strategy.

PayPal acquired several brands, including Braintree, to broaden its product line.

Revenue Model:

Venmo generates revenue through transaction fees. While the service is free for most transactions, a 3% fee applies to credit card transactions.

Unlike many free apps that use advertisements, Venmo’s revenue comes from transaction fees.

Safety and Security:

Venmo claims to encrypt and protect users’ personal and financial data on secure servers to prevent unauthorized transactions.

P2P Transactions and Growth:

Person-to-person (P2P) transactions have been a significant growth driver for PayPal.

P2P transactions, including Venmo, contributed to PayPal’s growth, even though they may have lower margins compared to larger merchant transactions.

Venmo’s Origin:

Venmo was founded by Andrew Kortina and Iqram Magdon-Ismail.

The idea for Venmo came from a desire to create a mobile payment solution that felt consistent with other communication tools.

Venmo’s Popularity and Branding:

Venmo has become popular among millennials and is often used as a verb (“Venmo me”) in everyday language.

Venmo has launched branding campaigns to make its name synonymous with mobile payments.

Monetization and Growth:

Venmo processed billions of dollars in transactions and experienced significant growth, contributing to PayPal’s overall revenue.

While not profitable as of 2019, Venmo’s monetization efforts have shown promising results.

Functionality:

Venmo enables users to make payments, connect with friends, make purchases, and transfer money to their bank accounts.

It offers fee waivers for payments from Venmo balance, bank account, debit card, or prepaid card, with a 3% fee for credit card payments.

Key Takeaways:

Venmo’s integration within the PayPal ecosystem has been a successful strategy for both companies.

The app’s popularity among millennials and its use as a verb highlight its cultural impact.

P2P transactions, including Venmo, have transformed the peer-to-peer payments industry and contributed to PayPal’s growth.

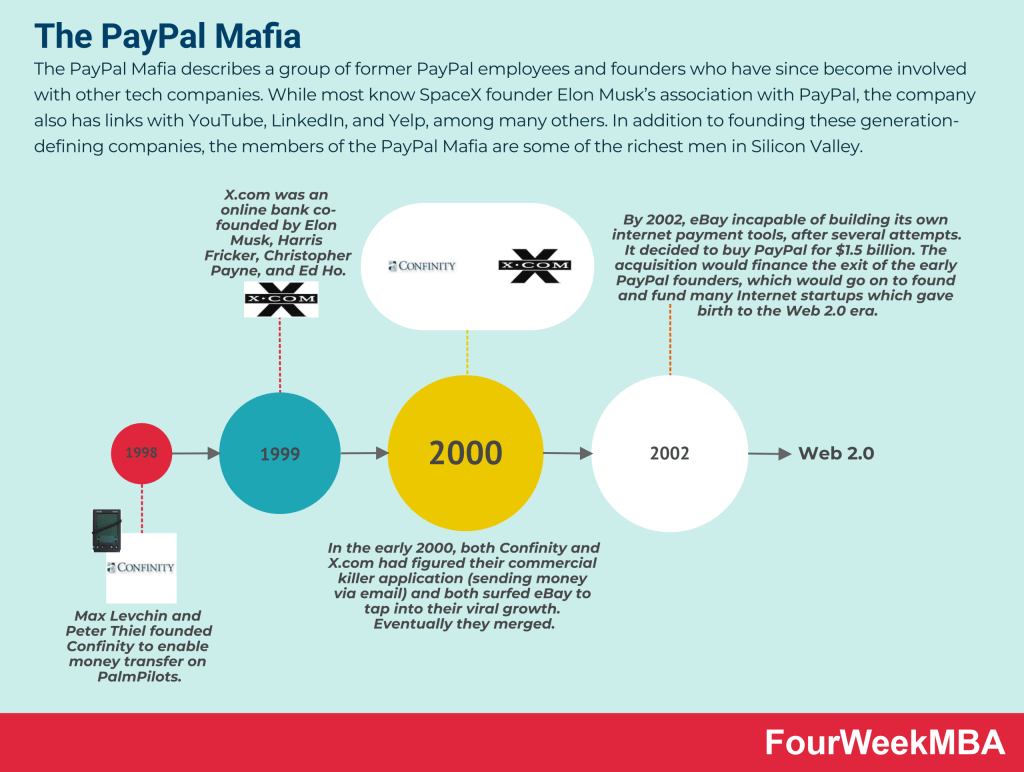

PayPal was first founded in 1998; it was called Confinity (among its founders was Peter Thiel); later, it merged with X.com, its major competitor, founded by Elon Musk (which would become known for other companies like Tesla and SpaceX). From this merger, PayPal was born. In 2002, PayPal was bought by eBay for $1.5 billion. eBay spun off PayPal in 2015, which would be listed as an independent entity. Today, PayPal owns brands like Braintree, Venmo, Xoom, and iZettle. Today, PayPal is mostly owned by institutional investors like The Vanguard Group (8.4%) and Blackrock (6.7%)

PayPal makes money primarily by processing customer transactions on the Payments Platform and other value-added services. Thus, the revenue streams are divided into transaction revenues based on the volume of activity or total payments volume—and value-added services, such as interest and fees earned on loans and interest receivable. In 2023, PayPal generated nearly $30 billion in revenues and $4.24 billion in net profits.

PayPal is a two-sided marketplace which collects a transaction fee for each payment that happens via the platform. PayPal’s flywheel is based on creating a stronger and stronger network, where the company provides a suite of services to merchants, and consumers are given affordable digital payment solutions. In 2022, PayPal processed over $1.35 trillion in global payments.

PayPal processed $1.53 trillion in payment volume in 2023, $1.36 trillion in payment volume in 2022, and $1.25 trillion in 2021—a growth of 12.5% year over year. In 2020, PayPal passed a trillion-dollar in payment volume, with $936 billion processed via the platform.

In 2023, PayPal generated nearly $30 billion in revenue compared to over $4.24 billion in profits. Compared to over $27.52 billion in revenue and over $2.42 billion in revenue in 2022.

In 2023, of nearly $30 billion in revenue, nearly $27 billion came from transaction revenues. Thus, transaction revenue represented over 90% of total revenue, while revenues from other value-added services (primarily comprising revenue earned through partnerships, interest and fees from merchants and consumer credit products, interest earned on certain assets underlying customer balances, referral fees, subscription fees, and gateway services) were over $2.91 billion, representing about 9% of PayPal’s total revenue.

PayPal had 426 million active accounts in 2023, a 2% slowdown compared to 435 million active accounts (users) in 2022, back to the 2021 level, when PayPal had 426 million active accounts.

The PayPal transaction per active account/user is a critical metric to measure the level of usage of PayPal. In 2023, the transaction per active account grew to 58.7, compared to 51.4 in 2022 and 45.4 in 2021. Thus, each active account has performed (on average) nearly 59 transactions via PayPal in 2023.

The PayPal Mafia describes a group of former PayPal employees and founders who have since become involved with other tech companies. While most know SpaceX founder Elon Musk’s association with PayPal, the company also has links with YouTube, LinkedIn, and Yelp, among many others. In addition to founding these generation-defining companies, the members of the PayPal Mafia are some of the richest men in Silicon Valley.

Acorns is a fintech platform providing services related to Robo-investing and micro-investing. The company makes money primarily through three subscription tiers: Lite – ($1/month), which gives users access to Acorns Invest, Personal ($3/month) that includes Invest plus the Later (retirement) and Spend (personal checking account) suite of products, Family ($5/month) with features from both the Lite and Personal plans with the addition of Early.

Started as a pay-later solution integrated to merchants’ checkouts, Affirm makes money from merchants’ fees as consumers pick up the pay-later solution. Affirm also makes money through interests earned from the consumer loans, when those are repurchased from the originating bank. In 2020 Affirm made 50% of its revenues from merchants’ fees, about 37% from interests, and the remaining from virtual cards and servicing fees.

Alipay is a Chinese mobile and online payment platform created in 2004 by entrepreneur Jack Ma as the payment arm of Taobao, a major Chinese eCommerce site. Alipay, therefore, is the B2C component of Alibaba Group. Alipay makes money via escrows transaction fees, a range of value-added ancillary services, and through its Credit Pay Instalment fees.

Betterment is an American financial advisory company founded in 2008 by MBA graduate Jon Stein and lawyer Eli Broverman. Betterment makes money via investment plans, financial advice packages, betterment for advisors, betterment for business, cash reserve, and checking accounts.

Braintree

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Chime is an American neobank (internet-only bank) company, providing fee-free financial services through its mobile banking app, thus providing personal finance services free of charge while making the majority of its money via interchange fees (paid by merchants when consumers use their debit cards) and ATM fees.

Coinbase is among the most popular platforms for trading and storing crypto-assets, whose mission is “to create an open financial system for the world” by enabling customers to trade cryptocurrencies. Its platform serves both as a search and discovery engine for crypto assets. The company makes money primarily through fees earned for the transactions processed through the platform, custodial services offered, interest, and subscriptions.

Compass is a licensed American real-estate broker incorporating online real estate technology as a marketing medium. The company makes money via sales commissions (collected whenever a sale is facilitated or tenants are found for a rental property) and bridge loans (a service allowing the seller to purchase a home before the revenue from the sale of their previous home is available).

Dosh is a Fintech platform that enables automatic cash backs for consumers. Its business model connects major card providers with online and offline local businesses to develop automatic cash back programs. The company makes money by earning an affiliate commission on each eligible sale from consumers.

E-Trade is a trading platform, allowing investors to trade common and preferred stocks, exchange-traded funds (ETFs), options, bonds, mutual funds, and futures contracts, acquired by Morgan Stanley in 2020 for $13 billion. E-Trade makes money through interest income, order flow, margin interests, options, future and bonds trading, and through other fees and service charges.

Klarna is a financial technology company allowing consumers to shop with a temporary Visa card. Thus it then performs a soft credit check and pays the merchant. Klarna makes money by charging merchants. Klarna also earns a percentage of interchange fees as a commission and for interests earned on customers’ accounts.

Lemonade is an insurance tech company using behavioral economics and artificial intelligence to process claims efficiently. The company leverages technology to streamline onboarding customers while also applying a financialmodel to reduce conflicts of interest with customers (perhaps by donating the variable premiums to charity). The company makes money by selling its core insurance products, and via its tech platform, it tries to enhance its sales.

Monzo is an English neobank offering a mobile app and a prepaid debit card for consumers and businesses. It was one of the first app-based banks to enter the UK market, founded by Gary Dolman, Jason Bates, Jonas Huckestein, Paul Rippon, and Tom Blomfield in 2015. All were employees of Starling Bank, a similar neobank challenging the dominance of established financial institutions in England. The company enjoys many revenue streams: business and consumer subscriptions, interchange and overdraft fees, personal loans, and more.

NerdWallet is an online platform providing tools and tips on all matters related to personal finance. The company gained traction as a simple web application comparing credit cards. NerdWallet makes money via affiliate commissions determined according to the affiliate agreements.

Quadpay was an American fintech company founded by Adam Ezra and Brad Lindenberg in 2017. Ezra and Lindenberg witnessed the rising popularity of buy-now-pay-later service Afterpay in Australia and similar service Klarna in Europe. Quadpay collects a range of fees from both the merchant and the consumer via merchandise fees, convenience fees, late payment, and interchange fees.

Revolut an English fintech company offering banking and investment services to consumers. Founded in 2015 by Nikolay Storonsky and Vlad Yatsenko, the company initially produced a low-rate travel card. Storonsky in particular was an avid traveler who became tired of spending hundreds of pounds on currency exchange and foreign transaction fees. The Revolut app and core banking account are free to use. Instead, money is made through a combination of subscription fees, transaction fees, perks, and ancillary services.

Robinhood is an app that helps to invest in stocks, ETFs, options, and cryptocurrencies, all commission-free. Robinhood earns money by offering: Robinhood Gold, a margin trading service, which starts at $6 a month, earn interests from customer cash and stocks, and rebates from market makers and trading venues.

SoFi is an online lending platform that provides affordable education loans to students, and it expanded into financial services, including loans, credit cards, investment services, and insurance. It makes money primarily via payment processing fees and loan securitization.

Squarespace is a North American hosting and website building company. Founded in 2004 by college student Anthony Casalena as a blog hosting service, it grew to become among the most successful website building companies. The company mostly makes money via its subscription plans. It also makes money via customizations on top of its subscription plans. And in part also as transaction fees for the website where it processes the sales.

Stash is a FinTech platform offering a suite of financial tools for young investors, coupled with personalized investment advice and life insurance. The company primarily makes money via subscriptions, cashback, payment for order flows, and interest for cash sitting on members’ accounts.

Venmo is a peer-to-peer payments app enabling users to share and make payments with friends for a variety of services. The service is free, but a 3% fee applies to credit cards. Venmo also launched a debit card in partnership with Mastercard. Venmo got acquired in 2012 by Braintree, and Braintree got acquired in 2013 by PayPal.

Wealthfront is an automated Fintech investment platform providing investment, retirement, and cashmanagement products to retail investors, mostly making money on the annual 0.25% advisory fee the company charges for assets under management. It also makes money via a line of credits and interests on the cash accounts.

Zelle is a peer-to-peer payment network that indirectly benefits the banks’ consortium that backs it. Zelle also enables users to pay businesses for goods and services, free for users. Merchants pay a 1% fee to Visa or Mastercard, who share it with the bank that issued the card.

Gennaro is the creator of FourWeekMBA, which reached about four million business people, comprising C-level executives, investors, analysts, product managers, and aspiring digital entrepreneurs in 2022 alone | He is also Director of Sales for a high-tech scaleup in the AI Industry | In 2012, Gennaro earned an International MBA with emphasis on Corporate Finance and Business Strategy.

2 thoughts on “How Does Venmo Make Money? Venmo Business Model In A Nutshell”

thank you so much

you’re welcome 🙂